Key Takeaways:

- Not all insurance portals serve the same purpose, picking the wrong type costs more to fix later.

- Insurance portal development works best in clear phases with structured execution planning.

- With a custom portal, you own everything but if you’re just starting out, a platform-based solution is usually the more practical first step.

- A basic portal can start around $25,000. Once you get into advanced builds with complex integrations and custom workflows, that number can cross $400,000.

- The vendor you pick, how seriously compliance is taken, and how security is handled quietly determine project success.

Insurance businesses are built on the promise of being there when things go wrong. The gap between that promise and the experience is where most insurers lose customers.

So where does the problem start? In most cases, it comes down to one thing: CRM, billing, and claims platforms that should stay in sync often don’t, leaving insurers to manually connect the dots that the system should connect automatically. Insurance web portals address this directly: when a claim is submitted, billing updates automatically, and a policy change reflects across every system that depends on it. That kind of synchronisation sits within the broader discipline of insurance software development, where the portal is one component of a larger ecosystem that includes policy administration, claims platforms, and payment infrastructure.

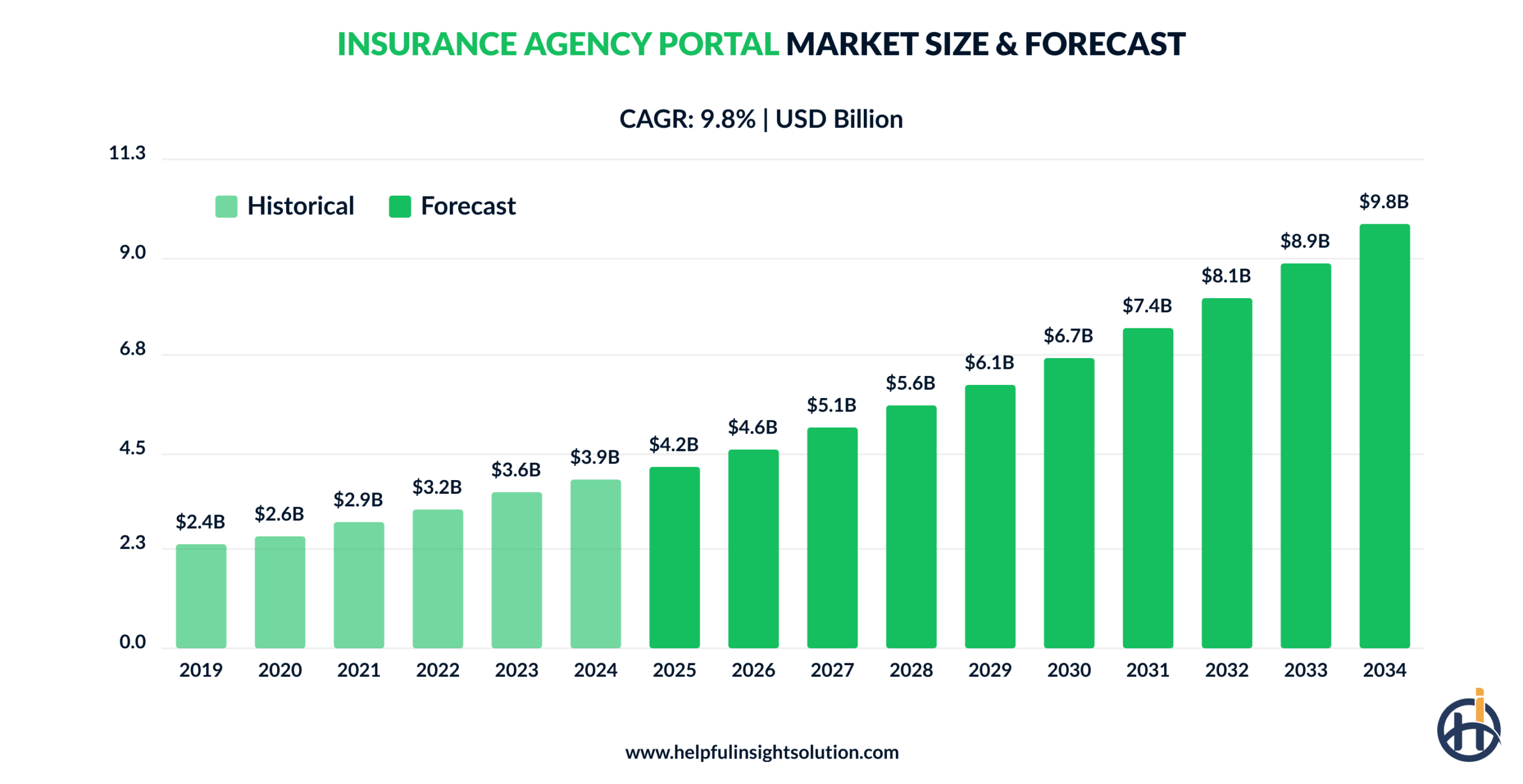

The global insurance agency portal market is expected to reach $9.8 billion by 2034, up from $4.6 billion in 2026. That kind of growth doesn’t happen unless the platform is solving something real.

If you’re running an insurance business, a well-developed portal isn’t an upgrade, it’s operational infrastructure. It reduces processing time, improves data accuracy, and gives clients the kind of self-service access they already expect from every other industry.

In this blog, we’ll walk you through everything you need to know about insurance portal development.

What is an Insurance Portal?

Ever logged into a banking app to check your balance or transfer money without calling the bank? An insurance web portal works the same way. It’s a secure digital platform where insurers, agents, and policyholders handle day-to-day insurance activities in one place.

Policyholders can log in to review their coverage details, submit and track claims, get quotes, and make payments without needing to go through multiple channels. Agents, in turn, get consolidated visibility into client data, policy status, and pending actions.

Building this kind of platform is what insurance portal development is about — designing and architecting a system around the specific operational demands of the insurance industry. If you’re evaluating your options, our insurance software development services cover the full build lifecycle from architecture to deployment.

Unlike off-the-shelf solutions, a purpose-built portal is structured to support agents, policyholders, and brokers through clearly defined workflows and role-based access.

What separates a modern portal from basic online tools is its ability to integrate with core insurance systems such as claims management and policy administration, giving insurers a single, cohesive platform to run their operations efficiently.

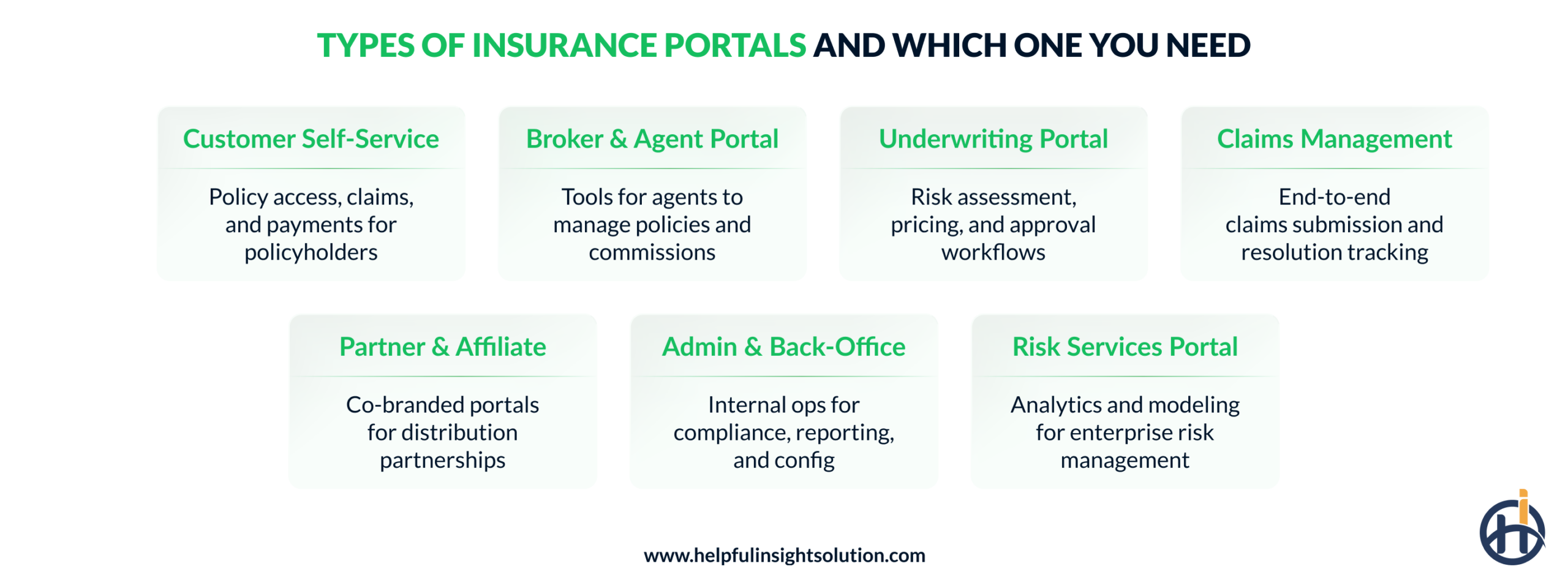

Types of Insurance Portals and Which One You Need

Not all insurance portals serve the same function. Some handle policyholder self-service, others are built around agent workflows or broker management. Before anything else is decided, you need to know which type you’re building.

In this section, we will explore the different types of insurance portal development you can consider.

Customer Self-Service Portal

A self-service portal lets policyholders log in anytime, check their coverage, pay premiums, download documents, and file claims. For insurance companies, it cuts down the routine support load. In fact, insurers using self-service portals have seen increased customer engagement.

Broker and Agent Portal

Agents spend hours searching for information like policy status, client history, and pending applications. The insurance agent portal puts all of that in one place. As a result, agents and brokers can get what they need and spend more time selling policies instead of searching. If you run an agency or work with a large agent network, this portal is all you need.

Underwriting Portal

Underwriting slows down broker communication, and applications are scattered across spreadsheets. This portal brings everything together so brokers submit, underwriters assess, and decisions move faster. If your team is losing days to manual follow-ups, an underwriting software solution can cut that time down.

Insurance Claims Management Portal

If slow claim cycles are costing you customers, then you definitely need to develop insurance claim management software. It allows policyholders to submit, upload documents, and track progress on their own. Adjusters receive complete information right from the FNOL, claim cycles shorten, and customers stay informed without anyone having to chase anything.

Partner and Affiliate Portal

External partners, affiliates, and co-sellers can only sell what they know. If they’re working off outdated product information, that’s a problem your internal team ends up fixing manually every time something changes. A partner portal sorts this out, everyone gets access to current resources, and your team isn’t stuck sending updates.

Admin and Back-Office Portal

The admin team needs a clear view of what’s running, what’s delayed, and where things are breaking down. Instead of jumping between multiple systems, an admin portal provides them with all the resources to manage the same, from compliance tracking and reporting to workflow management.

Risk Services Portal

Managing large policy volumes is one thing, but when risk evaluation starts slowing down decisions, that’s where things get costly. A risk services portal gives underwriters the tools to analyze, monitor, and report risk faster and with more accuracy than manual processes allow.

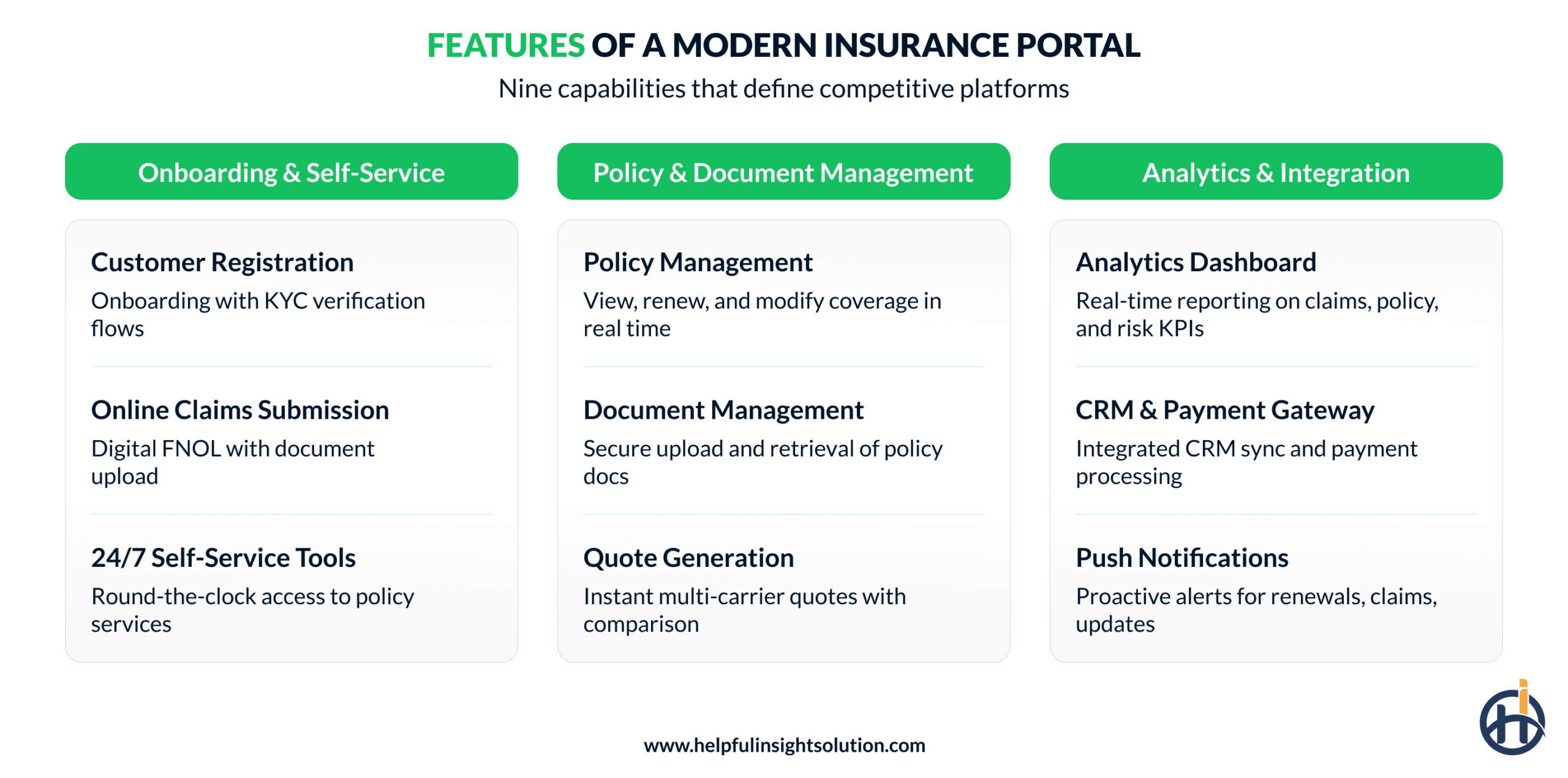

Core Features of a Modern Insurance Portal

Building a digital product for insurance is one thing, but building it with the right features is what makes it worth the investment. Here are the key features a software portal should have to function the way it’s supposed to.

makes it worth the investment. Here are the key features a software portal should have to function the way it’s supposed to.

| Feature | Description |

| Customer Registration | Allows new users to register through simple forms with identity checks, e-signature capture, and KYC verification built into the process. |

| Online Claims Submission | It enables policyholders to file claims, attach relevant documents, and monitor claim progress in real time. |

| Policy Management | Helps insurers handle everything from underwriting to renewals, so agents and customers always have the latest policy details. |

| Document Upload and Management | Let agents store and find insurance documents quickly without digging through folders or worrying about missing files. |

| Quote Generation and Comparison | With this feature, agents and policyholders get instant quotes and compare coverage options before making a decision. |

| 24/7 Self-Service Tools | Customers on their own can update information, pay premiums, and access policy documents without depending on agent availability. |

| Analytics and Reporting Dashboard | It gives insurers a clear view of claims, customer activity, and overall performance without fetching data from multiple places |

| CRM & Payment Gateway Integration | This feature connects data across systems like CRM and allows policyholders to make premium payments securely right through the portal. |

| Push Notifications and Alerts | Sends automated reminders for renewals, claim updates, and payment deadlines so nothing gets overlooked. |

Custom vs Platform-Based Insurance Portal Solution: What’s Right for You?

Well, there are two methodologies insurance businesses can choose for enterprise insurance portal development. Each comes with its own advantages and disadvantages. If you are also confused about which one to go with, this section will clear all your doubts.

Custom Insurance Portal

A custom portal is built from scratch around your specific workflows, needs, and customer base. This means every module from policy administration to claims workflow is engineered around your processes and regulatory obligations. There are no workarounds or feature compromises as the platform is built to fit your operations precisely.

Pros

- Built around your specific requirements

- Full control over features

- High scalability

Cons

- Higher upfront development cost

- Takes longer to build and deploy

- Requires ongoing support and maintenance

When to Choose

- You’re a mid to large-sized insurer handling high policy volumes.

- Full ownership of the product is a priority.

- Business is scaling and needs room to grow.

- Deep integration with existing systems is needed.

Platform-Based Insurance Portal

It is basically a ready-made portal you license from a vendor. You configure it, set it up, and start using it relatively quickly. Most platform-based solutions offer standard modules covering policies and claims. However, customization is typically constrained by the vendor’s architecture, which can limit how closely the platform aligns with your specific workflows or branding standards.

Pros

- Faster to deploy

- Lower upfront cost

- Works for standard insurance workflows

Cons

- Limited customization options

- Licensing costs add up eventually

- Complex legacy integrations

When to Choose

- You’re an early-stage insurtech or small agency testing the market.

- Don’t need heavy customization.

- Have a limited budget.

- Quick deployment is the immediate priority.

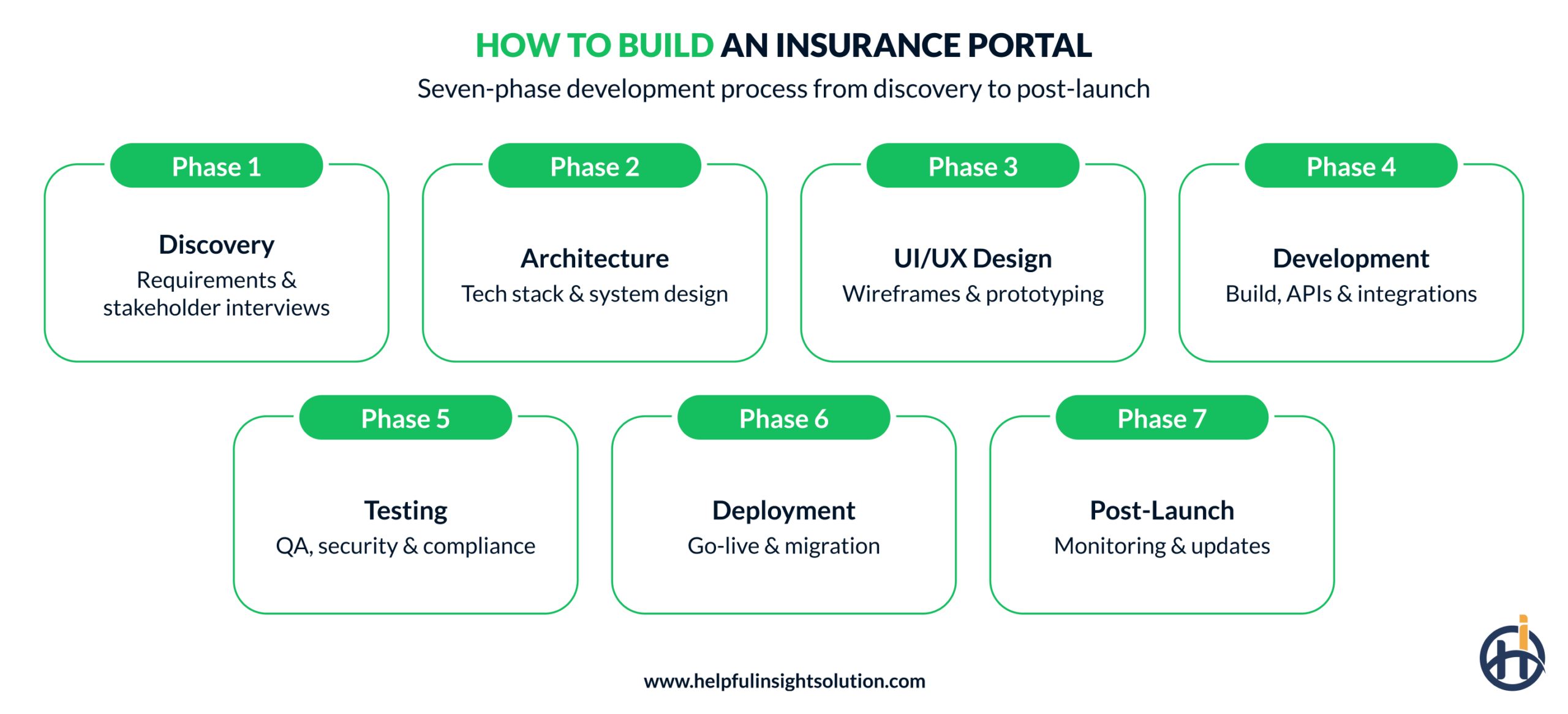

How to Build an Insurance Portal: 7 Phase Development Process

Each phase of the process is designed to build on the one before it, moving from discovery and architecture through development, integration, testing, and final deployment. For insurance portals specifically, this includes aligning workflows for policy management, claims processing, and regulatory compliance, with each area handled methodically throughout the process.

Phase-1. Discovery and Research

At this stage, the focus is on understanding who the portal is being built for, whether that’s policyholders, agents, or internal operations teams. It involves mapping current workflows, spotting inefficiencies, and defining what the platform actually needs to achieve. The decisions made here influence everything that follows, from architecture choices to feature priorities, which is why this phase usually has the biggest impact on the success of the project.

- Map existing insurance systems

- Identify key user roles

- Define success metrics before development begins

Phase-2. Architecture Planning

This is where the technical foundation gets defined. Insurance software developers decide how the insurance portal will connect with existing systems, which integration approach makes sense, and how data will flow consistently across platforms without breaking what’s already working.

- Define API contracts between the portal and the core insurance systems

- Set up CI/CD pipelines

- Plan data encryption and identity management controls

Phase-3. UI/UX Design and Prototyping

In this stage, UI/UX designers will create visually appealing and user-friendly interfaces. They will understand how policyholders, agents, and internal teams actually interact with insurance processes, then design around that before development begins. Clickable prototypes are tested with actual users.

- Build personas based on real user behavior

- Map end-to-end journeys

- Test designs against WCAG 2.1 AA accessibility standards

Phase-4. Development and Integration

Insurance portal software development is done in sprints, starting with the MVP, which includes only the essential features needed to make the portal useful. During this phase, the frontend, backend, and integration layers are built, and the required workflow automation is also set up.

- Run regular sprint demos for early feedback

- Enforce security checks within the development pipeline

- Develop data migration scripts alongside features

Phase-5. Testing and Compliance Validation

In this phase, the QA team runs functional, performance, and security tests across every portal flow. This includes test cases for user authentication, permission controls, claims and payment workflows, API integrations, and data encryption to verify the platform is stable, secure, and production-ready. Any issues found get fixed before moving forward. Compliance checks GDPR, PCI-DSS, HIPAA are validated at this stage itself, not after the portal goes live.

- Use synthetic data for claims testing

- Test high-traffic flows

- Run penetration testing

Phase-6. Deployment

Once the insurance portal passes all testing stages, it is prepared for deployment. A full rollout on day one is usually not the best approach. Instead, starting with a pilot helps gather real-world feedback before the portal handles full traffic. Running the old and new portals in parallel during the transition keeps operations stable throughout.

- Run the legacy and new portals in parallel during the transition

- Use canary deployments, release to 5% of users before full rollout

- Monitor error rates and system load in real time

Phase-7. Post-Launch Support

If you think that the job is done after the launch, then no, it’s just the beginning. In fact, the real work starts after that. Users will run into things that no testing environment could predict, like slow load times, confusing flows, and edge cases in claims or payments. Keeping a dedicated support cycle in place for the first few months makes a significant difference in how well the portal actually performs.

- Track business metrics like FNOL rates

- Schedule regular security patches and compliance updates

- Monitor user behavior to identify friction points and usability gaps

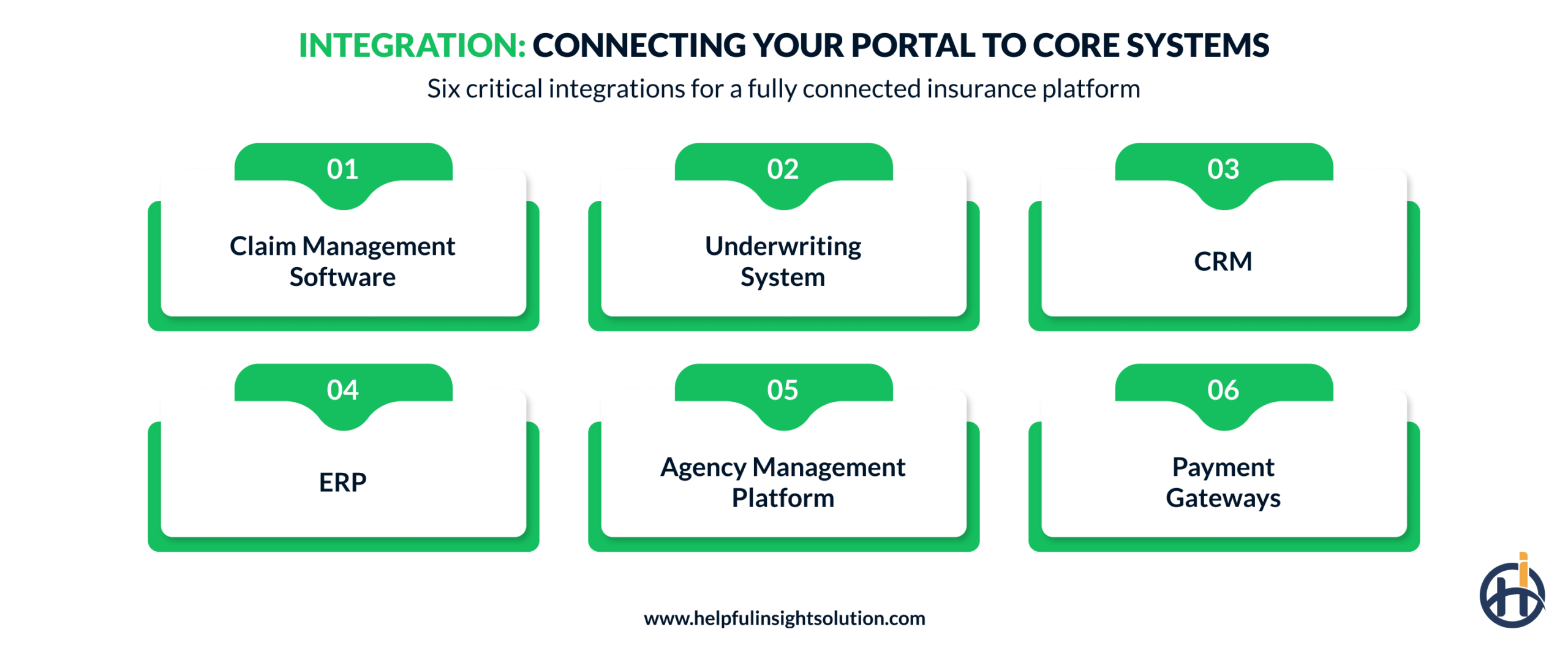

Integration: Connecting your Portal to Core Insurance Systems

Most insurance companies already have core systems like policy administration, claims platforms, payment gateways, and CRMs. The portal needs to connect with all of them to work efficiently. How well those integrations are built directly impacts data accuracy, processing speed, and how much operational overhead actually gets reduced.

Claim Management Software

Without this integration, claimants have to call just to file claims or check updates. Connecting the insurance portal to a claims management system lets them submit and track everything online, making processing faster and reducing manual work.

Underwriting System

Manual underwriting for simple cases can slow things down. Connecting the portal to an underwriting engine automates risk checks, delivers instant quotes, and accelerates policy issuance, keeping the process consistent and efficient at scale.

CRM

Many insurers already know, but don’t always act on the fact that decisions are often made without the full picture. A CRM integration fixes that by bringing policies, claims, and customer interactions together. So when a renewal comes up or a customer calls in, teams actually know what’s going on.

ERP

Financial data and transactions shouldn’t require someone to manually keep them in sync. When your portal connects to your ERP, it happens automatically. Billing runs automatically, and reporting gets much cleaner.

Agency Management Platform

Agents already have enough to manage, and jumping between systems to quote and bind policies only adds to that load. Integrating the agency management platform directly into the portal gives agents everything they need in one place, like client data, policy status, and binding capabilities, so things move faster without the unnecessary switching.

Payment Gateways

From paying premiums to renewals, policyholders expect to handle all of it online. Integrating a secure payment gateway makes real-time transactions possible, supports multiple payment methods, and even sends automated receipts.

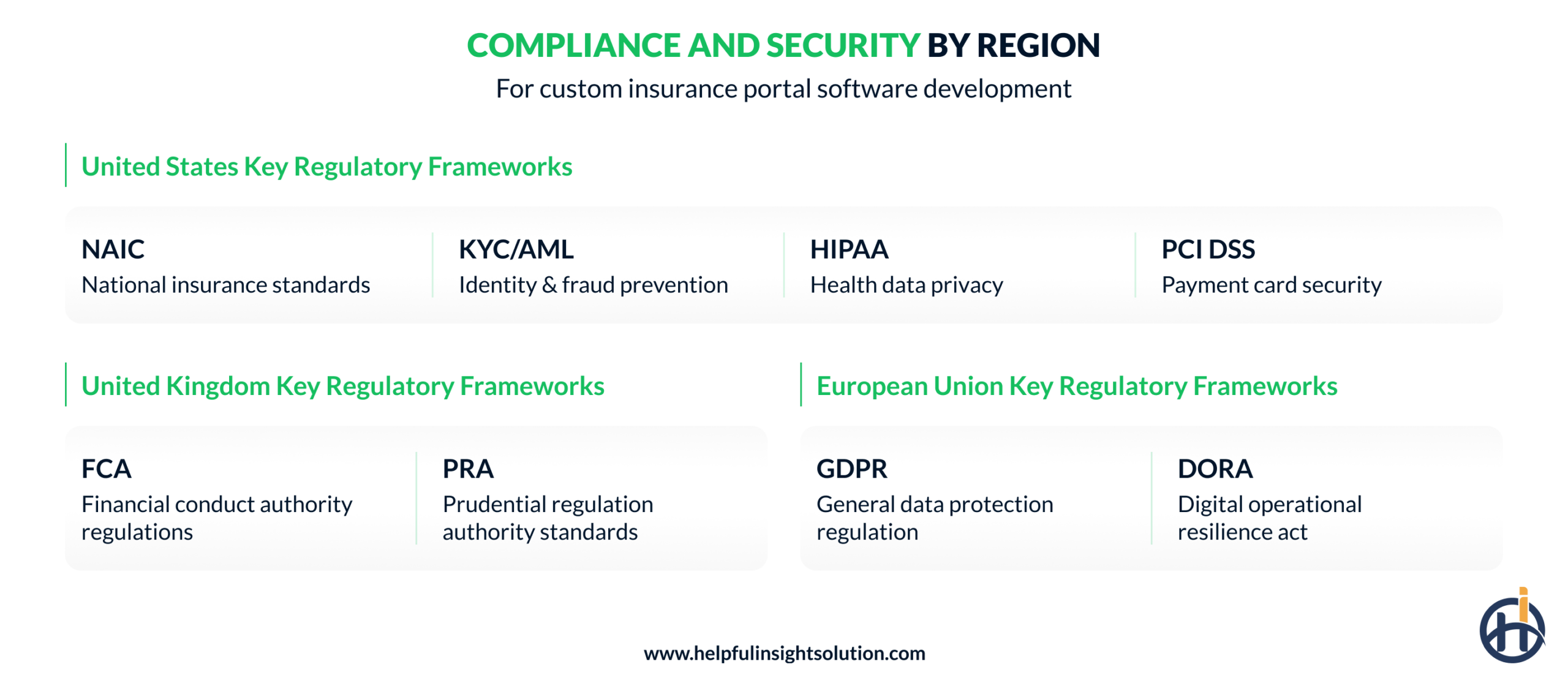

Compliance and Security by Region for Custom Insurance Portal Software Development

Where you operate shapes what your portal needs to comply with, and those requirements usually go deeper than most teams initially expect. Data privacy laws, security standards, and claims regulations vary by region and need to be factored into the build early. Here’s a regional breakdown of the key compliance and security requirements to plan around.

United States (USA)

NAIC (National Association of Insurance Commissioners)

NAIC sets the baseline rules for how insurance companies operate across US states. Your portal needs to align with these standards depending on which states you’re licensed to operate in.

KYC/AML Compliance

Before onboarding any customer, insurers need to verify who they are and flag suspicious activity. This isn’t optional so regulators expect it, and skipping it creates serious legal consequences.

HIPAA (Health Insurance Portability and Accountability Act)

If your portal handles any health-related insurance data, HIPAA applies — it governs how that data is stored, accessed, and shared across every touchpoint. The compliance requirements here go deeper than most teams initially expect, and health insurance software development carries a different level of technical and regulatory complexity compared to standard property or auto insurance portals. A breach doesn’t just cost money; it damages trust in a way that’s very difficult to recover from.

PCI DSS (Payment Card Industry Data Security Standard)

Every time a policyholder pays a premium online, PCI DSS rules apply. It sets the security standards for handling card payments and protecting that data from the moment it’s entered.

United Kingdom (UK)

FCA (Financial Conduct Authority) Regulations

The FCA controls how insurance products are sold and how customers are treated. Your portal needs to meet their conduct standards from how policies are presented to how complaints are handled.

PRA (Prudential Regulation Authority) Standards

It focuses on financial stability. For insurers, this means web portals underlying operations need to demonstrate that the business can handle risk without putting policyholders at financial risk.

European Union (EU)

GDPR (General Data Protection Regulation)

Any policyholder data agents collect, store, or process falls under GDPR. Users have the right to access, correct, or delete their data. Non-compliance comes with fines that are hard to ignore.

DORA (Digital Operational Resilience Act)

DORA came into effect in January 2025 and applies directly to insurers operating in the EU. It requires insurance portal software and its third-party tech dependencies to meet strict digital operational continuity standards.

Insurance Portal Development Cost: Full Breakdown

There’s no doubt that insurance portal software development involves significant costs, so concerns about pricing are completely natural. The overall cost depends on a range of factors, including:

Portal Type and Complexity

A simple self-service portal and a multi-user platform with claims and billing modules are very different builds. So naturally, the more you’re asking the portal to do, the more it’s going to cost to build it.

Features

Every feature you add takes time to build and test. Basic features like policy access are usually less costly. But when you start adding advanced features like AI-powered capabilities, the effort increases and so does the overall cost.

Number of Integrations

The more systems your portal needs to connect with, the more work and cost is involved. Integrating with CRMs or ERPs takes time, especially if you’re dealing with legacy systems that aren’t easy to connect.

Technology Stack Selected

The tech stack software developers select to build insurance platforms affects both upfront cost and long-term maintenance. Some technologies need specialists who charge more. Others are cheaper to build but expensive to scale.

Compliance and Security Standards

If you think meeting compliance standards like GDPR and PCI-DSS is optional, it’s not. It definitely adds to the cost. Security audits, penetration testing, none of it comes free. And cutting corners here usually ends up costing more later than it saves upfront.

Development Team Location

Where your portal development company is based makes a noticeable difference in the cost. Teams in North America or Western Europe usually charge higher hourly rates, while teams in parts of Asia can offer similar quality at more affordable rates.

Keeping all the above factors in mind, it’s difficult to give an exact figure. But here’s a rough idea of the cost range for digital insurance portal development based on complexity:

| Complexity Level | Estimated Cost Range |

| Simple Portal | $25,000-$80,000 |

| Mid-Level Portal | $80,000-$200,000 |

| Highly Complex Portal | $200,000-$400,000+ |

Want a more accurate estimate? Share your project details with our team, and we’ll help you with a custom quote.

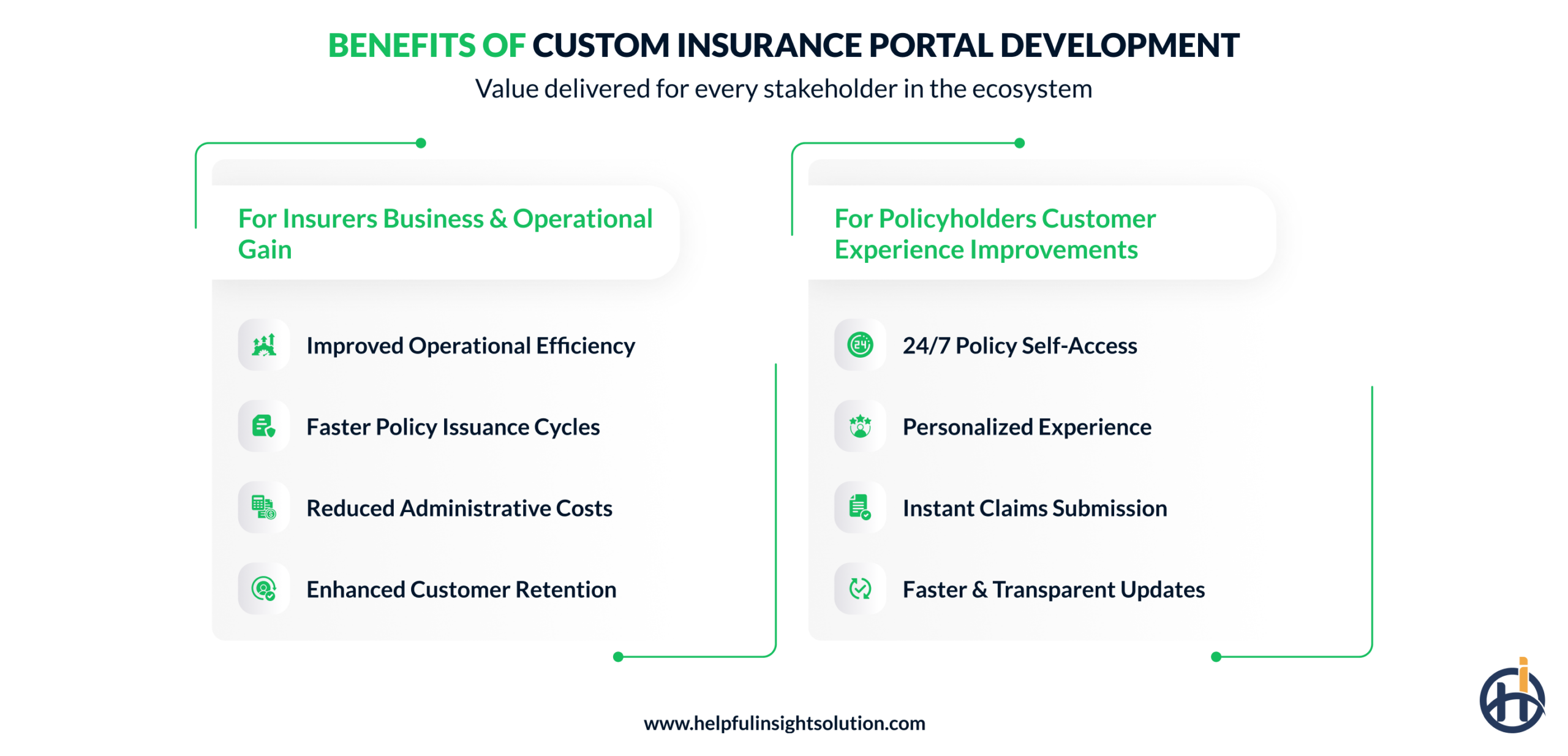

Benefits of Custom Insurance Portal Development

Investing in custom insurance portal development is a strategic decision for insurers and insurtech companies focused on long-term operational efficiency and customer experience. When designed around specific business workflows, compliance requirements, and user expectations, a custom portal delivers measurable value for both insurers and policyholders.

From streamlined policy operations to improved digital engagement, the right portal infrastructure supports scalable growth and better service delivery, much like how insurtech startups are reshaping insurance from the ground up.

Let’s explore the advantages of developing an online insurance portal.

For Insurers

Improved Operational Efficiency

Just like any other business, insurtech companies want to run their operations more efficiently. Insurance work involves a lot of routine tasks, like updating policies and handling documents, which don’t always need a person. A custom portal can take care of these tasks, freeing insurers to focus on work that really needs their skills.

Faster Policy Issuance Cycles

Nobody wants to wait days for a policy when it can be issued in minutes. Digital insurance platform automates validation checks and digitizes the application process. What used to take hours now happens almost instantly, and that speed directly affects how many customers you win before a competitor does.

Reduced Administrative Costs

Manual processes can be costly not just because of salaries, but also due to errors and the time spent fixing them. An insurance agent portal that automates renewals, payment reminders, and claims submissions reduces much of this work. Over time, those savings add up and a year in the drop in operating costs is hard to ignore.

Enhanced Customer Retention

Most customers don’t leave because they found a cheaper policy. They leave because dealing with their insurer became too much effort. When checking a policy or filing a claim takes minutes instead of phone calls, customers tend to stick around. Customer experience matters, and a well-designed portal can make it much easier.

For Policyholders

24/7 Policy Self-Access

For a policyholder, one of the first things that stands out is access. Not limited to office hours and not dependent on whether an agent is available. With a portal, they can log in at any time, check coverage details, and download documents. This really means a noticeable difference in how manageable the policy feels.

Personalized Experience

Who doesn’t like getting special attention? Everyone does. With an AI-powered insurance portal, customers see relevant policies and coverage suggestions based on their actual profile rather than sorting through products that don’t apply to them. That level of personalisation depends heavily on how the AI layer is built , AI development for insurance isn’t the same as adding a recommendation widget, it requires training on domain-specific data and integrating with policy logic that varies by product type.

They don’t have to sort through unrelated products and are less likely to choose something that doesn’t truly fit.

Instant Claims Submission

Filing a claim used to mean paperwork, branch visits, and repeated follow-up calls. A claims management portal changes that. Policyholders can upload documents, enter details, and submit everything from home. The guided process also helps reduce errors that often cause unnecessary delays down the line.

Faster and Transparent Updates

Not knowing where things stand is one of the more frustrating parts of the insurance experience. A web portal gives clear visibility at every stage, whether it’s a claim, policy update, or request under review. Policyholders stay informed without having to follow up repeatedly, and they know when action is needed from their side.

Common Challenges in Insurance Web Portal Development and Their Solutions

Enterprise insurance portal development is rarely a straightforward process. There are real challenges that come up along the way, some technical and some operational. Here’s a look at the common ones and how to deal with them.

Legacy System Integration

Challenge

Older systems weren’t built to connect with modern platforms. Getting them to communicate with a new portal without disrupting live operations takes careful planning and the right technical approach.

Solution

Middleware layers and API gateways are typically the most reliable way to bridge older systems with a new portal — they keep live operations stable while data flows consistently between platforms.

For insurers, this is usually where Insurance IT services become relevant, since the challenge is less about building the portal and more about connecting it to infrastructure that was never designed to integrate with modern software.

One of our clients in the USA had a legacy claims platform with no native API capability and a completely proprietary data structure. We built a middleware layer that translated data between the old system and the new portal, managing schema mapping and real-time sync independently. The integration was rolled out in controlled phases, with data integrity checks at each stage, and their live operations continued without any disruption.

Data Security and Compliance

Challenge

Insurance portals handle sensitive data, payment information, and health records. One security gap doesn’t just create a compliance issue; it can permanently damage customer trust and attract serious regulatory penalties.

Solution

Build security into the development process from day one. This means setting up role-based access controls so each user type only sees what they are supposed to, adding multi-factor authentication across all portal logins, and encrypting data both in transit and at rest. Moreover, penetration testing and compliance validation should happen during the build, not at the last minute.

Poor User Experience Design

Challenge

A portal that’s hard to navigate doesn’t get used. If policyholders or agents can’t figure out how to do something quickly, they’ll call in instead which defeats the whole purpose.

Solution

Dedicated insurance portal developers should design around real user behavior by prototyping key journeys early, testing with actual users, and fixing issues before development begins rather than after the portal is already built.

A client came to us with a portal that had been live for months but policyholder adoption was low. We ran a full UX audit and mapped exactly where users were getting stuck. The flow had been built around internal process logic rather than actual user behavior.

We restructured the submission journey, simplified the field architecture, and added inline guidance at the highest drop-off points. Support volumes around claims queries came down significantly in the weeks following the update.

High Development Costs

Challenge

Insurance self-service portal development isn’t cheap, and costs can spiral quickly when scope isn’t defined clearly upfront. Many businesses end up paying for rebuilds or feature fixes that could have been avoided with better planning.

Solution

Start with a simple MVP. Focus only on the most important features first. You can always add more later, and that’s usually cheaper and easier than building everything at once.

What’s Next for Web-Based Insurance Portal: Future Trends

Insurance portals have already changed how day-to-day operations run. But the more important question is where they’re heading next. Some of these advancements are already in early deployment, and insurers building portals today should design with them in mind.

Conversational Portals Powered by LLMs

Current insurance portal chatbots perform well for basic queries, but often struggle with more complex policyholder requests. Large language model (LLM)-powered portals address this limitation by enabling more contextual, human-like interactions. Insurers planning this capability should work with an experienced LLM development company rather than bolting a generic chatbot onto an existing portal.

When users ask questions beyond predefined scripts, the system can deliver clear, accurate responses in natural conversation. For insurers, this reduces support dependency and allows the portal to handle a broader range of customer inquiries efficiently.

Autonomous Claims Settlement Without Human Intervention

Simple claims are already being processed faster with automation in the insurance industry. What’s coming next takes that further. The portal reads the submitted photos, cross-checks the policy, calculates the payout, and releases the payment, without an adjuster touching it.

For simple cases, settlement could happen within minutes of submission. Insurers still handling these manually are carrying a cost they don’t need to.

Underwriting Through IoT and Wearable Data

In the future, we can see insurance software fetching live data from smartwatches, home sensors, and connected devices to reassess risk on an ongoing basis. Your coverage recommendations could be updated based on how you actually live, not just a snapshot from years ago.

Micro-Insurance Portals for On-Demand Coverage

Micro-insurance is already growing. What changes is the infrastructure behind it. Future portals will handle thousands of short-term, on-demand policies simultaneously, coverage switched on for a single flight, a rental car, or a weekend event. The portal manages the entire transaction in real time without any manual processing on the insurer’s side.

How to Choose an Insurance Portal Development Company: Questions to Ask

Looking for the best insurance portal development company? The partner you choose can make or break your project. An inexperienced team doesn’t just slow things down it can cost you months and sometimes means starting over. So before you commit, here are a few questions worth asking.

Do you have experience building insurance-specific web portals?

General web development experience alone is not enough here. Working with a specialized software development company that understands insurance workflows, compliance requirements, and system dependencies makes a measurable difference to the outcome.

Insurance comes with its own workflows, compliance requirements, and system dependencies. A team without experience in this industry may end up learning as they go, and that usually affects both your budget and timeline.

Can you share a portfolio of past insurance projects?

Many companies claim to offer insurance portal development services, but a proven portfolio demonstrates actual industry experience. Review the insurance solutions they have built, the business challenges those platforms addressed, and whether their experience aligns with your operational requirements, workflows, or customer expectations.

How do you handle integrations with legacy systems?

Most insurance businesses already have systems running like CRM, billing, and claims platforms. The portal has to work with all of that. If the company hasn’t dealt with legacy integrations before, you’ll find out the hard way halfway through the project.

What security measures do you build into the portal during development?

Security should be treated as a foundational requirement, not a final checklist item. During vendor evaluation, it is worth asking specifically how encryption, access controls, and compliance validation are handled. A technically capable insurance portal development partner will have clear, detailed answers to those questions without needing to deliberate.

Do you offer post-launch support?

Vendor support after launch is worth evaluating as carefully as the development capability itself. Before committing, establish what post-launch support looks like in practice for the team you are planning to hire. Response time expectations, issue escalation processes, and whether maintenance is included in the contract are all questions that need clear answers before the project begins.

FAQs

The cost to develop an insurance portal is influenced by multiple variables like project complexity, portal type, platform chosen, features, UI/UX design, regulatory requirements, developer’s location, and many more. A basic portal typically starts around $25,000 to $80,000, while a more advanced portal can range from $80,000 to $200,000 or more.

The timeline for the enterprise insurance portal development is impacted by a wide range of factors. These include project scope, feature complexity, design, third-party integrations, data migration, and testing. A minimum viable product (MVP) can take approximately 3 to 6 months, while a more complex portal may take 6 to 12 months or longer.

There is a broad range of portals insurance companies can consider building such as:

- Insurance self-service portal

- Underwriting portal

- Insurance comparison portal

- Agent portal

- Risk services portal

- Insurance claims management portal

Yes, and it’s something we prioritize in every portal we build. Most policyholders manage their insurance from their phones today, so we will help you develop a portal that works smoothly on all devices.