Key takeaways:

- Fintech app development cost typically ranges from $25,000 for a simple build to $250,000 or more for a fully AI-powered platform, depending on scope.

- SME adoption of FinTech solutions has crossed 62% globally, a clear sign this market isn’t slowing down anytime soon.

- Platform choice affects cost significantly; native development for iOS and Android nearly doubles frontend work compared to cross-platform frameworks.

- KYC and AML compliance isn’t something you can skip, and building it in properly can add $10,000 to $40,000 depending on scope.

- Launching with an MVP first, rather than a fully-loaded app, keeps early spending in check while you validate the idea with real users.

Most sources that quote FinTech app development costs give a number without explaining what drives it. That’s what makes budgeting genuinely difficult.

The cost to build a FinTech app typically runs from $25,000 for a basic MVP to $250,000 or more for a full-featured platform, shaped by app type, compliance requirements, feature complexity, and team location.

FinTech costs more to build right, since the app is handling real money and real regulatory exposure, not something most other app categories deal with.

A wrong cost estimate doesn’t just delay a launch. It can mean rebuilding core features mid-development or running out of runway before the app reaches its first users.

Business Research Insights found that 62% of SMEs worldwide already use FinTech solutions for payments and banking, and that kind of adoption doesn’t happen without serious infrastructure behind it.

That growth is exactly why so many businesses are now looking to build their own FinTech product.

This blog focuses specifically on the cost of developing a FinTech application. If you’re evaluating the broader build process, our guide to FinTech mobile app development covers that in full.

What is the cost to build a FinTech app?

No two FinTech apps cost the same to build; a simple app can start around $25,000, while an advanced, AI-powered platform can climb past $250,000.

The gap between those numbers comes down to feature complexity, compliance requirements, integration depth, and where your development team is based.

Here’s a breakdown of custom FinTech application development cost by complexity level, so you can see roughly where your project fits.

| Complexity Level | Estimated Cost Range | Timeline | Features Included |

| Simple App | $25,000 – $60,000 | 2 to 4 months | Basic user onboarding, payment gateway integration, and transaction history |

| Mid-Level App | $60,000 – $150,000 | 4 to 8 months | Multi-currency support, biometric authentication and budgeting/analytics tools |

| Complex App

( AI-powered) |

$150,000 – $250,000 | 8 to 12+ months | Personalized financial insights, KYC/AML automation and AI-driven fraud detection. |

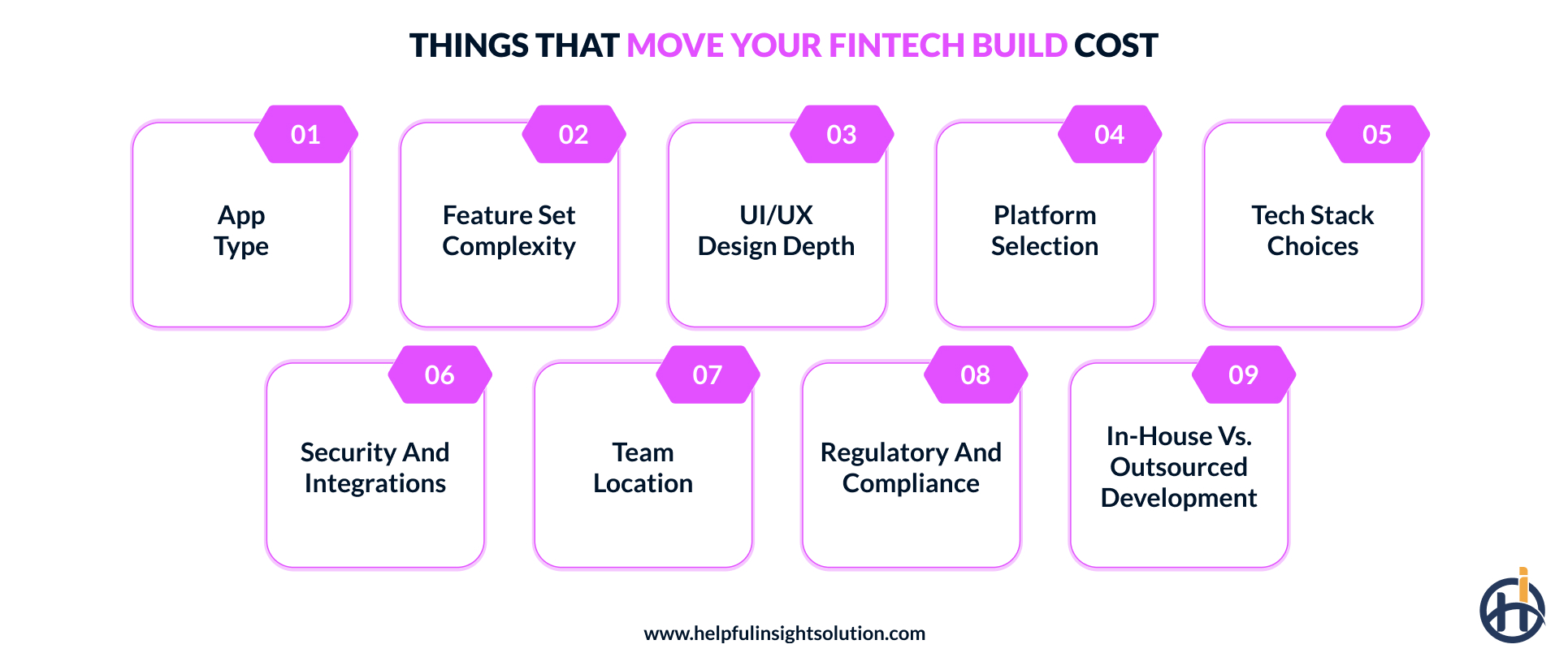

Key factors that influence FinTech app development cost

Estimating the FinTech application development cost takes more than counting features. No single factor decides the final number; it’s a combination of several variables, from feature complexity and data architecture to team structure.

Here’s what actually drives the cost up or down:

App type

The type of FinTech app you’re building changes the cost picture entirely. A peer-to-peer payment app and a full digital banking platform aren’t in the same category at all; the infrastructure, backend architecture, and security needs differ long before you even start adding features.

App type also determines compliance scope. A crypto wallet and a personal finance tracker are governed by very different regulations like KYC and AML obligations, PCI DSS, SEC requirements, and those differences reflect directly in the development budget.

Feature set complexity

The number of features matters, but what actually drives up the cost to develop a FinTech app is how complex each one is to build correctly.

A basic login screen takes days, while something like real-time fraud detection or AI-driven credit scoring can take weeks of specialized engineering from developers with financial domain knowledge.

If you are planning a lending or investment app, expect feature complexity to be the single biggest cost variable both categories rely heavily on exactly these kinds of high-effort, data-intensive features.

UI/UX design depth

The more a screen asks a user to understand or decide, the more it costs to design well. Simple login or profile screens are straightforward to build, but dashboards involving investment tracking or credit scores require custom data visualizations and multiple design revisions before they are clear enough for everyday users.

UI/UX design timelines in FinTech consistently run longer than standard apps for this reason; one confusing financial screen can permanently damage user trust.

On cost, a simple design covering login, onboarding, and a standard account dashboard usually falls between $5,000 and $15,000.

Go custom instead: interactive charts, personalized dashboards, multiple rounds of usability testing, and that range moves up to $20,000 to $40,000 or more.

Platform selection

Whether you build for iOS, Android, or both, this decision alone can shift your budget significantly. Native development means two separate codebases: Swift for iOS, Kotlin for Android, and that alone nearly doubles the frontend work on most mobile app development projects.

Many businesses start with one platform to keep the MVP lean and expand later. In FinTech, though, cost savings from cross-platform frameworks like React Native or Flutter tend to shrink fast.

Add biometric authentication, NFC payments, or real-time trading charts into the scope, and native code becomes necessary again, no matter what framework handles the rest of the app.

FinTech application development cost by platform comparison

| Platform | Cost Range | Best Suited For |

| iOS | $30,000 to $90,000 | Apps targeting higher security standards |

| Android | $20,000 to $60,000 | Broader global reach |

| Cross-Platform (React Native/Flutter) | $35,000 to $100,000 | Startups needing both platforms fast, on a tighter budget |

| Native + Cross Platform | $50,000 to $120,000 or more | Apps with heavy security and biometric needs alongside general features |

Tech stack choices

The technology stack you choose is one of the biggest drivers of financial app development costs, affecting both what you pay to build the app and what you keep paying to run it afterward.

Some frameworks cost less to host and scale, and that difference compounds as transaction volume grows over time.

In FinTech specifically, certain stacks handle encryption, audit logging, and compliance requirements more efficiently than others, which cuts down the engineering work needed later to meet regulatory standards.

A stack that’s harder to secure doesn’t just cost more upfront; it costs more every year after that too.

Security and third-party integrations

Payment gateways, identity verification services, and banking data providers all carry their own licensing fees on top of the actual integration work your development team has to do.

These are not one-time costs; most are billed per user, per transaction, or monthly, and they grow as the app scales.

Security work itself adds a separate layer of cost. Encryption, multi-factor authentication, biometric login, penetration testing- all of it needs dedicated engineering time before launch, not after. And in 2026, deepfake-resistant liveness detection has quietly become close to mandatory for KYC.

It costs more to build in, but it also shuts down a vulnerability that regulators and banking partners are watching closely right now.

Here’s a rough breakdown of what these integrations cost:

| Integration Type | Estimated Cost |

| Identity Verification (KYC/AML) | $7,000- $18,000 |

| Open Banking APIs | $12,000- $25,000 |

| Fraud Detection and Risk Scoring | $10,000- $30,000 |

| Payment Gateways | $5,000- $12,000 |

Development team location and hourly rates

Team location plays a major role in the total FinTech app development cost.

Hourly rates vary sharply by region, and the same build can cost two to three times more with a US-based team than with an equally experienced team in Eastern Europe or India.

The difference is significant enough that many funded startups choose offshore or nearshore teams for the build phase and keep a smaller senior team in-house for product decisions.

Our guide on how to hire software developers for a startup covers how to structure that decision.

Here are the 2026 developer hourly rates by region:

| Location | Hourly Rates |

| North America | $80 to $150 |

| Western Europe | $50 to $120 |

| Eastern Europe | $35 to $80 |

| Asia | $20 to $60 |

Regulatory and compliance requirements

Compliance is mandatory in FinTech; the depth of your implementation is where the decision lies.

KYC and AML requirements apply to nearly every FinTech app by default, but the extent of verification, transaction monitoring, audit logging, and regulatory reporting you build in depends on your app type and the markets you operate in.

This can add $10,000 to $40,000 or more to development costs, depending on how many regulatory frameworks apply.

If your app operates across multiple markets, say India (RBI), the US (FinCEN), and the UAE (Central Bank), compliance costs don’t just add up, but they stack. Each jurisdiction brings its own separate requirements to meet, often meaning separate KYC workflows for each region.

In-house vs. outsourced development

The staffing model you choose affects your budget nearly as much as location, sometimes more. In-house hiring means covering salaries, benefits, and a recruitment process that typically takes two to three months, particularly for developers with financial compliance experience.

Outsourcing removes that hiring delay entirely and generally costs less overall, though the exact savings depend on the partner’s rates and region.

For FinTech startup founders specifically, that speed advantage often matters as much as the cost difference.

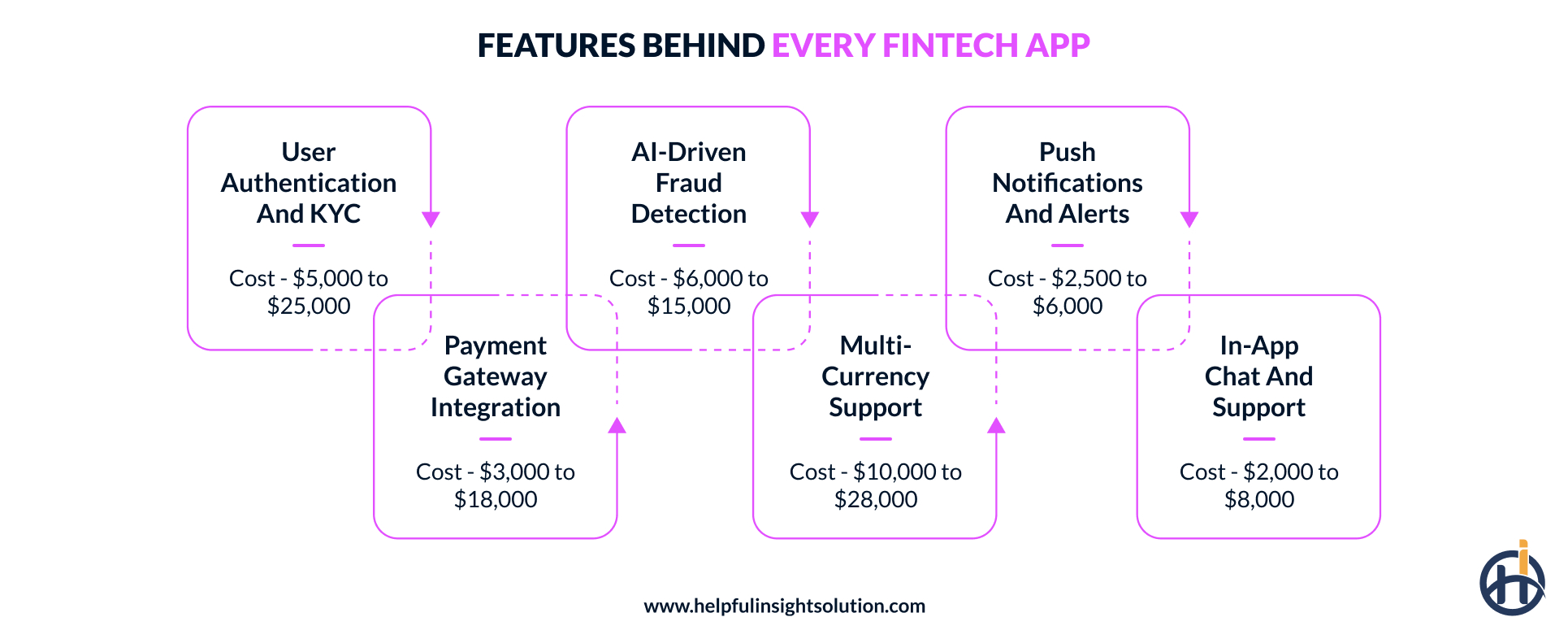

How much do key fintech app features cost to build?

Feature selection plays a major role in determining the cost to develop a FinTech app, since each one adds a different level of engineering effort, integration complexity, and ongoing maintenance.

Below are the most essential features and what each typically costs to build.

User authentication and KYC

Basic authentication alone is simple, but FinTech apps require KYC verification, which means connecting to identity verification providers like Sumsub, Onfido, and Persona, handling document uploads, and running AML background checks automatically.

What often gets missed in cost estimates is that KYC isn’t a one-time build cost; ongoing verification API fees continue per user even after launch.

Estimated Cost Range: $5,000- $25,000

Payment gateway integration

Payment integration is not optional for a FinTech app, since moving money securely is often the core function of the product itself.

This usually means connecting to processors like Stripe, Razorpay, or Square for standard builds, and connecting to local payment rails such as UPI in India, ACH in the US, depending on where the app needs to operate.

What often gets overlooked is that custom-built payment infrastructure doesn’t just cost more upfront; it also shifts PCI DSS liability for security compliance onto your team instead of the payment processor, a significant compliance burden that most early-stage teams are not equipped to manage.

Estimated Cost Range: $3,000- $18,000

AI-driven fraud detection

Manual fraud review can’t keep up with transaction volume anymore; that’s the real reason this feature has become standard in FinTech apps.

Many businesses work with an AI development company specifically for this functionality, since building accurate risk-scoring models requires specialised expertise in machine learning and financial transaction data that most in-house teams do not have,

Note that the cost range below covers the initial build. Fraud models require ongoing retraining as attack patterns evolve, which adds to the annual maintenance budget.

Estimated Cost Range: $6,000- $15,000

Multi-currency support

Multi-currency support is expected in any FinTech app dealing with remittances, cross-border payments, or international users.

Getting it right requires real-time exchange rate feeds, wallet-level currency handling, and transaction logic that remains accurate under constant rate changes. Apps operating in multiple markets also need to account for currency-specific compliance requirements.

Estimated Cost Range: $10,000- $28,000

Push notifications and alerts

Push notifications feel like a minor feature, but in finance, timing and reliability are non-negotiable. A delayed fraud alert or a duplicate transaction notification causes real harm; it is not just a UX issue.

Backend systems built to handle sudden spikes in alert volume without lagging or failing.

Few cost estimates account for the additional testing required to prevent duplicate alerts, a small bug that can seriously damage user trust in a financial app.

Estimated Cost Range: $2,500- $6,000

In-app chat/support

Users want answers fast when money is involved, not a generic ticketing system. Basic chat integrations are easy to build, but adding AI-driven responses, encrypted messaging, or voice support raises complexity significantly.

What most estimates skip is that FinTech support conversations often need to be logged and retained for compliance reasons, and the same audit trail rules that apply to transactions can extend to customer communications, depending on the regulatory framework involved.

Estimated Cost Range: $2,000- $8,000

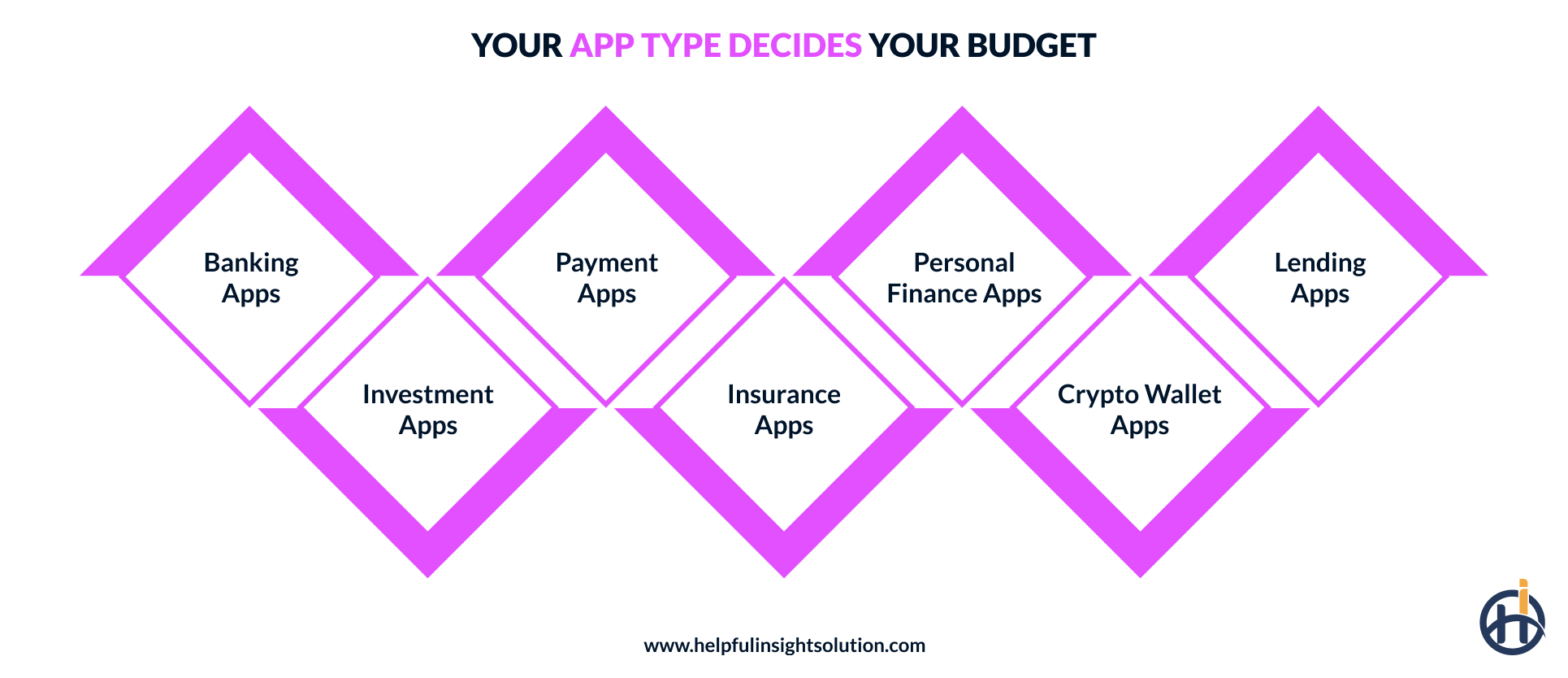

FinTech app development cost by app type

The type of FinTech app you’re building largely decides the final number, since a lending app and an investment app development demand entirely different backend logic, compliance requirements, and integration depth.

Knowing which category your idea falls into before you start budgeting helps you avoid basing your estimate on the wrong comparison entirely

In this section, let’s explore the different types of FinTech apps and what each one typically costs to build.

Banking apps

Banking apps carry more complexity than most other apps in the FinTech category because they manage a business’s core financial operations end to end, not just a single function like payments or budgeting.

Banking app development cost typically runs between $25,000 and $200,000 or more, driven primarily by core banking system integration and real-time transaction processing.

Fraud monitoring and compliance auditing are not one-time build costs.

They require ongoing investment well after launch and can collectively approach the original build cost within two to three years of operation.

Payment apps

Where banking apps handle the full account relationship, payment apps move money fast, sending, receiving, and storing funds securely between users.

Development for something similar to payment apps like PayZapp usually costs around $30,000 to $150,000 or more, driven mainly by fraud detection depth and third-party bank integrations (UPI, ACH, SEPA) and the backend reliability required for real-time settlement.

Instant transfer features cost more to build than standard payment flows.

Real-time settlement needs low-latency backend systems, redundant failover setups, and reconciliation logic to confirm every payment actually went through correctly.

Personal finance apps

Personal finance apps help users track spending, set budgets, and understand their financial habits without moving money between accounts.

It may fall between the range of $40,000 and $250,000 or more, shaped mainly by how many banks and data providers the app connects to and the depth of the analytics features.

Bank APIs change often, so automatic transaction syncing needs regular maintenance, which should also be considered in the final budget.

Lending apps

Lending apps like Dave manage the full loan lifecycle, including credit assessment, KYC verification, automated underwriting, EMI calculations, and repayment tracking.

Custom FinTech application development cost for this category runs around $25,000 to $120,000 or more, with automated underwriting being one of the bigger factors that pushes the number toward the higher end.

Adding AI-driven credit scoring raises the cost further and extends it well past initial launch. Credit scoring models require continuous retraining as repayment data builds up, a model trained on 10,000 loans behaves differently from one trained on 100,000, and keeping it accurate is an ongoing engineering cost that most initial estimates do not include.

Investment apps

72% of FinTech investors prefer mobile apps for trading. Investment apps cover stocks, mutual funds, crypto, and often a combination of all three, pairing real-time market data with portfolio tracking, trade execution, and personalised recommendations.

Investment app development costs run from $50,000 to $180,000 or more, and two cost drivers specific to this category often get left out of that number entirely.

Real-time market data providers like Bloomberg charge ongoing licensing fees that start at launch and grow as usage increases.

On top of that, most markets require regulatory approval for investment apps, which adds legal costs and timeline that the development budget alone won’t cover.

Insurance apps

Insurance apps let customers browse policies, file claims, and check status updates, all from their phone, without waiting on hold or dealing with paperwork.

For insurers, the benefit is operational: claims move faster, manual processing decreases, and quicker resolutions improve customer retention.

Planning to invest in an insurance mobile app development? Cost typically starts around $20,000 and can climb to $300,000 or more, depending on how many policy types the app supports, how many insurer or reinsurer integrations are needed, and whether features like AI-driven claims assessment or underwriting automation are included.

The integration complexity with legacy insurance systems is where most budget surprises in this category come from.

Crypto wallet apps

Crypto wallet apps rank among the costlier FinTech app categories to build, since these apps need blockchain integration, secure private key management, multi-signature wallet architecture, and real-time price tracking to work together without failure.

One security gap in a crypto wallet can mean permanent loss of funds, not just an inconvenience.

Crypto wallet app development cost typically falls between $60,000 and $230,000 or more. Multi-chain support plays a big role in that range. So does the number of jurisdictions the app needs to comply with, and each one comes with its own security audit requirements on top.

In 2026, crypto apps operating in the US, EU, and UAE all face increasingly specific licensing requirements, adding legal and compliance costs that sit outside the development budget itself.

Cost by development stage: MVP vs. full-scale vs. enterprise

Cost isn’t fixed once; it shifts significantly depending on which stage you’re building for. A FinTech MVP cost covers just the essentials needed to validate the idea with real users.

Full-scale and enterprise builds bring added infrastructure, compliance, and scale requirements. Understanding this early helps you budget realistically at each stage.

Here’s the breakdown in the table below:

| Development Stage | Estimated Cost Range | Timeline | Key Focus | Best Suited For |

| Minimum Viable Product (MVP) | $25,000- $70,000 | 1 to 3 months | Validating core functionality with essential features and basic security | Pre-funding founders testing product-market fit |

| Full-Scale Product | $100,000- $250,000 | 5 to 9 months | Adding advanced features, integrations, and stronger compliance infrastructure | Funded startups ready to scale operations |

| Enterprise-Level System | $400,000 to $900,000+ | 12 to 20+ months | Building for high transaction volume and scalability | Established businesses or regulated financial institutions |

FinTech app monetization strategies: How to generate revenue

Understanding what a FinTech app costs to build is one side of the equation. The other is how it generates revenue once it is live.

Several monetization models exist for FinTech apps, including subscription plans, transaction fees, and interest margins. Most apps don’t rely on just one; they blend two or three depending on the user base.

Transaction fees

Revenue here comes directly from user activity, a cut taken from every transfer, payment, or trade processed through the app.

It works particularly well for apps with frequent, high-volume usage. Pricing this correctly matters; set the fee too high and users switch to a cheaper competitor fast.

Subscription model

Charge users regularly, monthly or yearly, for access to premium tools or deeper financial insights they can’t get for free. Income becomes steady and forecastable instead of fluctuating with daily transaction activity.

The free version needs real value on its own; otherwise, nobody sticks around long enough to consider paying.

Interest margins

This model works by charging interest on loans or BNPL balances at a rate higher than the cost of funding them, the gap between the two is where the profit comes from.

It’s one of the most lucrative models in fintech, though it only works well with strong credit scoring and risk management in place.

Interchange fees

Every time a user swipes a card linked to your app, a small cut of the merchant’s transaction fee flows back to you, no charge to the user at all.

This model works well for card-based fintech products, though earnings depend heavily on how often users actually spend using the card.

Hidden and ongoing FinTech app costs to budget for

Most FinTech app development cost breakdown estimates stop at launch, when in reality, that’s where a second set of expenses begins.

API renewals, compliance audits, cloud infrastructure, and security testing all continue well after the app goes live, and together commonly adding 15% to 25% of the original build cost annually.

Here are the additional costs worth planning for before finalizing your budget.

Third-party API and licensing fees

Most of what powers a fintech app is not a one-time cost. Payment gateways, KYC verification providers, banking APIs, and certain compliance tools all come with ongoing fees, some charge a flat monthly rate, others charge based on how many users or transactions you have.

As your app grows, these costs grow with it. This is the expense that most early-stage budgets underestimate and most mid-stage companies find hardest to absorb.

Cloud hosting and server costs

Cloud hosting costs scale directly with transaction volume and data storage needs, and financial mobile apps typically run higher than standard apps due to encryption overhead and compliance-grade storage for audit trails, which costs meaningfully more than standard storage tiers.

A simple app might cost $100 to $500 monthly on standard cloud infrastructure.

Add compliance-grade storage, multi-region redundancy and peak transaction capacity planning, and that figure rises significantly for any app operating at production volume.

App maintenance and bug fixes

Maintenance in fintech goes beyond fixing bugs and keeping up with iOS or Android updates; it also means staying ahead of new compliance requirements as regulations shift. Plan for 15% to 20% of your mobile app development cost annually here, and don’t let it slide.

Delayed maintenance doesn’t just risk crashes; it can trigger compliance violations that end up costing far more to fix down the line.

App store and platform fees

Another hidden cost businesses generally don’t account for is app store commissions. Apple and Google usually take 15% to 30% on in-app purchases and subscriptions, though most fintech transactions happen outside this system, so it doesn’t apply the same way it would for a typical app.

Subscription features and premium add-ons, though, still fall under these fees.

Compliance audits and renewals

Getting certified for PCI DSS or SOC 2 once isn’t enough; these need renewal on a regular cycle, and each renewal comes with its own audit and documentation costs.

Miss a renewal window, and you could lose the ability to legally process transactions until it’s sorted out.

Most businesses don’t plan for this as something recurring; they treat it like a one-time cost, then get caught off guard when it comes up again a year later.

How to reduce FinTech app development cost without cutting corners

Knowing what a FinTech app costs matters, but keeping that number under control comes down to the choices made during planning and development.

The approaches below aren’t shortcuts; they’re about spending in the right places so quality never takes the hit.

Here’s where the savings actually come from:

Start with an MVP

Launching with a full feature set before validating demand is one of the most expensive mistakes, since features built without real user feedback often get rebuilt anyway.

Starting with just the core function, a single payment flow or budgeting tool, keeps initial spend focused. It also puts you in a stronger spot when raising funds; investors want to see something working, not a list of planned features.

Use BaaS providers

Building core banking infrastructure from scratch takes months and requires banking licenses that most startups don’t have.

BaaS providers like Stripe Treasury, Unit, or Synapse let you connect to existing banking infrastructure through APIs, cutting both development time and legal overhead significantly.

This shifts your team’s focus to the actual product instead of banking plumbing, though it does mean depending on your provider’s uptime and compliance standing.

Choose cross-platform where possible

Building separate native apps for iOS and Android doubles the frontend work. A shared codebase through React Native or Flutter usually brings costs down by 30-40%.

It has limits though; security-heavy features like biometric login tend to need native components no matter which framework you’re using elsewhere.

Outsource development

This is one of the best ways to lower cost without giving up quality. Teams based in Eastern Europe or Asia often bring the same level of expertise as US-based hires, just at a fraction of the rate, and without the overhead of full-time salaries and benefits.

If your scope extends into broader financial software development beyond a single app, an experienced outsourced team can usually advise on that path too.

How Helpful Insight can help you develop a FinTech app within budget

Getting a realistic cost estimate matters; sticking to it matters more. That’s exactly where the right development partner makes the difference.

As an experienced FinTech app development company, we bring hands-on experience building secure, compliant, scalable apps for startups, banks, and financial institutions.

Our team understands the financial ecosystem deeply, with a strong grasp of regulatory compliance that shapes every decision from day one. That’s how we help clients avoid the budget surprises so many teams run into midway through development.

Our services

- Strategic consulting services

- Custom app development

- UI/UX design

- MVP development

- Third-party integrations

- FinTech app testing

- Support and maintenance

A FinTech app we built: Case study

Here is an example of a FinTech app Helpful Insight built: a peer-to-peer payment platform where budget management, security, and compliance all had to work together from day one.

Project: Peer-to-Peer payment app

Our client wanted to build a P2P payment app that let users send and receive money instantly, but their existing plan lacked the security infrastructure needed to handle real-time transfers safely.

Challenge

- Processing transfers instantly without delays

- Keeping user data secure

- Preventing duplicate or failed transactions

- Building a simple, fast user experience

- Integrating with multiple banks reliably

The solution we delivered

- Built a real-time fraud detection engine using pre-trained models to control cost

- Used a BaaS provider instead of building settlement infrastructure from scratch

- Set up automated duplicate transaction checks at the database level

- Built scalable cloud infrastructure to handle peak transaction volumes

- Kept the initial UI simple, prioritizing speed over unnecessary features

- Choose a cross-platform framework to launch on time and on budget

The impact

- Onboarding time cut by half

- Zero security breaches post-launch

- 30% increase in user retention

- Fraud incidents reduced by 40%

Building a FinTech app involves more cost variables than most initial estimates capture: feature complexity, compliance depth, integration overhead, and the ongoing costs that begin at launch.

This guide covers each one so the number you take into planning reflects the full picture, not just the development quote.

If you’re ready to build your own fintech app and want a team that can deliver exactly what you need, within budget, share your project requirements and we will talk through the scope.

FAQs

The cost to develop a simple FinTech app can start from $25,000, and it can reach up to $250,000 or more for an advanced app. It’s shaped by a range of factors, including feature complexity, app type, number of features, UI/UX design, third-party integrations, and where your development team is based, among others. A combination of these factors determines the final number.

Expect $25,000 to $70,000 for a FinTech MVP. It costs more than a standard MVP for one reason mainly, financial apps handle real money, which means security and compliance can’t be an afterthought, even in the earliest version.

A personal finance app typically costs between $30,000 and $200,000 or more. The actual figure comes down to feature complexity, how many banking or data integrations you need, your security setup, and the location of developers.

Most FinTech apps take somewhere between 3 and 12 months to build. A basic MVP can be ready in 1 to 3 months. Add heavy compliance work and multiple integrations, and that timeline stretches closer to 9 months or more.