Since you are also.</p>

"Pinterest")

Insurance is one of the most digitally researched industries today, but one of the least digitally purchased.

74% of insurance shoppers go online to research and get quotes, while 25% purchase a policy online. (Source: JDPower)

Since you are also in the insurance industry, this data might not seem strange to you. This is something that every insurance company is going through.

Have you ever wondered what the possible reason behind it could be? Among all the reasons, one issue remains the same: insurance software in front of the customer is not built for them.

As a result, forward-thinking insurance companies are investing in insurance software development services tailored to their specific customers, products, and buying journeys.

From policy administration to claim management software, the right software allows customers to feel informed about what they are buying, valued as a buyer, and trusted enough to complete the purchase online.

Cut short, insurance software purpose-built for your specific processes and customer needs is key to sustaining and succeeding in the industry.

This blog will help you cover everything you need to know about insurance software development in 2026, including types, core capabilities, technologies, development process, compliance, costs, trends, and how to pick the right development partner.

So, let’s get started.

What is Insurance Software Development?

Insurance software development is the process of building software tailored to your insurance business processes. It combines insurance and technology, also known as insurtech, to help your business understand your customers better and serve them more efficiently.

So, instead of forcing your team and your customers to work around a generic platform, the software works around how your business actually runs.

Technically speaking, insurance software development is the process of designing, building, testing, and deploying software using the technologies your business needs.

This includes policy administration systems, claims management software, underwriting tools, customer portals, agent dashboards, billing modules, and integrations with payment gateways, KYC services, and regulatory systems.

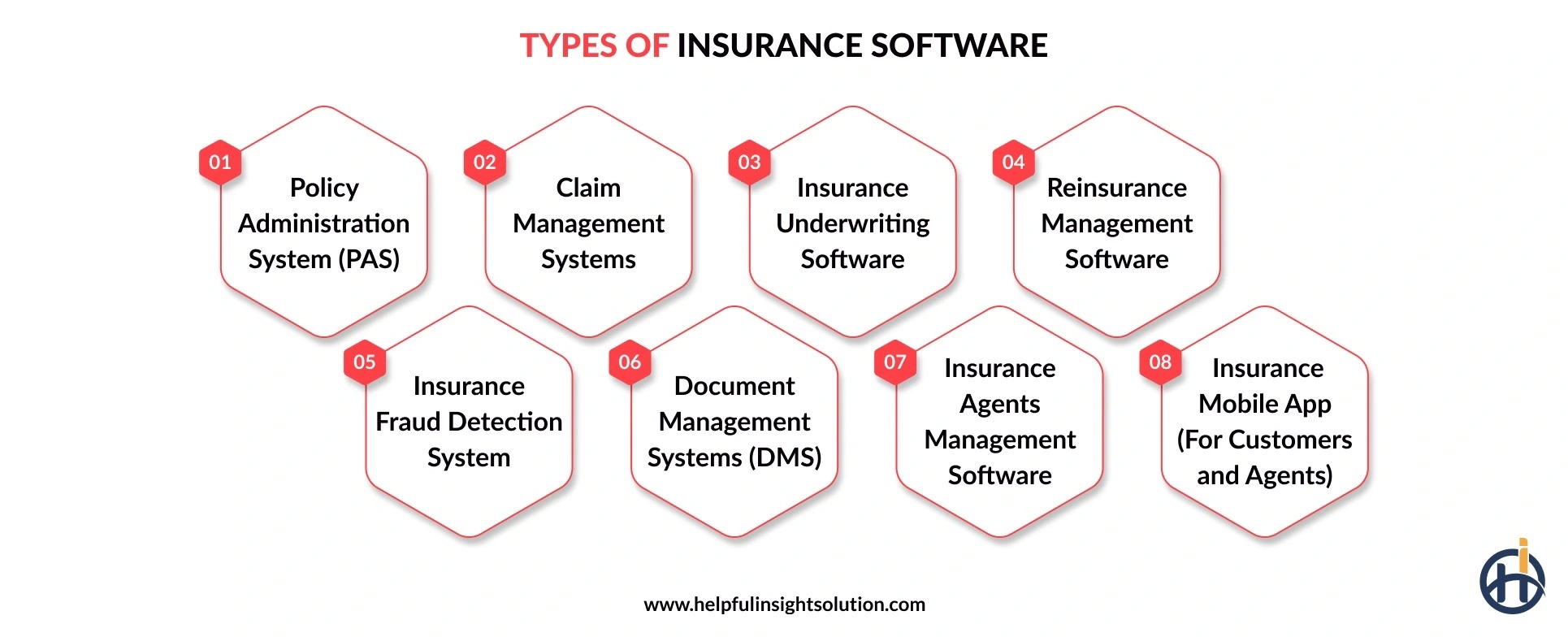

Types of Insurance Software

Insurance is a broad industry with multiple processes; therefore, it requires different types of software, each handling a specific business process.

In this section, we will discuss the types of insurance software, so you can know the value of each for your business processes.

1. Policy Administration System (PAS)

The Policy Administration System (PAS) is one of the essential software systems for insurance companies of all sizes. It helps to manage the end-to-end lifecycle of a policy from issuance and underwriting to renewals, endorsements, and cancellations.

Simply saying, you can name it as a central record system that stores every policy detail, premium calculation, and customer interaction tied to that policy.

In 2026, as 47% of all insurance policies are purchased online through digital channels, a policy administration system is a must to help your customers with online facilities for all their policy-related needs.

2. Claim Management Systems

Claims are an inevitable part of the insurance business and how you handle them is the single biggest factor in customer retention in 2026 and beyond. A claim is the moment a customer needs you the most. So, if your claim process is slow or messy, you are making their tough moments harder, and that is the fastest way to lose them.

Insurance claim management software brings the entire claim process online from first notice of loss (FNOL) to investigation, approval, and payout. Additionally, it connects adjusters, customers, agents, and third parties like repair shops or hospitals on a single platform, making the claim a hassle-free process.

3. Insurance Underwriting Software

Underwriting is the backbone of the insurance industry, which has an important role in determining who should get insurance at what price based on risk profile assessment.

Insurance underwriting software helps insurers assess risk and decide whether to issue a policy and at what premium. It can pull data from multiple sources, such as credit reports, medical records, telematics, and public records, and uses preset rules or AI models to score the risk.

So, instead of an underwriter spending hours on manual checks, the software does most of the heavy lifting in seconds. Additionally, the use of AI in insurance software development can also support straight-through processing, which means low-risk applications get approved automatically without human intervention.

4. Reinsurance Management Software

Reinsurance is the process by which a company buys insurance from another company to cover its risk.

Having reinsurance management software that tracks these reinsurance contracts, calculates the ceded premiums and recoverables, manages claims recoveries, and handles reporting for regulators.

So, for large insurers and reinsurance companies, this software keeps the books accurate and the contracts managed. Without it, reinsurance accounting becomes a manual mess of spreadsheets, which is risky for an industry where billions of dollars move between carriers and reinsurers.

5. Insurance Fraud Detection System

Fraud is something that not only hurts the company’s finances but also its reputation. Therefore, having fraud detection software that uses data analytics, machine learning, and rule-based systems to spot suspicious claims and applications.

For example, this software can flag anomalies such as duplicate claims, inflated damage estimates, or staged accidents, so investigators can review all anomalies before finalising the claim.

6. Document Management Systems (DMS)

The insurance industry runs on documents. Today, as everything is digitised, a document management system should be there.

A Document Management System stores, organises, and retrieves all the paperwork tied to insurance, such as policy documents, claims files, ID proofs, medical reports, signed agreements, and regulatory filings. Additionally, it can also handle version control, access permissions, and audit trails.

Keep it simple. So, a DMS removes the chaos of scattered files and makes sure agents, underwriters, and claim adjusters can pull up the right document in seconds.

7. Insurance Agents Management Software

Agents and brokers are often the first point of contact for customers when they are purchasing policies. So, don’t you think there should be software to manage the network of agents seamlessly?

Agents Management Software handles the network of agents, keeping track of their performance, managing commissions, licensing, and compliance. Additionally, it can also act as a single source of truth for all the information agents need to sell faster, such as quote engines, lead management, and policy issuance.

8. Insurance Mobile App (For Customers and Agents)

An insurance mobile app can be both customer-facing and agent-facing front end of the entire insurance business.

For customers, it lets them buy policies, file claims, pay premiums, upload documents, and check coverage from their phone. For agents, it lets them generate quotes, onboard customers, manage leads, and access policy details on the go.

Ultimately, an insurance mobile app is a must to sustain in a competitive environment and grow by investing in the right mobile app development, which makes insurance processes simple and trustworthy.

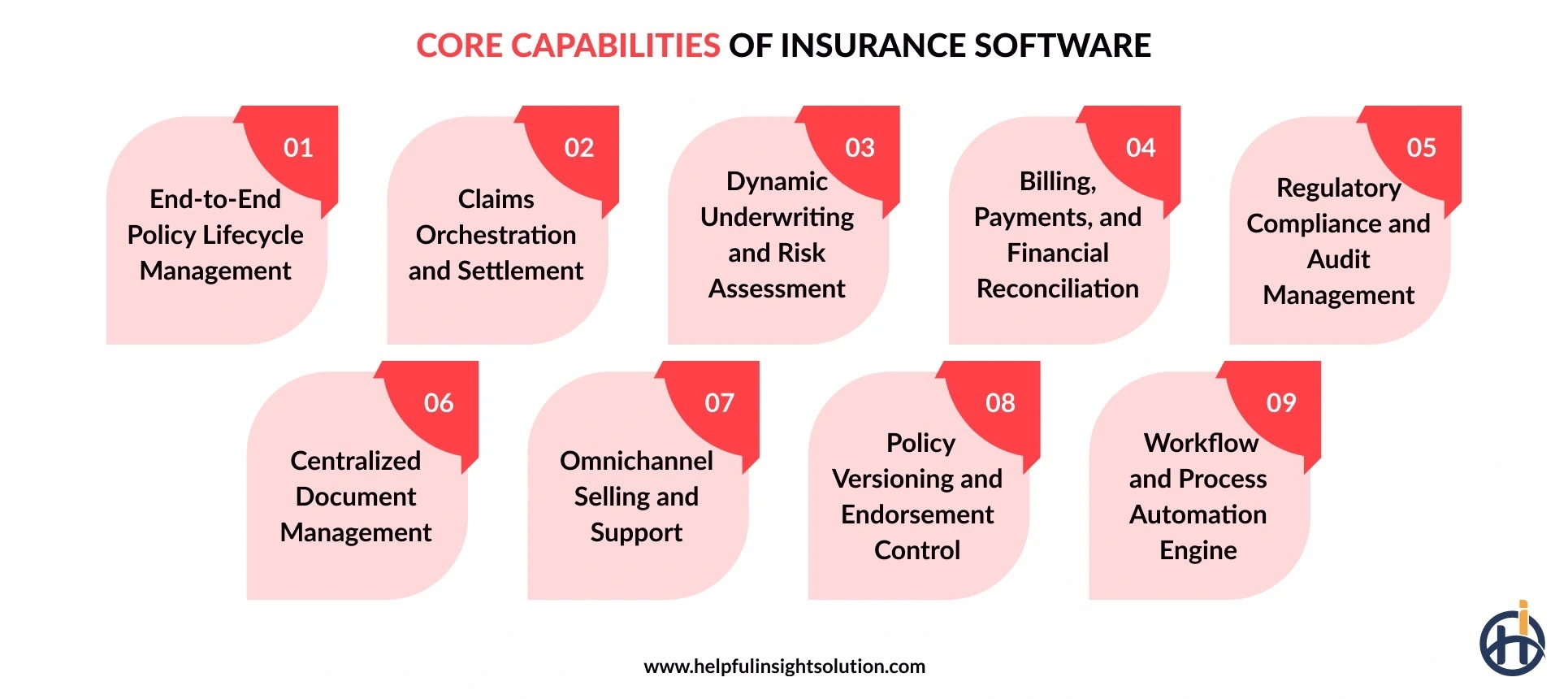

Core Capabilities of Insurance Software

Every insurance company is different, and so is the insurtech software development purpose-built to support their needs. Here, we have discussed some of the core capabilities every insurance software must have.

1. End-to-End Policy Lifecycle Management

This feature refers to the capability of handling the policy from the day it has been issued till the day it’s cancelled. Simply said, you will have access to everything that happens to that policy in between (premium payments, endorsements, claims, customer requests) in a single system.

Without a single record of policy management, your agent might see one version of policy, while underwriters see another one. Also, what if your customers see another one? This could lead to several conflicts and issues, resulting in lost customers and revenue.

You can mark this feature as one of the must-have features for insurance software development to be considered.

2. Claims Orchestration and Settlement

As said earlier, a claim is the moment when you either retain your customers by supporting them or lose them.

This is the moment when the customer is already stressed, so they need a process that is simple, fast, and easily accessible to them.

Claim orchestration capability connects all processes and people involved in claim settlement into one platform. So, when the customer submits the claim requests, it automatically routes to the right person.

Additionally, you can also use the AI to automate the process; human involvement will be needed only for final approval.

Doesn’t this capability seem beneficial for both customers and insurance companies as well? This is the right benefit. If you ask me about indirect benefits, you can enjoy repeat customers and word-of-mouth marketing.

3. Dynamic Underwriting and Risk Assessment

Traditional underwriting takes days, if not months, to do so. Nowadays, when customers are seeking speed and convenience, the traditional underwriting process is the step where you lose your customers.

Insurance software can be integrated with credit bureaus, medical records, and telematics devices. Therefore, you can have all the relevant underwriting fetch instantly, speeding up the policy issuance process.

Additionally, as said beforehand, you can use AI to ensure that low-risk applications are approved automatically.

4. Billing, Payments, and Financial Reconciliation

Insurance billing has many options to offer customers, such as monthly, quarterly, or annually. Additionally, there are policies such as group plans that split the premium between the employer and the employee.

On top of that, agent commissions also need to be calculated correctly to protect healthy margins.

Get this wrong, and your finance team spends a week every month chasing mismatches. Get it right, and nobody calls the support team about a wrong premium charge. This feature helps you do the same.

5. Regulatory Compliance and Audit Management

Insurance in the USA, UK, Dubai, and across the world ranks among the highly regulated industries. Every region has its own rulebook on data retention, KYC, customer consent, and product approvals, which must be complied with.

The insurance carrier software must be developed following these compliance requirements from day one to ensure no regulatory issues harm your business.

Additionally, at Helpful Insights, we believe that the insurance bodies may also introduce new regulations; therefore, the software we built can adapt to them easily.

6. Centralized Document Management

As discussed earlier, the insurance industry runs heavily on paperwork. This paperwork will help you have a single view of all the documents, such as proposal forms, ID proofs, signed agreements, claim photos, repair invoices, medical reports, and renewal notices.

You can pull any document related to any policy within seconds.

7. Omnichannel Selling and Support

Nowadays, customers don’t buy an insurance policy as they used to. Nowadays, they start their purchasing journey from the website, get a quote on a mobile app, and if any help is needed, they reach out to you on WhatsApp.

Having omnichannel selling and support capability ensures that customers’ information is transmitted to each channel they switch to without having to repeat it. So, their experience will be enhanced.

8. Policy Versioning and Endorsement Control

Policy changes may happen at any time during its duration.

For example, a beneficiary changes after a wedding or a death.

Each policy change is called an endorsement, and each endorsement creates a new version of the policy.

This capability of insurance carrier software will ensure that each endorsement is updated in the policy and communicated effectively to the customer.

9. Workflow and Process Automation Engine

This is the feature that can automate the low-touch tasks, such as renewal reminders, compliance check triggers, new policy issuance, and more.

These low-touch activities will be supported by the software itself without human intervention. So, your human workforce will focus on high-touch activities to bring more revenue, a core benefit of RPA in insurance.

Why Do Insurance Companies Need Specialised Software?

Insurance is unlike any other industry. Customer expectations and competition are increasing day by day, making it hard for insurers to sustain and grow in the industry.

Insurance software development purpose-built for your business is a must-have to remain competitive in the industry. Here we have outlined a few reasons why insurance companies need specialised software.

1. Half of the Insurance Buyers Now Purchase Their Policy Through Digital Channels

Almost half of the insurance buyers begin searching for policies through digital channels, instead of traditional methods like going through agents and branches. (Source: J.D. Power 2025 U.S. Insurance Digital Experience Study)

Additionally, the same study also found that 92% of customers with a good digital experience are more likely to make a purchase. This means the buying journey, the quote, the comparison, and the payment are all happening on a screen, and the customer experience must be intuitive.

So, the insurance company that fails to deliver a smooth digital experience loses these customers to a competitor whose software actually works.

2. AI in Insurance Could Deliver $1.1 Trillion in Annual Value, But Only on Specialised Platforms

McKinsey & Company estimates that AI could create up to $1.1 trillion in annual value for the global insurance industry. This value will be a byproduct of improvements in underwriting, claims processing, fraud detection, and customer service.

However, AI is only as good as the software that powers it. A specialized insurance software is the foundation to enable AI development services to deliver real value.

AI needs real-time data, insurance-specific models, and integrations with telematics, medical records, claims history, and risk databases. A specialised insurance software is the foundation to enable AI to deliver value.

3. Specialised Insurance Software Reduces Cost Per Policy by 41%

Insurance is a cost-prone industry. Every single dollar spent on operations directly affects profitability.

According to McKinsey, insurers running modern, specialized platforms achieve a 41% lower cost per policy and 40% higher operations productivity than peers using off-the-shelf or legacy software. Therefore, this saving can help the insurance companies to recover their insurance software development cost within a year or two.

4. 81% Customer Retention Is Achievable With Personalized Insurance Services

Personalization in the insurance industry is no longer a marketing trend. Personalization is a key player for attracting and retaining customers.

Insurers that offer personalized products and experiences see customer retention rates jump to 81%, along with an 89% increase in customer engagement. However, to support personalization, the software must capture every customer interaction, understand customers’ coverage history, and tailor every renewal, recommendation, and communication.

A specialized insurance software purpose-built for your specific products and customers can help you to achieve personalization.

Custom vs. Off-the-Shelf Insurance Software

In simple terms, off-the-shelf software is the pre-built insurance platform you license from a vendor. You sign up, configure a few settings, and start using it.

Custom insurance software, on the other hand, is built from scratch around your specific products, workflows, and customer base.

For example, off-the-shelf is like renting a furnished apartment. Custom is like designing your own home. Both software works, but serve different purposes.

Technically speaking, off-the-shelf platforms come with fixed architecture, pre-defined modules, and limited APIs for integration. They’re faster to deploy and lower in upfront cost.

Custom insurance software development gives you full control over the tech stack, data architecture, integrations, and the underwriting and claims logic.

Ultimately, the choice of which software to use is subject to your needs. For example, if you are an early-stage InsurTech disrupting traditional insurance models or a small carrier, then you can start with off-the-shelf. Conversely, mid-sized insurers choose custom software development for better control.

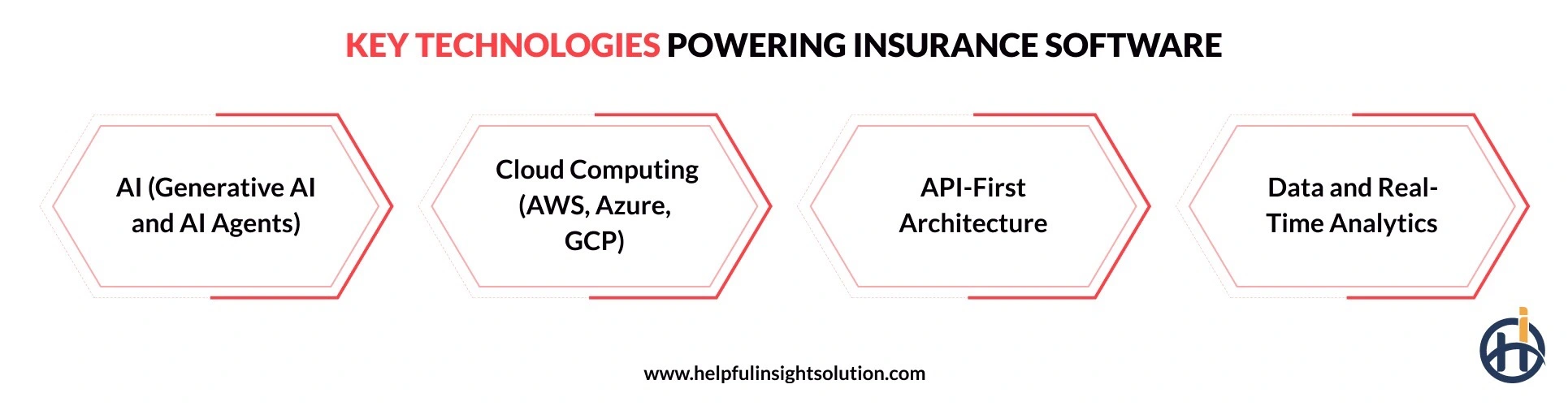

Modern insurance software is built on a few core technologies that work together to handle policies, claims, customer data, and integrations. Here are the four that matter the most.

Key Technologies Powering Insurance Software Today

Modern insurance software is built on a few core technologies that work together to handle policies, claims, customer data, and integrations. Here are the four technologies powering software today.

1. AI (Generative AI and AI Agents)

According to BCG, the insurance industry is adopting AI faster than any other industry, such as technology, media, and telecommunications.

When it comes to AI, generative AI agents are fueling the adoption.

Simply put, generative AI is the technology that reads, writes, and explains. Beyond this, it can also draft a policy document and answer customer queries through chat.

Agentic AI, on the other hand, can act like your employee. For example, an AI agent can trigger a renewal, request a missing document from a customer, or run an underwriting check.

Technically speaking, both are powered by large language models trained on insurance-specific data. They can help insurers to reduce manual work, speed up the customer experience, and free up the team for complex cases.

2. Cloud Computing (AWS, Azure, GCP)

Have you heard about AWS, Azure, and Google Cloud? These are the 3 cloud computing service providers powering the majority of the insurance companies globally.

Simply put, they are helping insurers to securely store all their data on a remote server, making it accessible from anywhere in the world. Additionally, they can allow you to scale up when you need more, and pay only for what you use.

For an insurance business, cloud computing helps in three ways. It supports faster product launches, handles regional data residency requirements, and reduces the cost of running large-scale software.

3. API-First Architecture

API-first architecture means the insurance software is designed around APIs from day one. Every function, like issuing a policy or fetching a quote, can be accessed by another system through a clean API.

API-first architecture helps insurance software to communicate and pull data from external partners.

For example, you can connect it with payment gateways, pull KYC data, and integrate with hospitals, garages, and partner networks.

4. Data and Real-Time Analytics

Insurance is a data-driven business. Therefore, real-time analytics is the technology that collects and analyzes data instantly, instead of running it through reports that the team reviews later.

In insurance software, real-time analytics is used to track risk, monitor customer behavior, detect fraud as it happens, and check business performance live.

The benefit is simple: better data leads to better pricing and fewer losses. Insurers who run their software on real-time analytics react faster to market changes than those still depending on weekly or monthly reports.

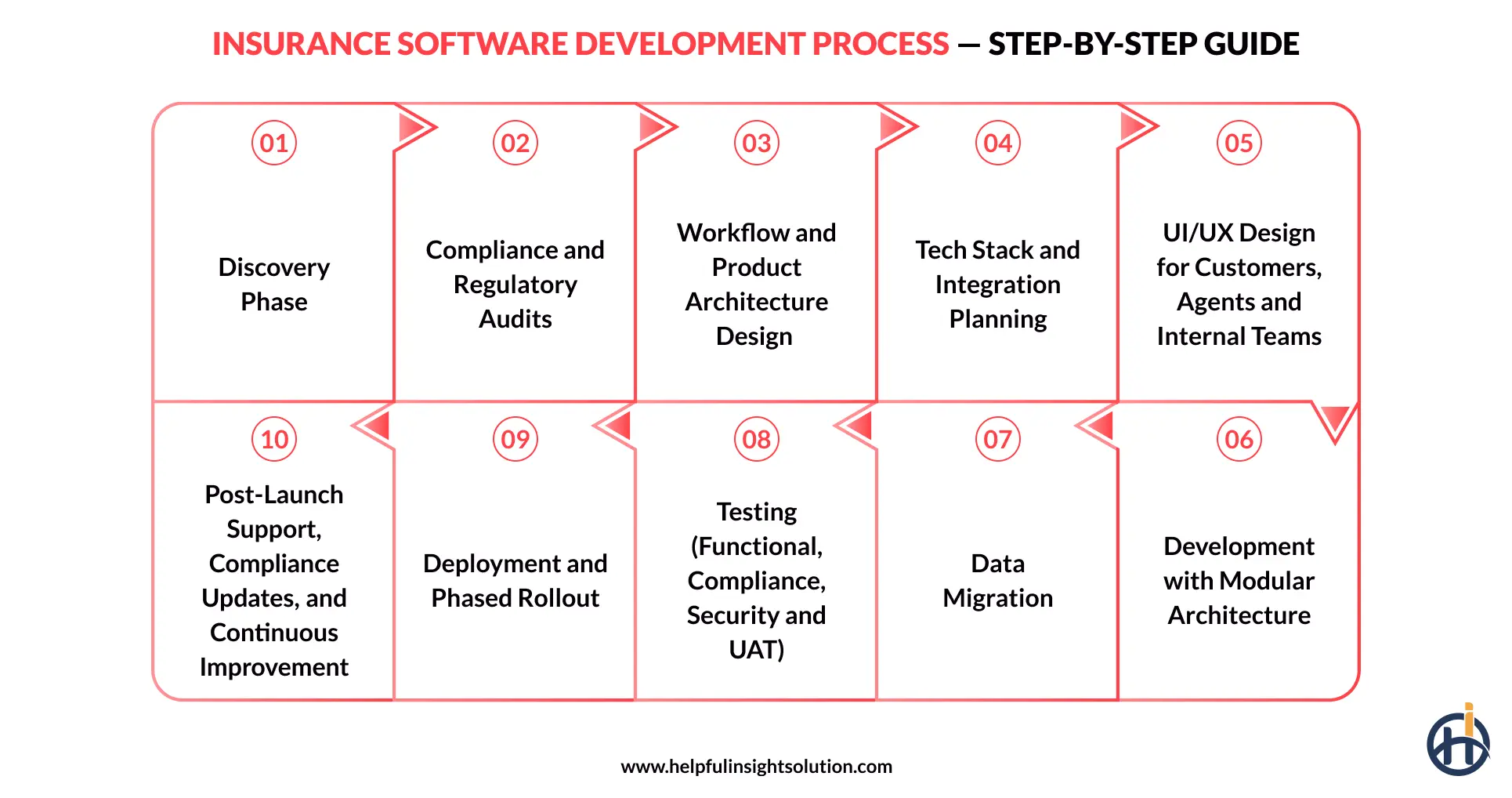

The Insurance Software Development Process — Step-by-Step Guide

The insurance software development process is not a one-size-fits-all process. Every insurance product has its own processes, product, and customer base; therefore, the software must be tailored to them.

Here is a step-by-step insurance software development process we follow at Helpful Insights.

Phase 1. Discovery Phase

This might seem too basic, but you will be surprised to learn that most of the projects fail because they often take it very easy.

We believe that you know your business and customers better than anyone. Therefore, leveraging our industry expertise and your knowledge, we will understand your needs and align them with your goals.

This process starts by understanding the line of business you operate, like motor, health, life, P&C, or commercial.

The next step is knowing your products and how they are priced, along with the distribution channels, such as agent-led, direct-to-customer, or broker-driven.

We also work on knowing the existing pain points your business might be facing. For example, if your claim TAT is high, or your renewal drop-off is high, the software has to be designed to fix those gaps.

Understanding this will yield the foundation for custom insurance software solutions that will deliver the return on investment from day one.

Phase 2. Compliance and Regulatory Audits

As said earlier, insurance is a highly regulated industry. Therefore, insurance software development has to map out regulations, and your software must answer.

Each regulation has its own rules on data residency, customer consent, KYC, audit trails, and reporting. These rules shape the architecture, the database design, and the user flows.

For example, if you operate in the USA, customer data has to be hosted within the USA, which means your cloud setup has to be planned accordingly from day one.

Phase 3. Workflow and Product Architecture Design

In this next step, the team starts working on translating your insurance workflows into a system design. This will include underwriting flow, claims flow, policy lifecycle, endorsement handling, billing logic, and how each product is structured.

For example, if you are selling a motor insurance product, you might have different flows than a health insurance product. Health insurance software development will need medical underwriting, network hospital integration, and cashless claim flows. Therefore, the architecture must support the needs of the business.

Phase 4. Tech Stack and Integration Planning

This step covers two decisions. First, the tech stack, which includes the database, language, frameworks, and cloud provider. Second, the external system of the software needs to communicate to perform different tasks.

Phase 5. UI/UX Design for Customers, Agents, and Internal Teams

Insurance software has different users to serve, such as customers, agents, and internal teams. Each user has different expectations from the software.

For example, Customers need a simple interface to buy policies, file claims, and pay premiums. Agents need fast quote tools, lead management, and policy issuance flows. Internal teams like underwriters and claim adjusters need deep data, reports, and decision-support tools.

The software must be designed keeping the needs of all three users in mind so that they can navigate easily with the best user experience possible.

Phase 6. Development with Modular Architecture

The software is built in modules instead of one large monolithic system. The main modules include policy administration, claims management, underwriting, billing, customer portal, and agent portal.

Each module of software is built and deployed independently. So, you can update or replace one module without breaking the rest.

Phase 7. Data Migration

If you are an established player in the insurance market, then existing data must be migrated from the legacy system to a new, built insurance application.

The data could be anything from policy records, customer data, claims history, agent records, financial transactions, and document archives. Additionally, you might also have to perform data cleansing to ensure the migrated data is consistent and ready to support the software.

Phase 8. Testing (Functional, Compliance, Security, and UAT)

This is the step when your chosen development partner’s expertise will be tested. The software must go through the four testing layers, such as functional, compliance, security, and UAT.

Here is an understanding of each insurance software testing layer.

Functional testing checks whether each feature works as expected. Compliance testing verifies that the software meets the regulatory requirements identified in step 2. Security testing covers data protection, encryption, penetration testing, and vulnerability checks.

User acceptance testing, also called UAT, is done with actual underwriters, claim adjusters, and agents using the software in real-world scenarios.

Each layer is important, and skipping any one of them can lead to issues post-launch. For example, missing security testing can lead to data breaches, which are extremely costly in terms of insurance.

Phase 9. Deployment and Phased Rollout

At Helpful Insights, we emphasize phased rollout instead of a single release. You can start with one line of business, one region, or one user group, to see software is performing well.

Once that phase is proven to be stable, you can proceed to the next phase roll-out.

For example, a multi-line insurer might launch a motor first, run it for two to three months, fix any issues, and then roll out health and life.

Final Phase. Post-Launch Support, Compliance Updates, and Continuous Improvement

Software is never finished, and the insurance industry is no exception. Once it goes live, the work shifts to ongoing support and continuous improvement. This includes fixing bugs, adding new product lines, integrating new partners, and adapting to new regulatory requirements.

Our Insurance IT Services team ensures your software stays compliant and scalable as your business grows.

For example, if IRDAI introduces a new disclosure requirement next year, the software has to be updated to comply with it. Similarly, if you decide to launch a new product like cyber insurance for SMEs, the system has to support it.

This is exactly how we have built market-leading products for our clients. See our portfolio

Challenges in Insurance Software Development

Here, we have outlined a list of challenges we have seen firsthand in insurance software development. Therefore, we can plan your software development to ensure challenges never come in the way.

Modeling Insurance Products

Insurance products are not simple transactions. For example, a single motor insurance policy might have multiple covers (OD, TP, add-ons), conditional pricing rules, NCB logic, IDV calculations, and underwriting exceptions. Therefore, software must be developed to have an accurate pricing and coverage model for each customer.

Handling High Transaction Volumes

Renewal season, festival sales, regulatory deadlines, or events like floods, earthquakes, or pandemics cause sudden spikes in policy purchases or claims. Therefore, the software must be developed to handle 10x to 20x or a normal load without facing any issues.

At Helpful Insights, we recommend using AWS’s auto‑scaling (EC2, ECS, EKS, Lambda) to ensure servers are added or removed to handle increased traffic, while keeping the cost controlled.

Security and Privacy Across Multiple Geographies

Insurance handles some of the most sensitive personal data, such as medical history, financial records, and KYC documents. Furthermore, security has to meet the highest standards while also complying with data residency rules in each market.

Balancing Automation With Human Involvement

A lot of insurance work, like underwriting and claim assessment, needs human judgment for edge cases.

Building software that automates the routine 80% but routes the complex 20% to the right human, with full context, is harder than full automation or full manual work.

Insurance Software Development Cost and ROI

Insurance software development costs are subject to multiple factors, including scope, integrations, compliance requirements, and, most importantly, where the development team is based.

For example, a developer in the US costs $75 to $120 per hour. The same skilled developer in India costs $25 to $50 per hour. This is why insurance companies in the US, UK, and UAE choose insurance software development services in India. You get the same talent and engineering quality at 50% to 70% lower cost.

The ROI comes from faster policy issuance, automated claims, lower fraud losses, and reduced operational costs. Most insurance software pays for itself within the first one to two years.

Trends Shaping Insurance Software in 2026

The insurance industry is evolving fast, and everyone knows that. The real advantage, however, comes from knowing exactly which trends are driving this change. Let’s look at the trends shaping insurance software in 2026.

1. Embedded Insurance

Embedded insurance is the practice of selling insurance inside another product or service, instead of selling it as a separate purchase.

For example, Uber offers in-trip insurance to riders in many markets through partnerships with insurers like Chubb. The cover is automatically included in the trip cost or offered at booking, without the rider having to visit a separate insurance website. Similarly, Airbnb offers built-in host protection and guest cover during bookings.

The numbers behind this trend are big. According to Research and Markets, the embedded insurance market was valued at $116.05 billion in 2025 and is projected to grow at a CAGR of 19%, reaching an estimated $138.08 billion in 2026.

2. Micro-Insurance and On-Demand Products

Micro-insurance is short-term, hyper-specific coverage built around a real-time need. Examples include 1-day travel insurance for a single trip, hourly car insurance for short-term vehicle use, and gig worker coverage that activates only during work hours.

The global micro-insurance market, from $95.15 billion in 2026, is expected to reach $171.44 billion by 2035 at a CAGR of 6.77%.

Additionally, this trend also matters because it matches modern usage patterns.

Nowadays, customers are looking for alternatives to traditional policies to policies covering them during vulnerable times for a few hours, a few days, or a single event. So, stepping into this trend can help with a competitive advantage over others.

3. Hyper-Personal Insurance

Customers’ preferences are changed to policies that are purpose-built for them, rather than one-size-fits-all. Hyper-personalization ensures that the policy coverage and pricing are tailored for individuals.

For example, two customers buying the same health insurance product can pay different premiums based on their lifestyle, health metrics, and medical history. Similarly, a young driver with safe driving habits can get lower motor premiums than another driver of the same age and vehicle.

4. Zero Touch Claims

Zero-touch claims refer to the automated process in which claims are processed and settled within minutes with minimal human involvement. The process looks like the following:

Customer files a claim → system validates the data → runs fraud checks → calculates payouts → approves the claim.

For example, in motor insurance, AI can review uploaded photos of vehicle damage, estimate the repair cost, cross-check the policy, and approve the claim without an adjuster visiting the site.

According to Forrester’s insurance technology survey, 91% of the insurance providers will deploy an AI-powered claim automation system. Therefore, it has become a must to deploy automated claim management to stay competitive in the market.

5. Usage-Based and Behavior-Based Pricing (UBI 2.0)

Usage-based insurance has been in the industry for a long period of time, powered by basic telematics.

UBI 2.0 goes further. It includes driving style scoring based on real driving data, health behavior tracking through wearables apps, and lifestyle-based pricing for life and health products.

This helps customers with a lower price based on their safe habits.

How to Choose the Right Insurance Software Development Partner?

The selection of an insurance software development company is one of the most important decisions. The wrong selection can result in delays, compliance issues, or require rebuilding the software from scratch. Here is how you can choose the right partner:

- Insurance domain experience: First preference should be given to companies with prior experience in building insurance software. Additionally, if your software requires AI capabilities, knowing how to hire AI developers with insurance domain experience will give you a strong advantage

- Regulation knowledge of your market: If you operate in the USA, the development partner should have an understanding of NAIC and state-level regulators. Validate compliance requirements mandated in your market.

- Portfolio review: Ask for live products they have built and the results of those products delivered. This will help you know how proficient the partner is.

- Technology stack experience: If you have specific technology on which your software needs to be built, choose a partner having experience in that particular technology.

- Post-launch support model: As said earlier, insurance software is never finished. So, choose a partner with reliable post-launch support.

Final Take

Insurance software development is the foundation of how modern insurance businesses operate, sell, and grow.

At Helpful Insights, we build insurance software for carriers and InsurTechs across India, the USA, and the UAE through our software development services. So, if you are planning insurance software development, talk to our team and let’s walk through your project and how we can support it.