Key Takeaways:

- The FinTech app that targets a specific financial problem for a specific user has a much stronger foundation than one built around a broad general idea.

- Not all FinTech apps are built the same way. Payments, lending, budgeting, and insurance apps each come with different technical and regulatory requirements.

- FinTech app development costs start from $25,000 for a basic product and can reach $150,000 or more for AI-powered platforms.

- An MVP takes 3 to 6 months to build and validates the concept with real users before full-scale development begins.

- Choosing between build, buy, and BaaS early determines your timeline, budget, and how much control you retain over the final product.

Most financial apps in production today were designed for a different era. Customers now expect instant transfers, real-time fraud alerts, and frictionless mobile experiences yet most banks still operate on infrastructure that was never designed to deliver them. This is exactly the problem FinTech app development solves and businesses that invest in it now are already seeing measurable returns.

The market reflects this shift, with the FinTech app industry projected to be valued at $500.9 billion in 2026 and projected to reach $1,026.1 billion by 2032. According to the Market.us report, already, 75% of global consumers use FinTech-powered services for payments and transfers.

There is, however, a side to building a FinTech product that market projections rarely capture: how much genuinely goes into making one work at scale. Compliance requirements, security layers, infrastructure decisions, and integration complexity are the variables that separate products that perform from ones that struggle after launch.

FinTech businesses that approach these decisions carefully tend to build platforms that retain users, reduce internal friction, and scale without structural problems.

From app types, core features, development processes, costs, to compliance, this guide covers everything you need to build a FinTech app the right way.

What is FinTech mobile app development?

FinTech app development is the process of building mobile applications that deliver financial services such as payments, lending, insurance, investing, and digital banking.

It includes everything from UI/UX design and backend architecture to security, compliance, API integrations, and deployment- the same core mobile app development process, with financial-grade requirements layered on top.. For financial businesses, the way these applications are developed directly impacts scalability, security, and customer experience.

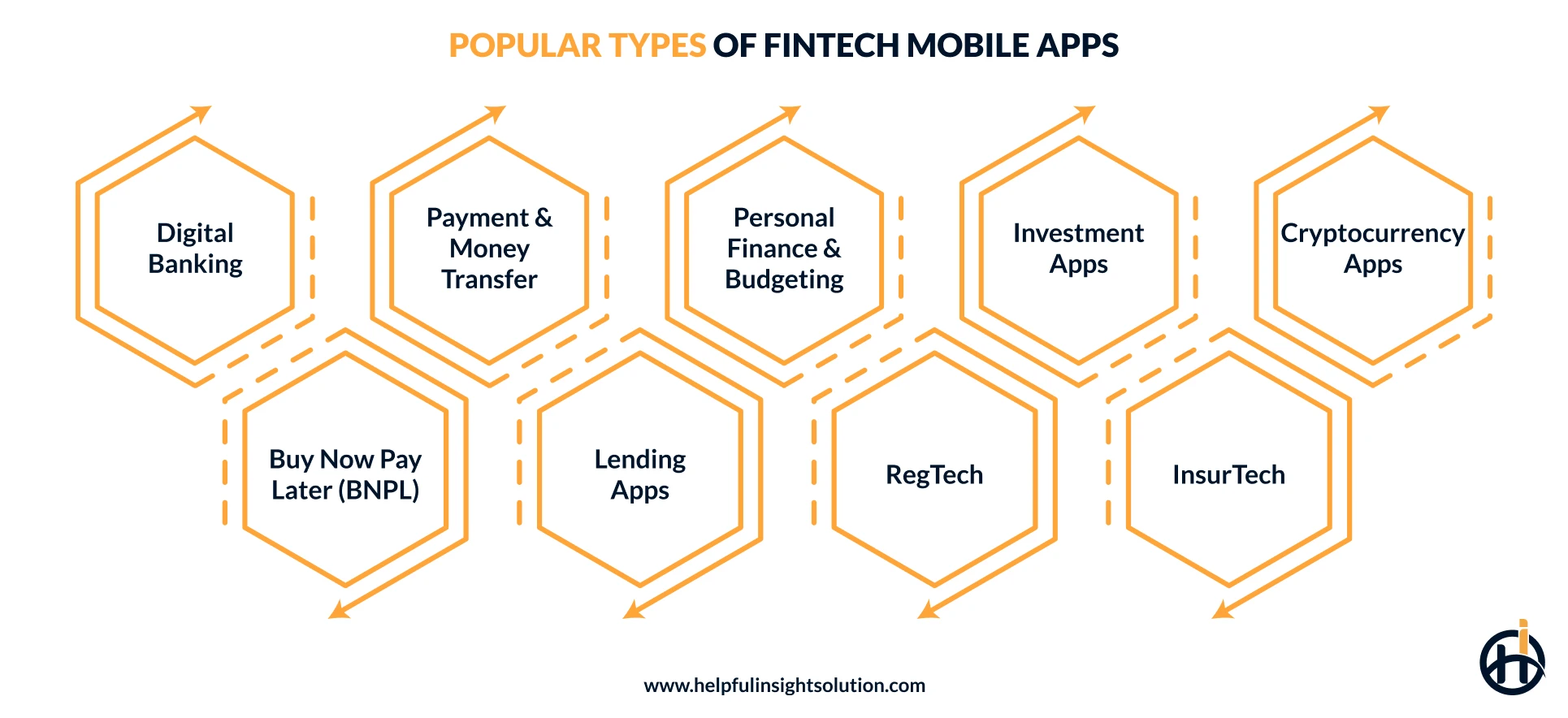

Types of FinTech mobile apps with real-world examples

FinTech covers a surprisingly wide range of products, each solving a different financial problem. Someone applying for a loan on their phone, a business automating payroll, and an investor tracking portfolios in real time each has an app, just built around very different needs.

In this section, let’s take a look at the different types of FinTech apps.

Digital banking and neobank apps

Banking used to mean branch visits, paperwork, and waiting. Neobanks and digital banking apps changed that, not by improving the old model, but by replacing it. Everything from account opening to transfers happens on mobile, with none of the overhead traditional banks carry.

The user experience is noticeably different too. Fewer fees, faster processing, and interfaces actually designed around how people use money today rather than how banks prefer to manage it.

Real-world example

Chime is a U.S.-based neobank app that offers fee-free banking with no minimum balance requirements. Its standout feature is early direct deposit, where users receive their paycheck up to two days before the official pay date.

Payment and money transfer apps

Whether paying back friends or sending money to family in another country, these used to involve multiple confusing steps. Payment apps stripped most of that process away, making transfers something that takes seconds rather than days.

What made this category stand out was not just speed. It was the removal of friction at every step, no branch hours and no waiting period that made simple transactions feel unnecessarily complicated.

Real-world example

Venmo was originally built for splitting costs but has since grown into a full payment platform used by over 90 million users. If you’re evaluating the payment app landscape more broadly, our comparison of PayZapp alternatives and top payment apps covers ten more platforms worth studying.

The best part about this secure FinTech app is that transactions show up as shared activity, which has become a defining part of how younger users engage with money transfers daily.

Personal finance and budgeting apps

Many people struggle to manage their personal finances; they have a rough idea of where their money goes. Budgeting apps replace that rough idea with something more honest: actual numbers and a clearer picture of habits that are easy to overlook when you are just checking balances occasionally.

Real-world example

YNAB (You Need A Budget) is a highly popular personal budgeting app that works on a simple principle: plan your money before you spend it, not after. Every dollar gets assigned a category in advance, which removes a lot of the guesswork around finances. In fact, 90% of users say their financial situation improved after starting with YNAB.

Investment apps

Investment and wealth management apps are tools that give users direct access to financial markets from their phones, covering everything from stock trading and ETF investing to portfolio tracking and crypto management.

For a long time, that access simply did not exist. Platforms were complicated, fees added up quickly, and the whole process assumed prior knowledge. Mobile investment apps changed that significantly.

Real-world example

Robinhood is a trading app that made investing accessible by removing commissions entirely across stocks, ETFs, options, and crypto. Users get custom price alerts, 2-factor authentication, and direct access to a chat associate for help whenever needed.

Cryptocurrency apps

Crypto apps are basically a type of mobile application that handles buying, selling, trading, and storing digital assets. Most include real-time market data and portfolio tracking.

The better ones offer wallet management without requiring users to understand how wallets actually function. That accessibility has driven serious market growth.

Real-world example

Coinbase built its user base around simplicity. It supports hundreds of digital assets within one interface and includes an educational feature where users earn small crypto amounts by completing short lessons. For first-time investors who hesitate because they do not understand what they are buying, that feature removes a real barrier.

Buy now pay later (BNPL) apps

BNPL apps stepped in where credit cards fell short, making small, short-term purchases more manageable without the need for a traditional credit application process. Users split a payment into installments, usually interest-free, with approval decisions that take seconds.

The payment schedule is visible from the start, which is part of why adoption grew quickly among younger users.

Real-world example

Klarna app lets users split purchases into four interest-free installments, pay within 30 days, or choose a longer repayment plan. It works across thousands of retailers and includes a standalone shopping app where users manage payments and track orders. Moreover, the platform offers up to 12% cashback at select stores, making it more than just a payment tool.

Lending apps

Getting a personal loan from a bank used to mean paperwork, branch visits, and waiting days for a decision. Lending apps cut through that entirely. Users connect their financial data through the app, eligibility is assessed within minutes, and credit products, including personal loans and cash advances, become accessible.

Real-world example

MoneyLion is one of the most widely used instant cash advance apps, where users can access interest-free cash advances, apply for personal loans, and monitor their credit score without switching between platforms. For a closer look at how MoneyLion compares to other cash advance platforms, see our roundup of the best apps like Dave.

It is built around users who need greater financial flexibility. The application process is simple, with no branch visits or physical paperwork involved at any stage.

RegTech apps

These types of smart finance apps handle the compliance side of running a financial product, including identity verification, fraud detection, KYC checks, AML monitoring, and audit reporting. For financial institutions managing these requirements manually, the time and operational cost can increase quickly. RegTech tools automate much of this process.

Real-world example

Onfido is an AI-powered identity verification platform that financial institutions use to confirm users are who they claim to be during onboarding. It runs AI-driven document scans and facial biometric checks in seconds. Banks, lending platforms, and FinTech startups use it specifically because it meets compliance requirements without slowing down the user experience.

InsurTech apps

Insurance has been one of the slowest industries to digitize. InsurTech apps changed that by bringing policy purchase, management, and claims filing into a single mobile interface. Users who were already managing banking and payments on mobile had little tolerance for an industry still running on manual processes and long turnaround times.

What makes these apps technically demanding is the depth of domain logic involved, from policy rules to claims workflows, areas where insurance software development requires a different level of precision than general app builds.

Real-world example

Lemonade helps with policy sign-ups and claims entirely through the app. Users get renters, homeowners, pet, or life insurance in minutes. Claims are reviewed through an automated process and, in some cases, paid out within seconds.

How do FinTech apps make money?

Investing in FinTech mobile app development is one decision, but figuring out how it generates revenue is another. Most successful FinTech products do not rely on a single income stream. They layer multiple monetization strategies depending on the user base, transaction volume, and the financial product they are built around.

Some of the most popular monetization strategies are:

Subscription model

With the subscription model, users pay a fixed recurring fee to continue accessing the premium features of the app. The model works best when the core product solves a problem users face regularly.

The YNAB app charges annually and retains users because the budgeting system requires ongoing engagement.

Transaction fees

FinTech platforms that process payments earn on every transaction that moves through them. The fee is usually a small percentage of the transfer amount, sometimes combined with a flat charge.

PayPal applies this model across personal and business transactions. Volume is what makes this model work. A fraction of a percent means very little on one transaction and a great deal across millions.

Interchange fees

Every time a user swipes a card linked to a FinTech app, the merchant pays an interchange fee, typically around 1% to 3.5% of the transaction value. The card network passes a portion of that to FinTech.

Chime earns substantially through interchange, making it one of the most consistent revenue streams in the industry.

Interest on loans and credit

Interest income is one of the oldest revenue models in finance and has not moved away from it. Apps that offer personal loans, credit lines, or installment payments charge interest on amounts not repaid within the interest-free window.

Some merchants absorb the interest cost to offer users a zero-percent option, while the platform earns on the rest.

Must-have core features every FinTech app needs

Digital finance apps that struggle usually have one thing in common: they were built with too many features and not enough focus. The core has to be secure, fast, and reliable first. Everything else comes after.

Dedicated developers who have built FinTech products before know which features actually work and which ones just add unnecessary complexity. Therefore, you can take their guidance in selecting the right feature set.

Let’s have a look at the FinTech app features.

Secure user authentication

Most people never think about how their financial app handles security until something goes wrong. Integrating secure authentication means users are protected through biometric logins, two-factor authentication, and encrypted sessions working together. No single method is enough on its own.

Digital KYC verification

Regulatory compliance during onboarding used to mean slow, manual identity checks that frustrated users before they ever experienced the product. Digital KYC changed that. Document scanning and facial recognition handle verification in minutes.

Real-time transaction tracking

This feature helps remove the blind spot, as every movement in the account shows up instantly. Users catch unauthorized activity early, understand their spending in real time, and do not need a monthly statement to know where things stand.

AI-powered fraud detection

AI in banking apps helps learn each user’s normal spending behavior and flags anything that breaks from that pattern immediately. Suspicious transactions get blocked at the point of attempt. The system also gets sharper over time, because every transaction it processes adds to the behavioral data it learns from.

[Learn more about how AI agents in finance are transforming fraud detection ]

Multi-payment integration

Different users transact differently. One user depends on UPI, while another expects crypto or wallet support. Restricting options at checkout is where FinTech apps quietly lose users. The wider the payment support, the wider the audience the app can realistically serve. So, you should definitely add this functionality.

Personal finance dashboard

A personalized dashboard turns raw transaction data into something users can actually understand, like spending breakdowns and investment performance. Users can see their full financial picture and make better decisions.

Smart budget management

Smart budget management lets users define spending limits by category and tracks progress automatically against real transaction data. When a limit is approached, the user gets notified. That kind of visibility changes spending behavior in ways a manual spreadsheet never could.

Instant money transfers

Waiting two to three business days for a transfer to clear is something that can frustrate users. Peer-to-peer payments, bill settlements, and cross-border transfers in seconds, not days, with an app. The mobile banking solution that gets this right retains users.

Offline functionality

Network issues do not warn users before they happen. Offline functionality means cached balances, recent transaction history, and queued payments are still accessible. When connectivity returns, everything syncs automatically.

Push notifications and alerts

A well-timed alert does more for user engagement than most features built into a FinTech app. Users want to know when a payment clears, when a balance drops, or when something suspicious appears on their account.

Too many notifications, and users switch them off entirely, which defeats the purpose of having them. So, indeed, this is a must-have feature.

Build vs. buy vs. BaaS: Which FinTech app development model is right for you?

Build from scratch, buy a ready-made solution, or go with a BaaS provider. The right choice depends on what the product actually needs, and each option comes with a different trade-off between speed, control, and long-term cost. Product type, available budget, and time to market all push the decision differently. Moreover, it also affects how much the product can grow and change over time.

Let’s explore all three FinTech application development approaches to help narrow it down for your specific FinTech project.

Build (custom development)

Custom FinTech app development simply means building the product entirely from scratch. Every feature, every user flow, and every architectural decision stays in your hands.

It is the highest control option available, but also the most resource-intensive. Teams that select this approach need developers who have built financial software before, a solid architecture plan, and a realistic timeline.

Pros

- Full product and UX control

- No vendor dependency or licensing restrictions

- Deep customization at every level

- Better long-term scalability options

Cons

- High upfront development cost

- Longer time-to-market timelines

- Requires ongoing maintenance

When to choose

- Your mobile app requires highly specific custom functionality.

- Long-term IP ownership is a non-negotiable requirement.

- The product cannot function within third-party platform limitations.

- Product differentiation is a core priority.

Typical timeline

MVP: 3 to 6 months

Full product development: 9 to 18 months or more depending on complexity

Buy ( off-the-shelf solutions)

Buying means licensing a ready-made platform that already exists and has been tested in the market. It gets the product live faster and at a lower initial cost than building from scratch.

The platform works within the boundaries the vendor has already defined, and scaling or modifying it later can become complicated quickly.

Pros

- Lower initial implementation costs

- Faster deployment and launch

- The vendor handles updates and maintenance

- Predictable subscription-based pricing models

Cons

- Limited customization flexibility

- Vendor lock-in risk over time

- Difficult legacy system integrations

- Compliance and security posture tied to vendor decisions

When to choose

- Speed to market is the primary business priority.

- Basic features satisfy business requirements.

- Long-term customization requirements are minimal or secondary.

- The business needs a working product to validate the market first.

Typical timeline

MVP: 1 to 3 months

Full product development: 3 to 6 months, depending on customization needs

BaaS (banking-as-a-service)

BaaS is one of the increasingly adopted models that allows businesses to offer financial services directly within their own products through API connections to a regulated banking infrastructure.

Payment processing, lending, and account management become accessible without the need to build financial infrastructure. The BaaS provider handles compliance and security while the business focuses on creating the product experience around it.

Pros

- No banking license required

- Lower infrastructure investment overall

- Quick FinTech product launches

- Flexible API-driven architecture support

Cons

- Less control over core financial infrastructure

- Limited backend operational visibility

- Provider pricing can increase at scale

When to choose

- The business wants to add financial features to an existing product.

- If you need banking features without holding a full banking license.

- Limited resources for banking operations management.

Typical timeline

MVP: 3 to 8 weeks

Full product development: 2 to 4 months depending on integration complexity

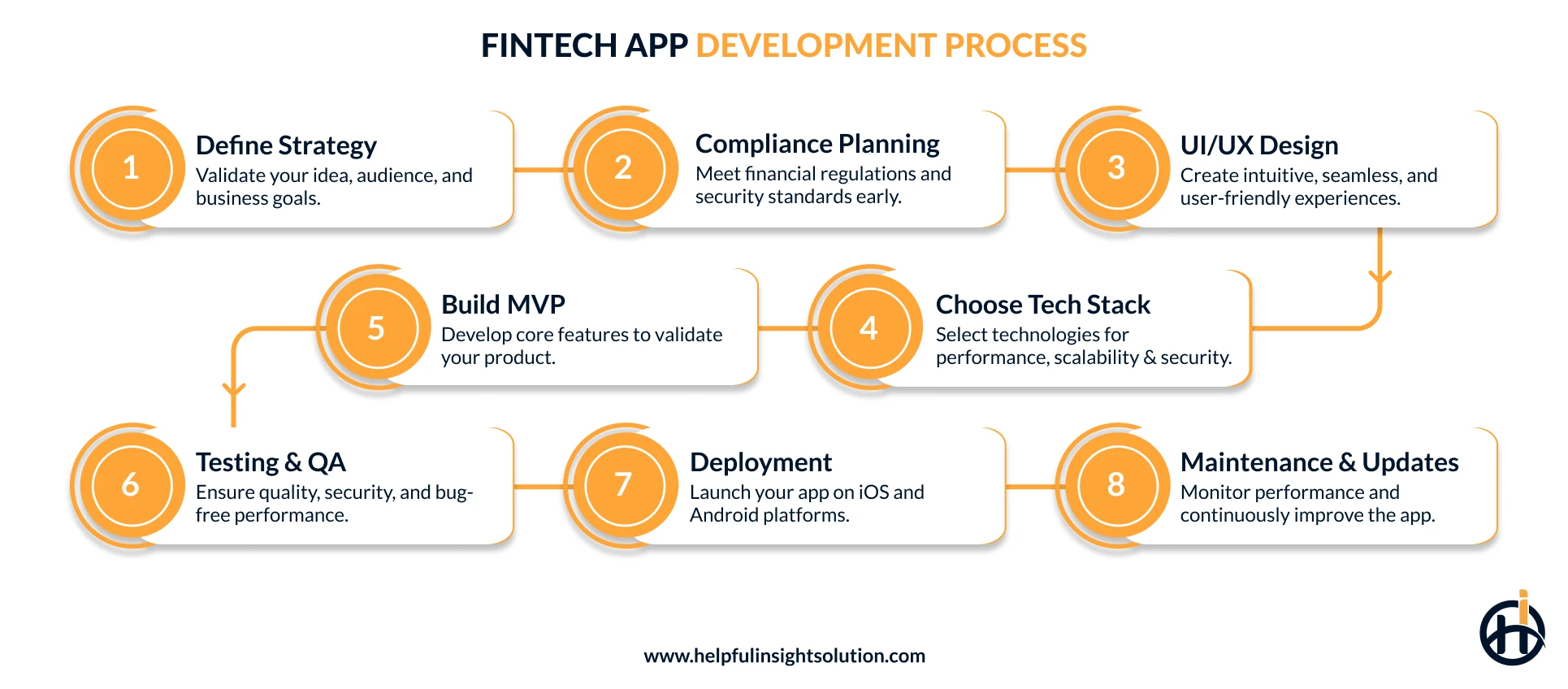

How to build a FinTech App: Complete development process

Every FinTech product starts as an idea. What separates successful launches from products that struggle later is the structure behind the development process. Compliance, architecture, UI/UX design, and testing all play a critical role in building secure and scalable financial applications.

Let’s have a look at the stages involved in building a finance app.

Define your niche and product strategy

Jumping into development without a defined niche is where most FinTech projects go wrong. The FinTech market is broad and competitive. An app without a specific focus ends up trying to serve everyone and does that job poorly. Before making technical or architectural decisions, the product strategy must be clearly defined.

Key questions that need to be answered early include:

- What financial problem does the app solve?

- Who is the target audience?

- Which market or geography will the product launch in first?

- What gap does the platform fill in the existing market?

Establishing this foundation early makes the entire FinTech app development process more focused, scalable, and easier to execute.

Meeting compliance requirements

FinTech operates in a heavily regulated environment, which means compliance cannot be treated as a later-stage consideration. Apps dealing with financial data and real money transactions have legal obligations that vary by region, product type, and target audience.

Getting compliance wrong is not just a regulatory risk, it directly impacts customer trust and platform credibility.

Depending on the financial product and market, FinTech apps typically need to comply with:

- KYC and AML regulations

- GDPR, CCPA, and regional data privacy laws

- PCI DSS standards for payment data security

- Licensing and regulatory requirements specific to the financial category

Plan UI/UX design and user flow

In this stage, the UI/UX design team creates wireframes, user flow maps, and interactive prototypes that define how users will interact with the application.

FinTech and mobile banking apps often lose users at the interface level. Complex navigation, unclear workflows, or too many steps during transactions can quickly impact user trust and retention.

Getting this stage right before coding starts is very important. Fixing a broken user flow discovered mid-development costs far more to fix than one caught at the wireframe stage.

Choose the right tech stack

The technology stack is something you cannot compromise on in FinTech app design and development. Poor architectural choices may not create immediate issues, but they often become visible later when the platform struggles to scale, handle high transaction volumes, or integrate efficiently with banking systems and payment providers.

The stack determines how well the app handles real transaction volumes, how cleanly it connects with banking APIs, and how secure the infrastructure actually is under pressure.

Cross-platform frameworks like React Native and Flutter are commonly used for FinTech applications targeting both iOS and Android. Node.js, Django, and Ruby on Rails are the backend options teams most commonly work with, depending on product complexity. PostgreSQL, MongoDB, and MySQL handle the database layer.

Selecting the right combination is not a generic technical decision. It depends on factors such as transaction volume, infrastructure scalability, security requirements, integration complexity, and long-term business goals.

Build an MVP

Before building a full-fledged financial app, it is wise to first develop an MVP (Minimum Viable Product). Why? Because no amount of internal planning fully replaces real user feedback.

An MVP focuses on the core function of the product and puts it in front of actual users. What they do with it, where they lose interest, what they ask for- that data is what drives the next phase of development.

Testing and QA

QA engineers thoroughly test the platform to deliver a secure online banking app. They look for bugs and glitches, and any issue found is fixed immediately.

Since FinTech applications handle sensitive financial data and real-money transactions, even minor issues can impact user trust significantly. In financial platforms, a single unresolved bug is not just a technical issue; it becomes a credibility and security concern.

Before deployment, FinTech applications typically go through multiple testing layers, including:

- Functional testing to validate core features and transaction flows.

- Security testing to identify vulnerabilities and data protection risks.

- Performance testing to evaluate system stability under high user load.

- Device and platform testing across iOS, Android and different screen environments

Deploy the application

In this stage, mobile app developers prepare the platform for deployment in the live production environment. Financial apps go through stricter review processes than standard applications on both the App Store and Google Play, so preparation matters more than most teams account for.

Getting this stage right means:

- Meeting App Store and Google Play financial app guidelines

- Setting up crash reporting and performance monitoring tools

- Configuring analytics before the first user signs up

- Having a feedback collection process ready from day one

Ongoing maintenance and performance optimization

Launching a FinTech application is only the beginning. Once the platform goes live, ongoing maintenance, monitoring, and optimization become critical to long-term product stability and user retention.

Compliance requirements shift, new security threats emerge, and real user behavior points to friction points that only become visible once actual people are using the product daily.

Maintenance in FinTech is an ongoing commitment that directly affects how long users stay and how much they trust the platform over time.

FinTech app security and compliance: Regional regulations to follow

A FinTech application cannot operate in any market without the right IT services for the finance industry backing its regulatory and security requirements in that region. This applies to startups, scaleups, and established financial enterprises.

Security and regulatory standards are not optional considerations in FinTech development. They are legal obligations that need to be addressed during the development process, not after the product is already live and serving users.

Security and regulatory standards are not optional considerations in FinTech development. They are legal obligations that need to be addressed during the development process, not after the product is already live and serving users.

Regulatory frameworks vary by geography, financial product category, and data handling practices, making early compliance planning a critical part of FinTech app development.

United States (USA)

PCI DSS (Payment Card Industry Data Security Standard)

When a user pays through a FinTech app, their sensitive card data passes through multiple layers of the system. PCI DSS defines how that data must be stored, processed, and transmitted securely at every stage. Meeting these standards is not optional for any platform processing card-based transactions in the US market.

GLBA (Gramm-Leach-Bliley Act)

GLBA applies to any FinTech business that collects personal financial information from consumers. It does not just require transparency about how the customer data is used, It also mandates that businesses put real security measures in place to protect it.

Companies that handle this data without meeting GLBA standards face regulatory action that is difficult and expensive to resolve.

BSA (Bank Secrecy Act)

The Bank Secrecy Act is one of the primary anti-money laundering (AML) regulations governing financial platforms in the United States. It requires FinTech companies to monitor transactions, maintain records, and file reports on suspicious activity.

EFTA (Electronic Fund Transfer Act)

The Electronic Fund Transfer Act establishes consumer protection rules for electronic financial transactions. It defines how FinTech platforms must handle issues such as failed transfers, unauthorized transactions, transaction disputes, and payment errors to ensure users are protected when digital transfers do not process correctly.

United Kingdom (UK)

FCA (Financial Conduct Authority) Regulations

The Financial Conduct Authority (FCA) regulates how financial services are offered and operated in the UK market. FinTech companies need authorization before they can legally operate. What that authorization covers depends on the product: payments, lending, or investment services each carry different requirements under FCA oversight.

PSD2 (Payment Services Directive 2)

PSD2 requires FinTech platforms handling payments to implement strong customer authentication on every electronic transaction. It also opens up banking data to authorized third-party providers through secure APIs. Any FinTech operating in the UK and European payments space has to meet these standards before going live.

AML (Anti-Money Laundering) Regulations

AML regulations help businesses in the FinTech sector stay on the right side of financial crime laws. User verification, transaction monitoring, and suspicious activity reporting are all mandatory obligations that begin the moment a user signs up.

Europe

GDPR (General Data Protection Regulation)

Any FinTech platform serving EU users falls under GDPR, regardless of where the business is based. Users have the right to access their data, correct it, or have it removed entirely. Penalties for non-compliance are among the highest of any regulatory framework globally.

EMD (Electronic Money Directive)

EMD helps non-bank institutions issue and manage electronic money legally. It creates a licensing framework specifically for Electronic Money Institutions, making it possible for FinTech platforms to offer digital payment products without holding a full banking license.

AMLD (Anti-Money Laundering Directive)

Financial crime does not announce itself. AMLD exists because FinTech platforms need a structured way to catch it early. Customer identity checks, ongoing transaction scrutiny, and timely reporting of anything suspicious are what this directive demands from every platform it covers.

Emerging technologies powering the next generation of FinTech apps

Modern FinTech apps like Cleo and Stripe are moving well beyond basic functionality. Advanced technologies like artificial intelligence and predictive analytics are actively raising the bar for what users expect from every financial app they use.

AI/ML

FinTech apps that integrate artificial intelligence and ML are more like intelligent financial assistants that users actually want. Spending patterns are analyzed, fraud is caught before it is completed, and credit decisions happen faster using data points that traditional scoring models never considered.

For businesses building a FinTech product today, integrating AI agents in finance is no longer a future roadmap item. It is a current competitive requirement.

Blockchain

By using blockchain technology in finance app development, developers can give users full transaction transparency with no central point of failure. Crypto wallets, decentralized finance features, and smart contracts are already part of leading FinTech products, reducing costs, removing intermediaries, and giving users direct control over how their money moves.

RPA

Manual processes in finance are expensive, slow, and prone to error. Robotic process automation solves that by automating the tasks that do not require human judgment, like transaction matching and data entry. FinTech businesses that have brought RPA services into their operations handle significantly higher transaction volumes without the operational overhead.

Predictive analytics

Predictive analytics engines process transaction history and behavioral data continuously. Credit risk becomes measurable before it materializes, spending patterns surface before they become problems, and investment signals appear early enough to act on. That is where predictive analytics services create real product differentiation.

How much does it cost to develop a FinTech app?

Understanding the FinTech app development process is only one part of the equation. For most founders and businesses, the next question is usually the most important: how much does it actually cost to build a FinTech app?

FinTech app development costs can start from around $25,000 for a basic MVP and exceed $250,000 for enterprise-grade platforms with advanced integrations, compliance requirements, and complex financial workflows. The final cost depends on multiple technical, operational, and business factors that need to be evaluated before providing an accurate estimate.

To give you a clearer picture, the table below breaks down the mobile application development cost for FinTech across different complexity levels.

| Complexity Level | Estimated Cost Range |

| Simple App | $25,000- $60,000 |

| Mid-Level App | $60,000- $150,000 |

| Advanced App | $150,000- $300,000 or more |

To get a personalized quote, feel free to connect with our team, or you can also use our free cost calculator .

How to choose the best FinTech app development partner?

Choosing the right FinTech app development partner directly impacts how successfully your product is built, launched, and scaled. Since FinTech involves payment infrastructure, compliance, and security requirements that most general app builds don’t, evaluate partners on more than portfolio size alone.

When assessing a potential partner, look for:

- Real FinTech domain experience — payment flows, banking APIs, and compliance-heavy builds, not just general UI/UX work

- A portfolio with actual financial products — not just mockups or demo apps

- Clear, specific answers on compliance and security — vague responses usually signal limited hands-on experience

- Transparent, responsive communication from the first conversation, not just after signing

- Verified client reviews on platforms like Clutch or Google, focused on delivery quality and post-launch support rather than star ratings alone

Getting this evaluation right early saves significant time, budget, and rework later in the project.

Conclusion

The financial industry has moved to mobile, and that shift is not reversing. A well-built FinTech app is no longer a competitive advantage. It is a baseline expectation from users who manage everything digitally.

Building a successful FinTech app requires more than good features. It involves making the right technology decisions, addressing compliance and security requirements early, and working with a fintech software development partner that understands the operational and technical complexities of financial software.

We hope this guide has provided clarity around the FinTech app development process and helped you better understand the strategic, technical, and regulatory considerations involved in bringing a FinTech product to market.

Frequently Asked Questions

The cost to develop a simple FinTech app typically ranges from $25,000 to $60,000, while an advanced FinTech app can cost anywhere between $150,000 and $300,000 or more. The exact figure is difficult to determine because it depends on a wide range of factors.

It includes app complexity, type, target platform, number of features, UI/UX design requirements, regulatory compliance, licensing fees, and the location of the development team.

Building an MVP typically takes around 3 to 6 months, while complex financial app development can take 7 to 12 months or more. Several factors impact the timeline, such as project scope, customization level, complexity, app design, third-party integrations, and the tech stack selected.

It is best to consult with a FinTech application development service provider to get a more accurate estimate based on your specific requirements.

A traditional banking app is a digital extension of an existing bank, built on legacy systems with slower update cycles and rigid processes. FinTech apps, on the other hand, are built around a specific user problem on modern cloud-based infrastructure, which allows for faster onboarding, better personalisation, and quicker feature releases.