Key Takeaways

- RPA in finance eliminates the manual effort behind high-volume workflows by deploying software bots that operate within existing systems.

- The robotic process automation market in financial services is projected to reach $32.71 billion by 2030, up from $15.28 billion in 2026.

- Top RPA use cases in finance include accounts payable automation, invoice processing, bank reconciliation, payroll processing, fraud detection, KYC verification, and loan underwriting.

- Data security, employee resistance, and compliance drift are the most overlooked challenges in RPA implementation and require proactive planning.

- When combined with AI and machine learning, RPA evolves into intelligent automation, capable of handling judgment-based tasks, not just repetitive ones.

Finance teams worldwide are under pressure to deliver faster reporting, ensure tighter compliance, and handle transaction volumes that keep climbing. When those pressures hit manual workflows, errors accumulate, deadlines slip, and teams spend hours on tasks that should take minutes.

RPA in finance addresses this directly, deploying software bots to handle repetitive tasks like data entry and report generation by operating across your current financial systems, mimicking what a human would do, only faster.

The impact is measurable. According to Data Intelo, financial institutions using RPA have cut system integration costs by 50–60% compared to traditional methods. At that level of reduction, the savings don’t just improve efficiency. They reshape how finance budgets are allocated.

The gap between what RPA can do and what most finance teams have actually automated, however, remains wide. Most organizations start with automating one or two finance processes, get early wins, and treat that as the finish line. The real value of robotic process automation services in finance comes when it extends across accounts payable, regulatory reporting, reconciliation, and fraud detection simultaneously, where cumulative time and cost savings become genuinely transformational.

This guide covers RPA in finance use cases with real-world examples from Bank of America, Deutsche Bank, and JP Morgan, a step-by-step implementation roadmap, and honest answers on where RPA works and where it doesn’t.

What is RPA in finance?

In the finance industry, RPA stands for robotic process automation, which refers to software bots that handle high-volume, rule-based tasks like data entry, invoice matching, and reconciliation that would otherwise consume significant manual effort. These bots operate through existing systems, so there is no infrastructure overhaul involved.

The outcomes are consistent: faster processing, cleaner records, fewer errors, and compliance teams freed from repetitive checks before every reporting cycle. The market trajectory reflects this.

The RPA market in financial services is projected to reach $32.71 billion by 2030, reflecting that organizations are moving well beyond pilot programs and treating automation as a core part of how they run their operations.

How does RPA work in finance?

Mimics human actions

RPA bots extract data from PDFs, emails, and scanned documents and populate the right fields across your financial systems. Exactly as a human operator would, but without the manual effort or risk of keying errors.

Runs on predefined rules

Every action a bot takes is rule-driven. An invoice amount is checked against a purchase order approved if the figures match, flagged for review if they don’t. Simple logic executed consistently across thousands of transactions without variation.

Operates around the clock

Bots process transactions, run reconciliations, and generate reports continuously, which means High-volume periods like month-end close no longer create backlogs because the processing never stops.

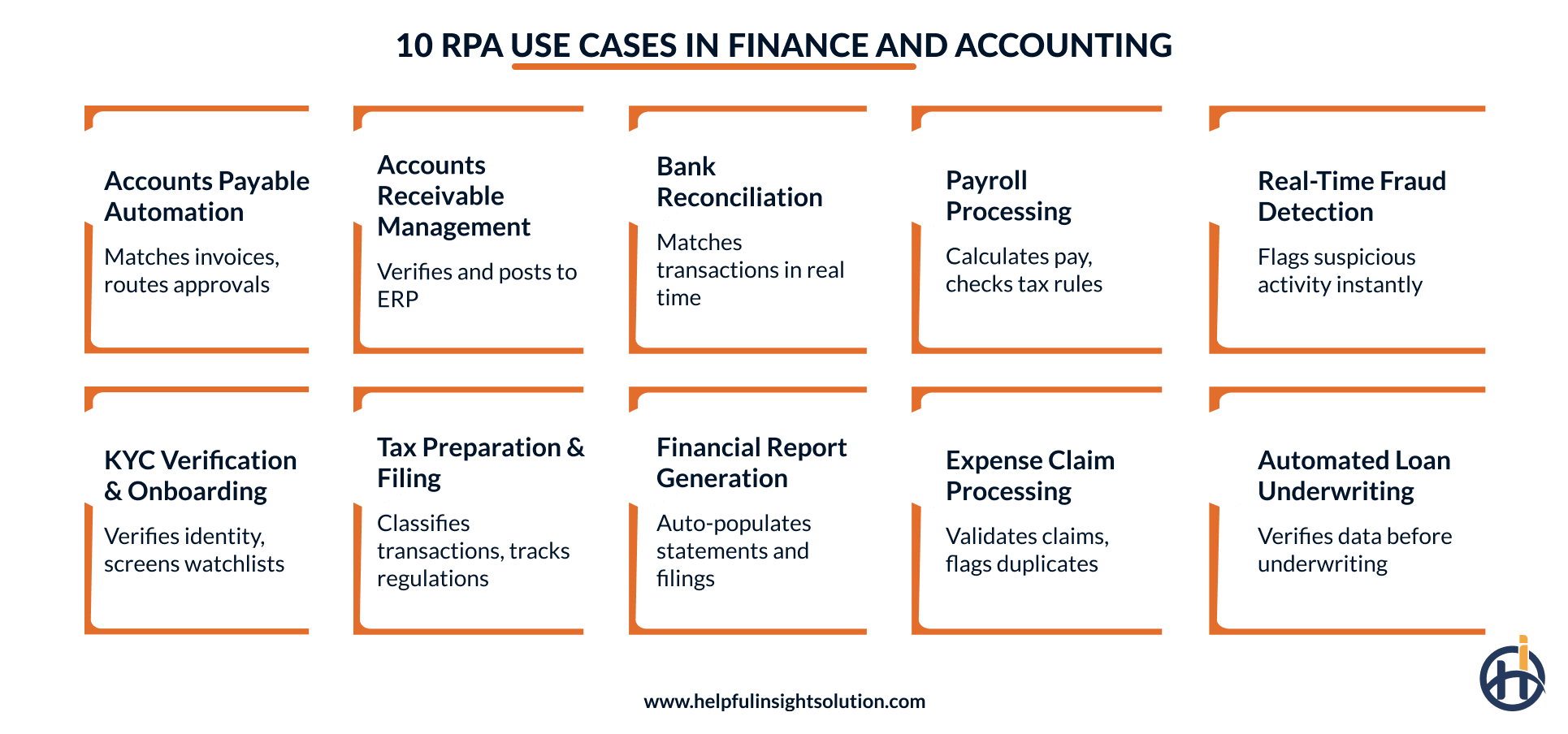

RPA use cases in finance and accounting

RPA use cases in finance and accounting cover more ground than most teams realise, from invoice processing and payroll to fraud detection and regulatory reporting. Below are the use cases delivering the most measurable results across banks, NBFCs, and finance functions.

Accounts payable automation

Manual accounts payable is one of the biggest time drains in any finance function and one of the clearest wins for RPA. Bots handle the entire cycle, extracting invoice data across PDF, email, and scanned formats, matching figures against purchase orders, routing through approval workflows, and scheduling payments once verified.

When combined with AI and ML, the capability extends further. Bots flag duplicate invoices, identify discrepancies before they escalate, and predict payment bottlenecks before they affect vendor relationships or payment terms.

Accounts receivable management

Processing invoices one by one across different formats is where finance teams lose hours they can’t get back. RPA bots pull the details, check them against purchase orders and delivery receipts, and push whatever matches straight into the ERP. No manual handling needed.

What does not match gets identified for someone to look at. The AR team doesn’t have to manually review every invoice and can start focusing only on the ones that genuinely need a decision.

Bank reconciliation

Reconciling bank statements manually is one of those tasks that looks simple until the volume hits. Every entry needs to be matched against internal ledgers, and a single misaligned figure can delay the entire close process.

Organizations running on existing financial software solutions can deploy RPA bots to continuously monitor transactions, reconciling them against bank statements in real time and producing exception reports for anything that doesn’t match.

Teams weighing a broader technology refresh alongside this often look at IT services in finance to see where automation fits into the bigger infrastructure picture.

The finance team receives a clean exception list rather than spending the close period buried in manual matching. Reconciliation that used to take days now completes in hours.

Payroll processing

Payroll involves pulling data from multiple sources like timesheets, attendance records, overtime logs, benefits deductions, and any error in that process affects people directly. RPA collects data across all those sources automatically, calculates final figures, and processes payments without manual data entry at any stage.

The same bots also cross-check payroll figures against regional tax regulations, comparing rates and deductions across each jurisdiction. Any discrepancy gets flagged automatically before disbursement, giving finance teams real-time to correct errors before disbursement.

Real-time fraud detection

Financial fraud moves faster than periodic manual review cycles can detect. Some fraud categories now trace 90% of new cases to cross-border payment loopholes and organised mule networks, schemes that evolve continuously and exploit the gaps between review windows.

RPA combined with AI agents monitors customer transactions and internal system activity around the clock, running payment details against verified risk databases and watchlists. Anything that looks suspicious is flagged immediately.

This is one of the clearest examples of AI in fintech in action; machine learning models get sharper with every case they process, and detection only gets better from here.

KYC verification and onboarding

Onboarding a new customer in financial services means moving through several steps one after another like document collection, identity checks, watchlist screening, AML database checks, and each one adds delay when a person has to handle it manually.

Every bit of friction along the way increases the chance of losing that customer before the onboarding completes.

Robotic process automation in finance handles the data collection and extraction from identity documents automatically, cross-referencing details against watchlists and AML databases as part of the KYC verification process, without anyone doing it manually.

Digital workers also create a complete audit trail of every verification step, reducing onboarding times from days to hours and ensuring every compliance step is documented.

Tax preparation and filing

Tax compliance is one of the most error-sensitive areas in finance. Different jurisdictions, constantly shifting regulations, and the sheer volume of data that needs to be accurately classified before a single return gets filed create conditions where manual processing is inherently risky.

RPA bots extract financial data across systems, ensure every transaction sits in the right tax category, and handle return population without figures being keyed in separately. Beyond filing, bots track regulatory changes across jurisdictions and flag anything that could alter the company’s tax position before the next cycle closes. For multinational finance teams managing filings across multiple regions, this is particularly valuable.

Financial report generation

Month-end and year-end close each bring pressure to produce accurate reports across multiple financial statements, often within tight deadlines and with figures drawn from systems that don’t naturally talk to each other.

RPA pulls figures from across the business, validates them against predefined rules, and populates report templates automatically.

This covers standard financial statements such as balance sheets, income statements, and cash flow reports. It also handles regulatory filings like Suspicious Activity Reports (SARs), where accuracy and consistent formatting are non-negotiable. For teams already running on modern FinTech software platforms, RPA compatibility is typically built in.

Expense claim processing

Expense claim processing is one of the most consistent high-volume use cases for RPA in finance. The volume never slows, regardless of team size or business cycle. Bots validate submitted claims, verify figures against company spending policies, identify duplicate entries, and move approved claims directly to reimbursement. The finance team steps in only when a claim genuinely requires a judgment call.

As claim volumes grow, the process does not break down or slow down. A team processing 5,000 claims runs the same workflow as one processing 500, without additional headcount, without proportionally more time, and without proportionally more errors.

Automated loan underwriting

Loan underwriting requires assessing multiple data sources before a credit decision can be made. Credit history, income documents, tax transcripts, and employment records are each pulled from different systems and verified against lending criteria.

RPA bots and agentic AI automate that entire data-gathering and pre-assessment process, flagging incomplete or inconsistent information. This blend of rule-based bots and judgment-aware AI is a good example of where AI in business process automation is heading next.

By the time a file reaches an underwriter, it is already completed and verified. Timelines that used to stretch across several days now get wrapped up within hours.

Which finance processes are not suitable for RPA?

In finance, robotic process automation works well within defined rules and predictable data. Certain processes, however, depend on human relationships or judgment calls that shift depending on context.

Deploying bots where they don’t belong doesn’t just fail; it actively creates problems that are harder to manage than the manual process they replaced.

Here are the finance processes where RPA is not the right fit.

Strategic financial planning

Strategic financial planning (FP&A) relies on challenging assumptions, interpreting ambiguous market signals, and making judgment calls that shift based on context no bot can read.

Each planning cycle carries its own mix of pressures such as shifting business performance, macroeconomic conditions, board priorities, and the kind of thinking that simply can’t be reduced to a fixed set of rules. This is where human expertise remains irreplaceable.

Complex vendor and contract negotiations

Vendor and contract negotiations depend on things that never make it into a dataset. A supplier pushes back, terms shift, and the person across the table reads the room and adjusts in real time. RPA use cases in finance and accounting cover a lot of ground, but this is not one of them.

Bots cannot read tone, detect hesitation, or decide when holding firm makes more sense than compromising. That kind of judgment comes from experience and relationship history, not rule-based logic.

Unstructured document processing

Unstructured documents are common in finance. Handwritten forms, free-form emails, irregularly formatted PDFs, and contracts with non-standard layouts. RPA was built for consistency: same fields and format every time. The moment a document breaks that pattern, a standard RPA bot either misreads it or flags the entire batch for manual review. Structured data is where RPA performs.

This is where intelligent document processing (IDP) and AI-powered OCR become relevant; they can handle unstructured inputs that pure RPA cannot. If your finance function handles significant volumes of unstructured documents, a combined IDP and RPA approach is worth considering rather than RPA alone.

Real-world examples of RPA in finance and banking

Market projections tell one part of the story. What global banks and financial institutions have actually achieved with robotic process automation tells the rest. The following examples come from institutions that have moved well beyond experimentation, building RPA into how they operate at scale across front, middle, and back-office functions.

Bank of America

With operations spanning retail banking, wealth management, and corporate finance, Bank of America needed automation that could work across functions. They deployed RPA bots across front, middle, and back offices to connect existing legacy systems, reduce manual workload, and drive measurable gains in cost efficiency and productivity.

The bank developed Erica, an AI-powered virtual assistant primarily for customers through the Bank of America mobile app. Over time, an internal version was rolled out for employees, helping with tasks like password resets, HR queries, and IT support. That internal rollout alone reduced IT service desk volume by over 50%.

Erica is also a useful reference point for any institution planning to develop fintech app experiences, since it shows how automation and customer-facing design can work together rather than as separate projects.

What makes Bank of America’s approach worth studying is that they did not automate isolated processes; it built automation as a continuous operational layer across the institution.

Deutsche Bank

As one of Europe’s largest banks, Deutsche Bank identified that corporate clients handling back-office operations were losing significant time to manual data extraction, document handling, and reconciliation, processes that were high-volume, consistent, and exactly what RPA is built for.

The bank developed an RPA-powered data processing and reconciliation solution capable of handling large document volumes simultaneously. The results are specific: reconciliation time dropped from two to three days to under an hour, and the solution saves up to 60–80 hours of manual work per month per team. For an institution operating at Deutsche Bank’s scale, the cumulative time recovery across functions is substantial.

JP Morgan

JP Morgan is one of the largest banks in the world, and with that comes an enormous volume of legal documents, client onboarding requests, and treasury operations that cannot afford delays or manual errors. The bank deployed RPA to address exactly those areas.

Bots read legal contracts, process documents, and handle treasury operations that previously depended on manual clearing workflows. Client onboarding has become measurably faster, and the integration of clearing infrastructure now runs without requiring clients to build new operations-driven processes on their end, a detail that directly improves the client experience.

Key benefits of RPA in finance industry

Deploying RPA and AI in banking brings measurable improvements across operations. Lower costs, fewer processing errors, stronger compliance, and teams that spend less time on repetitive work and more time on decisions that actually move the business forward.The benefits of RPA compound as automation scales.

Lower operational costs

A significant portion of finance work is rule-based and repetitive, and human processing of that work costs more than it needs to. RPA reduces that cost by deploying bots on the fixed-rule tasks, freeing up budgets that organizations can redirect toward higher-value activities.

In markets like the US and UK, industry data puts the cost of a bot at roughly one-tenth that of a full-time employee, which makes the ROI case pretty easy to build for high-volume finance functions.

Stronger regulatory compliance

In finance, compliance gaps rarely surface until an auditor finds them. RPA services for accounting close those gaps by running compliance checks continuously and maintaining detailed audit trails of every transaction processed. Nothing gets missed between reporting cycles because the monitoring never stops.

Frameworks like SOX, GDPR, and PCI DSS all call for documentation and RPA generates it automatically as a byproduct of normal operation, not as some extra compliance step tacked on afterward.

Faster ROI than traditional software

Traditional finance systems overhauls involve long implementation timelines and costs that can take years to recover. RPA bypasses that cycle entirely by operating within existing systems. Most organisations begin seeing measurable returns within weeks of deployment, rather than waiting through multi-year development timelines.

For finance functions with limited appetite for disruptive change, this is one of RPA’s most practical advantages.

Better customer experiences

Customers don’t see back-office processes. They notice the results like loan approvals that take a week, account openings that require follow-up calls, dispute resolutions that drag across multiple touchpoints. Each of those delays traces back to a manual processing step that RPA can automate.

Removing those steps means faster approvals, shorter wait times, and resolutions that complete without repeated customer contact. In a market where switching costs are lower than ever, the customer experience impact of operational speed is a direct competitive factor.

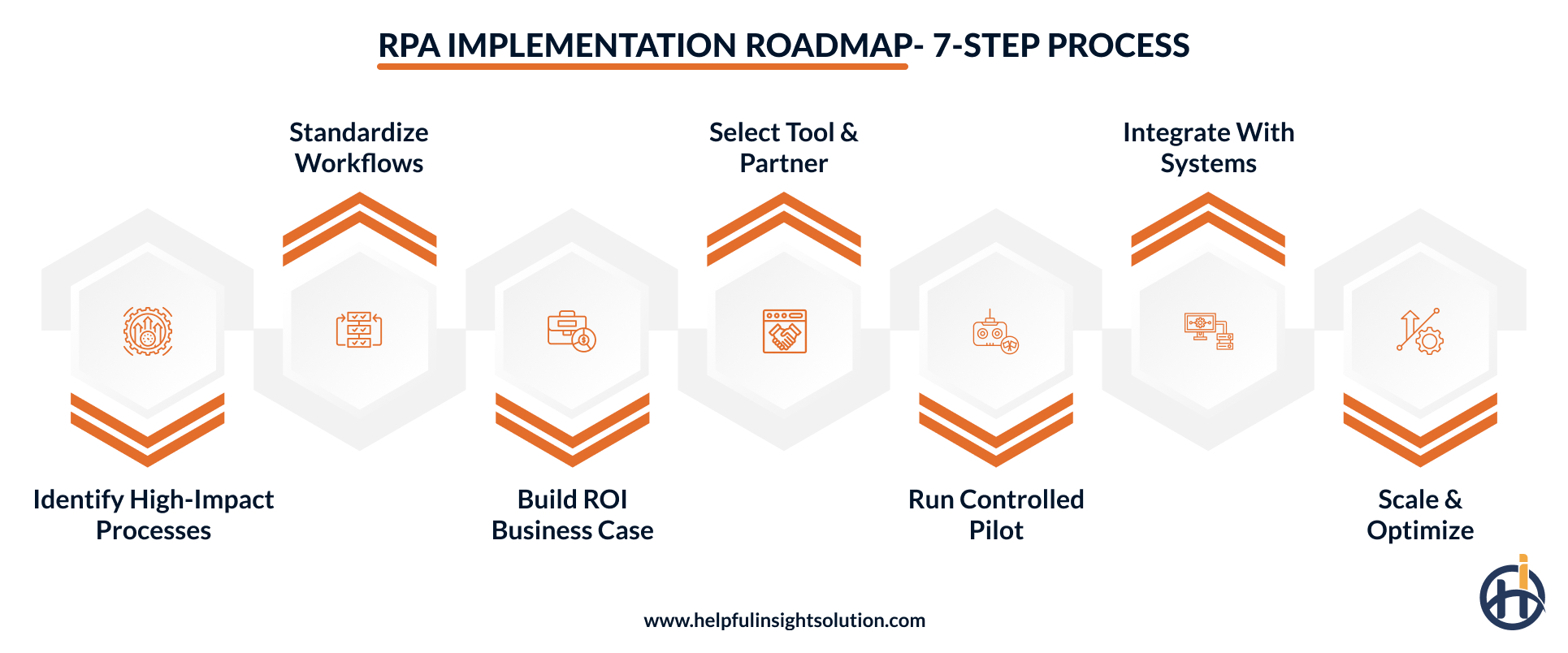

How to implement RPA in finance: A step-by-step roadmap

Successful RPA implementation in finance depends on choosing the right processes, right tools, and rolling out automation in planned stages rather than attempting to automate everything at once.

The groundwork matters because organizations that skip the planning stage are usually the ones dealing with bots that work in isolation and never scale.

Let’s have a look at the steps involved in successfully implementing RPA in finance and banking.

Identify and prioritize high-impact processes

Not every finance process is worth automating first. Focus on tasks that run on fixed logic, occur frequently, and take disproportionately long compared to their complexity. Expense management, report generation, bank reconciliation these are the processes worth automating first.

They’re repetitive, high in volume, and deliver measurable results quickly and build internal confidence in the program.

Standardize workflows before automating

A bot built on an inconsistent workflow will produce inconsistent results. Before RPA touches any process, every step needs to be mapped, redundant actions removed, and decision rules clearly documented.

Data formats need to be consistent across all inputs, and exception handling needs to be defined upfront rather than discovered during deployment.

Build a business case with ROI projections

Translate the processes identified in step one into concrete financial figures. How many hours does each process consume monthly? What does an error cost to fix? What is the current processing cost per transaction?

A business case built around those specific numbers is what gets a program funded and keeps it funded when questions arise after deployment.Include projected payback period; most well-scoped RPA implementations recover their cost within 6–12 months.

Select the right RPA tool and partner

Platform selection depends on the complexity of your existing systems, the volume of processes being automated, and the internal technical capacity available to manage the deployment. Leading platforms include UiPath, Automation Anywhere, and Blue Prism, each with strengths in different finance environments.

The implementation partner matters as much as the platform itself. Choose a partner who knows the compliance requirements like SOX, PCI DSS, AML, and can actually work with your existing systems. Get that right and deployment goes faster, with fewer of those configuration issues that only show up once you’re live.

Run a controlled pilot and measure results

Select one well-defined finance process, run it under live conditions, and measure what actually changes. Processing time, accuracy rates, exceptions flagged, cost per transaction. Compare those numbers against the baseline figures from the business case. If results match projections, the program has its green light to scale. If they do not, this is the stage to identify why and fix it before more processes get added to the automation pipeline.

Integrate RPA with existing financial systems

One of the practical advantages of robotics process automation in finance is that bots connect to existing systems through the user interface without requiring backend access or infrastructure changes. ERP platforms and accounting databases can all be connected without disrupting what is already running.

Here pre-built connectors exist for your platform (UiPath, Automation Anywhere, and Blue Prism all maintain extensive connector libraries), use them. They reduce development time significantly and come with security configurations already validated for financial environments

Scale, monitor and continuously optimize

Scaling RPA in finance is an ongoing discipline, not a one-time decision. Once results from the pilot are consistent, expand to additional processes but maintain performance tracking as you go.

Monitor bot utilisation, exception rates, processing accuracy, and system changes that could affect bot behaviour. As regulations evolve or internal systems are updated, bot logic needs to be reviewed and adjusted accordingly.

The finance functions that extract the most long-term value from RPA treat it as a managed operational capability, not a deployed tool that runs unattended indefinitely.

RPA implementation challenges in finance and how to overcome them

A lot of organizations invest in RPA and AI development services, expecting smooth deployment, but run into unexpected problems instead. Legacy system complexity, change resistance, and poor process selection are the most common. Fortunately, none of these are unavoidable when the right strategies are in place.

Data security and privacy risks

RPA bots work across ERPs, customer databases, and payment systems, so the same level of access that makes them productive also makes them a target if not properly secured. Poorly managed credentials or overly broad access permissions create vulnerabilities that cybercriminals actively look for and put valuable data at risk.

The solution

Use encrypted credential vaults, never hardcode access details into scripts. Limit what each bot can reach to only its specific task and audit those permissions regularly.

Automating broken processes

Automating a broken process doesn’t fix it, it accelerates the breakage. When a workflow has gaps, unclear decision points, or too many exceptions, deploying a bot makes those problems harder to catch and harder to fix.

The solution

Map and standardise every workflow before automation begins. RPA developers should document clear decision rules and define how exceptions get handled.

Employee resistance to change

Finance professionals who have spent years mastering manual workflows do not always welcome automation,particularly when the messaging around it is poorly handled. Concerns about job security and unfamiliar technology create friction that no deployment plan can afford to ignore, regardless of how strong the business case looks on paper.

The solution

Bring employees in early, not after deployment. Show them what changes and what does not. Industries like RPA in insurance handled workforce transition found that upskilling programs focused on higher value work, not just tool training. Teams that understood automation was taking over repetitive work, not their careers, adapted faster.

Compliance and governance gaps

As automation expands across finance functions, governance gaps quietly develop. RPA bots making unauthorized process changes or operating outside defined parameters introduce compliance risks that traditional monitoring processes were never designed to catch.

The solution

Adopt a compliance review process that runs alongside bot performance monitoring. Frameworks like SOX, FINRA, and BSA set the standards. Bot logic should be tested against updated requirements every time regulations shift, not annually.

Make your finance processes future-ready with Helpful Insight RPA implementation expertise

RPA in finance is not a future investment anymore. It is a present one, and the organizations adopting it are already seeing the difference in their processing times, compliance records, and operational costs.

What separates finance functions that scale cleanly from ones that struggle is the decision to start, pick the right processes, and build the program properly. That is exactly where Helpful Insight comes in.

We are a trusted robotic process automation company helping banks, investment firms, and lending institutions identify the right processes to automate, build deployment roadmaps that hold up under real conditions, and scale automation beyond the pilot stage. Many of these engagements grow into larger projects too, since the systems bots plug into often need work of their own, which is where our experience as a financial software development company comes in.

Our implementations have helped finance teams reduce processing times by up to 30% to 40% and cut manual errors significantly across their core workflows.

If automating your finance operations is on your roadmap or if you’re still figuring out where to start, connect with our RPA experts, and we’ll give you a clear, prioritised place to begin.

FAQs

Implementing RPA for a single well-defined finance process typically costs between $15,000 and $60,000. Scaling across multiple functions can range from $60,000 to $150,000 or more, depending on scope. The main cost drivers are system integration complexity, bot configuration, and ongoing maintenance. Organisations that have already standardised their workflows before engagement typically see lower implementation costs and faster deployment.

A single well-defined finance process typically takes 4–10 weeks to implement. Enterprise-wide deployments covering multiple functions can run 4–9 months or longer, depending on system complexity and the number of processes in scope. Organisations that standardise workflows before deployment consistently complete implementations faster than those that don’t — often by several weeks per process.

RPA in finance and banking is used across a wide range of functions like KYC verification, invoice processing, expense report auditing, and loan processing. The common thread across all of these is high-volume, rule-based work that does not require human judgment at every step.

RPA follows fixed rules to handle repetitive tasks like data entry, but AI goes further by learning from data, recognizing patterns, and making decisions in situations that do not follow a predictable script. The two work best when deployed together rather than treated as alternatives.

The dominant trends in RPA for finance in 2026 are hyperautomation, agentic AI integration, and intelligent document processing (IDP). Bots aren’t just running repetitive, rule-based tasks anymore. Paired with AI, they’re starting to handle workflows that actually require judgment.

Cloud-based RPA, also known as RPA-as-a-Service, is gaining ground too, alongside natural language processing for unstructured documents. RPA platforms are getting tighter with AI-powered analytics. The shift from standalone RPA to an integrated automation platform combining RPA, AI agents, and orchestration tools is where most enterprise finance deployments are heading.