Key Takeaways

- Fintech development outsourcing means an external team builds and maintains part or all of your finance software, with people who already understand settlement, ledgers, and compliance.

- Finance companies outsource mainly for compliance-ready teams and the ability to scale up for a launch and back down afterward.

- Almost any part of the project can be outsourced, including the app, payment and API integration, fraud systems, modernization, and managed services.

- Cost depends on scope and where the team sits. A fintech MVP costs roughly $30,000 to $75,000 offshore, while a full application costs $100,000 to $300,000.

- The safest engagements name the regulator in the contract and keep ownership of code and encryption keys with you.

- Choose a partner with real finance experience and its own security posture, not just on price.

The way money moves changes with the country, so a payment in India runs on UPI while the same feature in the US settles over ACH.

Fintech development outsourcing gives you a team that has already integrated these rails and handled their failure cases, like a delayed settlement or a reversed transaction.

The UAE adds its own systems again, and a partner who has worked across them helps with fintech product development that meets the specific regulations.

This blog will help you understand what fintech development outsourcing means, why finance companies use it, what you can outsource, how the process works, what it costs, and how to choose a partner.

What is fintech development outsourcing?

Fintech development outsourcing refers to a contract where an external partner owns part or all of the software development and post-deployment work, including maintenance, monitoring, and compliance updates.

It differs from general software outsourcing because of the domain.

The team working on your project must understand financial concepts like settlement, payment rails, double-entry accounting, KYC and AML workflows, along with the reporting a regulator expects, so they are not learning the business while building it.

The scope of what can be outsourced varies depending on your needs. Some companies outsource the full project from initial consulting to development, testing, and deployment.

Some companies have a core in-house team and bring only dedicated fintech developers for specific jobs like payment integration or a KYC module.

So, both startups and enterprises can use it. The more practical question is why finance companies outsource in the first place.

Why finance companies outsource fintech development

Outsourcing becomes the right choice when a development project needs skills your team does not have on payroll.

Fintech is among the most volatile and fastest-growing markets, on track to be worth $460.76 billion in 2026 and $1,760.18 billion by 2034, at a CAGR of 18.20%. When a market grows that quickly, a partner who keeps you compliant and improves customer experience often becomes a necessity.

The first of those reasons is the compliance layer, which is where most in-house timelines fall.

An experienced fintech software outsourcing company usually has certifications like PCI DSS and SOC 2 and has passed real audits, so you inherit that posture that is already proven. Therefore, you can expect your product to be shipped faster, that too with no to minimal revisions needed.

The partner has shipped financial products before, including payment reconciliation and identity verification, among others.

They can reuse proven designs that already handle the edge cases, so your first version behaves like a mature one, and your own team stays on the parts only you can define.

Outsourcing is also the right choice when your existing team has limited capacity to keep up with the timelines of your project. It lets you scale up for the release and down afterward, which is why it fits a one-time migration and a long roadmap equally.

Fintech outsourcing has become mainstream for this reason, with the IT services outsourcing market set to reach $1.22 trillion by 2030 at 8.6% a year.

Benefits of Fintech Development Outsourcing

In finance, an outsourcing benefit only counts if it reaches the revenue line or the risk register. These four do.

Faster, Compliant Market Expansion

Every new market fintech steps into comes with its own regulations, and satisfying each one is where most of the time gets spent.

A partner that has already built under India’s RBI and the US SEC, and dealt with the UAE Central Bank too, can carry the same product into a new market and accommodate its reporting and data-residency rules for it, without studying each regulator from scratch. So, you get a partner who can turn months of legal and engineering discovery into a scoped piece of work.

A Lower Cost of Change

Finance is a highly regulated industry; therefore, to stay compliant, organizations must adapt to changes. For example, a new payment rail launches or a regulator updates a reporting format, and the product has to follow. The same is true when an open banking standard changes.

A fintech software development partner can update your existing system in a modular, documented way to ensure specific changes can be made while other services remain unaffected. Also, the cost of each change stays low, because the architecture is designed to accommodate it.

Stronger Fraud and Security Tooling

Fraud is a constant cost in finance, more than almost any other industry where money is involved. The challenging part is preventing fraud without also declining legitimate customers, since every false decline is a lost sale and often a closed account.

A fintech development company that has built and run financial products brings best practices that already work, like device fingerprinting and velocity limits tuned on live traffic. It also reads behavioral signals that tell a routine login apart from an account takeover attempt.

Infrastructure Built for Volume Spikes

A fintech platform spends most of the month at a steady, predictable load. However, during a festive sale or salary day, transaction volume can spike ten to a hundred times within a couple of hours.

A system not built for that surge either slows to a crawl or fails outright, and both cost you in revenue and reputation.

A fintech product can be hosted on the Elastic Cloud Infrastructure, so services on AWS Auto Scaling or Kubernetes add instances as traffic climbs and shed them once the peak passes, and you pay for the extra capacity only while the surge lasts.

Fintech software development services you can outsource

A fintech organization has several interconnected systems, each of which needs different development methodologies.

Understanding what each covers makes it easier to decide what you can outsource and what must be managed internally.

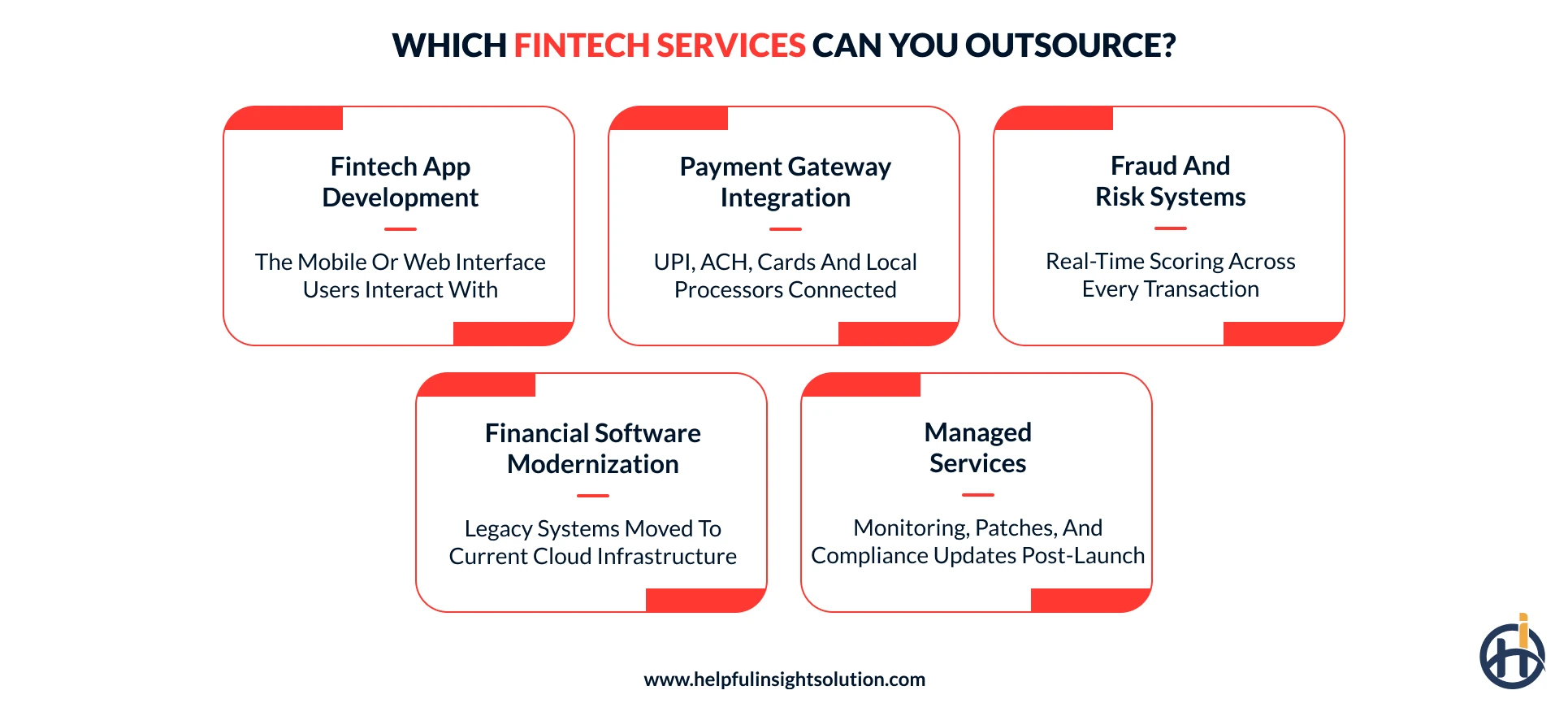

Fintech App Development

A fintech app is the part users touch: the mobile or web app where they open an account, check a balance, or make a payment. Demand for it keeps climbing as more finance moves to the phone, and North America alone held 32.30% of the global fintech market in 2025, the largest share of any region.

A fintech app is not a one-person job. It usually needs a UI/UX designer, developers for the front and back end, and a QA engineer to test every payment path before release. In the US, those roles are among the best paid in tech.

According to the BLS figures, a median US developer alone earns $133,080, so a small in-house team runs about $330,000 a year before benefits, often more than outsourcing the entire build.

Therefore, fintech app development is one of the most outsourced finance products, especially for its blend of front-end design and compliance-intensive engineering.

Payment Gateway Integration

A payment gateway is the backbone of every fintech product development. Every transaction passes through a payment gateway, the layer that moves money between the customer, the bank, and the card network. The volumes are enormous.

In India, UPI alone processed 22,716.07 million transactions worth ₹ 28.92 lakh Cr in June 2026, and at that scale, even a small failure rate turns into thousands of broken payments.

A product may need UPI in India, ACH and cards in the US, and a local processor in the UAE, each with its own message format and settlement timing. Anywhere the card data is handled, the work also has to stay inside the PCI DSS scope, which shapes how the whole flow is built and where data is stored.

This is why payment gateway integration is so often handed to a fintech software outsourcing company that has wired these rails before. They bring tested connectors and design for failures like a timeout or a reversal, so money is never lost in between, and they run the reconciliation that proves every payment landed.

Fraud and Risk Systems

Fraud and risk systems are the layer that decides, the moment a payment is made, whether to let it through or hold it for another check. The problem they fight keeps growing. In the US, consumers reported losing about $16 billion to fraud in 2025, the highest figure on record, according to the FTC.

Every financial software development project has to plan to mitigate such risks.

Most financial products combine a rules engine for known patterns with a machine-learning model that scores each transaction on risk in real-time. Keeping these models accurate as fraud tactics shift is the hardest part. A model that was effective six months ago may already be missing new attack patterns.

This is data-heavy work that improves with scale, which is why fraud and risk systems are often outsourced to a fintech development company that tunes these models across many clients.

Financial Software Modernization

If you have been using legacy software, then you might face challenges in serving today’s customers and connecting to different modern systems.

Modernization moves that legacy financial software onto current cloud-based systems, and demand for it is rising. The application modernization market is set to reach $92.08 billion by 2034, up from $30.36 billion in 2026, with a CAGR of 14.88%.

Modernization is beyond rewriting the software. A core system has carried years of business rules that are hardly documented, so a team has to move it without breaking the transactions running through it every day. Most modernization happens in stages, replacing one module at a time while the old and new systems run side by side.

It is defined work with clear goals, which is why financial software modernization is a strong fit for financial software outsourcing. A partner that has migrated finance systems before can help you plan the modernization, mitigating the risks.

Managed Services

A fintech product is never finished at launch; it needs constant upkeep, like monitoring, security patches, releases, and updates each time a regulator or a rail changes its rules.

Finance managed services cover the ongoing work that comes after the deployment of a fintech product.

In finance, an outage is more than downtime, since a payment service that goes down stops transactions and can breach an uptime obligation at the same time.

Managed services safeguard you against that, keeping a dedicated team ready to patch a vulnerability or restore a service before it becomes an incident, and keeping you compliant as regulations grow.

Managed services keep a dedicated team working on the system, ready to patch a vulnerability or restore a service before it turns into an incident.

Keeping a full team on call around the clock is hard for a small company, which is why maintenance and support are among the most common fintech outsourcing services.

A partner handling upkeep frees your own engineers for new features, and the support usually sits in the same contract as the original build.

How does the fintech development outsourcing process work?

Fintech development outsourcing follows a predictable path, whether you are outsourcing a single module or an entire platform.

Here we have outlined the stages most outsourcing projects walk through and what happens at each stage.

1. Scope and Discovery

Every fintech product development project starts by defining what you are building and the rules it has to meet. You and the fintech software outsourcing agency should agree on the features and the regulators in play, then decide which part to outsource.

Having a clear roadmap at the early stage will help you ensure that the project remains on the right track.

2. Pick the Outsourcing Engagement Model

Next, you choose how the work is structured. Some companies sign a fixed-scope contract for a defined build, while others bring in dedicated developers who work as an extension of their own team.

This is also where the NDA and the statement of work get signed, setting out ownership and timelines.

3. Design and Compliance Architecture

Before writing the code, the first step a software development company follows is mapping the architecture, and in finance that means designing for compliance from the start.

They must consider your requirements like PCI DSS and data-residency rules, along with the audit logging a regulator will expect later.

4. Build in Sprints

Development is often completed in short cycles, known as sprints. Each sprint can be seen as a milestone for completing specific parts of the project. So, you can see progress and can adjust the roadmap while it is still inexpensive to change, instead of waiting months for a single big reveal.

5. Test, Audit, and Secure

A finance product is not ready just because it works. It goes through functional and security testing, including a penetration test and a compliance check against the rules set at the start. Fixing an issue here costs far less than after real money is flowing.

6. Launch and Maintain

Once it clears testing, the product goes live, often in a phased rollout so any issue shows up small. From there, it moves into managed services, where the partner keeps it monitored and patched as rails and regulations change.

Timeline and team size drive the cost, which the next section breaks down.

Fintech outsourcing cost: what shapes the price?

Fintech outsourcing cost has no specific figures, it is subject to factors such as the scope of the work and where the team sits.

Location is one of the biggest factors in driving the fintech outsourcing cost in 2026. Rates vary widely, and 2026 outsourcing data shows how far.

| Region | Typical 2026 hourly rate |

| India / South Asia (offshore) | $25-$45 |

| Eastern Europe (nearshore) | $30-$75 |

| United States (onshore) | $100-$250 |

Here is how these costs are translated in a fintech project outsourcing:

- A fintech MVP: Around $30,000 to $75,000 for a working first version with important features for market testing.

- A full fintech application: Around $100,000 to $300,000 once compliance and integrations are added.

- Payment gateway integration: Around $10,000 to $40,000, depending on how many rails you connect.

- API and open banking integration: Around $8,000 to $30,000, based on the providers involved.

- Fraud and risk systems: Around $20,000 to $80,000 for the rules and scoring model, plus any third-party tool fees.

- Financial software modernization: Around $50,000 to $200,000, depending on the size and age of the system.

Fintech development outsourcing best practices

Outsourcing a finance product carries risks you can manage upfront if you set the terms well.

The practices below come from what actually goes wrong in fintech IT services outsourcing, and each one heads off a specific problem.

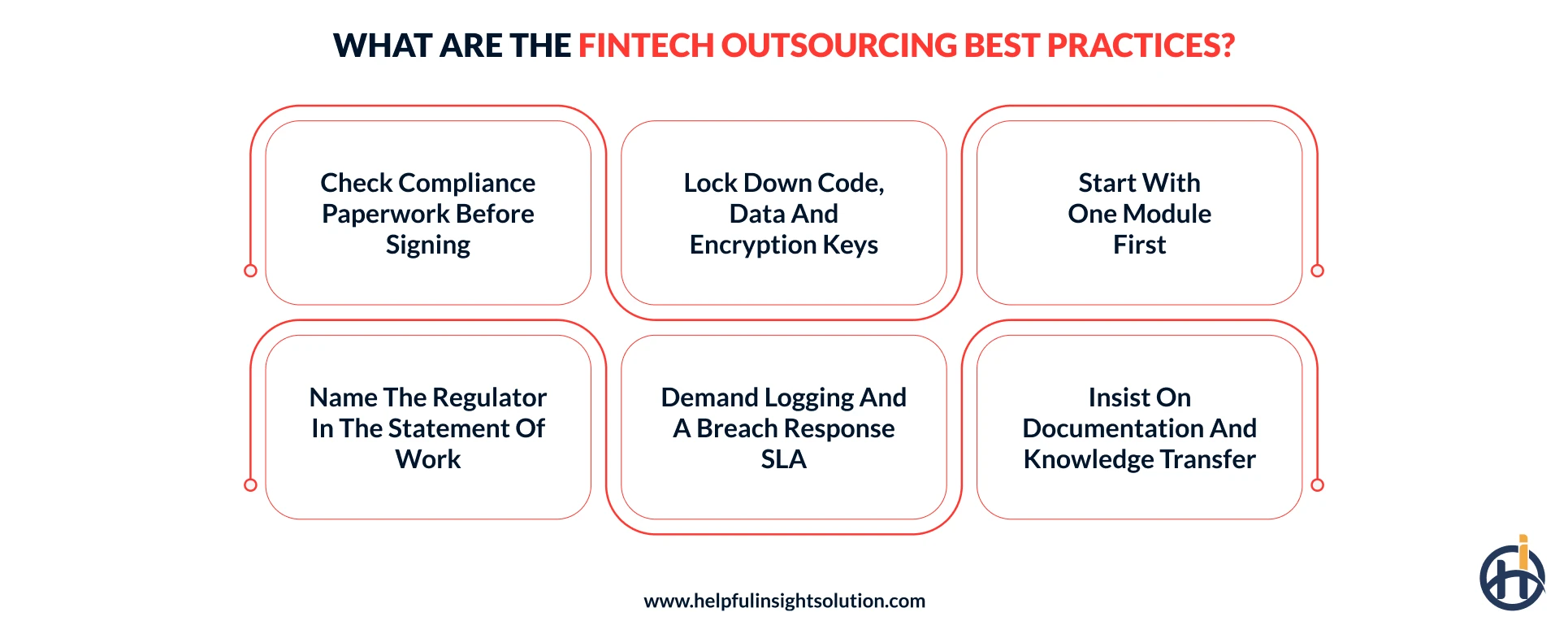

Check the Compliance Paperwork Before You Sign

A fintech outsourcing company that says it is PCI DSS compliant should be able to show a current Attestation of Compliance and a SOC 2 report that covers the scope you need.

Read them, confirm the certification is live rather than lapsed, and check the report actually covers the systems that will touch your data.

A gap in their compliance is a gap in yours the moment real data starts flowing.

Lock Down Ownership of Code, Data, and Keys

The contract must outline clearly that the ownership of all source code and IP is explicitly assigned to you. Also, it must say that you will have ownership over the production encryption keys.

If you are planning to switch partners or bring the in-house team later, then you should also add a clause for repository access and code escrow.

Start With One Module Before the Whole Platform

Outsource a contained piece first, like a KYC flow or a payment integration, and judge the partner on how they handle compliance and edge cases before committing the full roadmap.

A small paid pilot shows you their real code quality, testing rigor, and communication, which no sales pitch can.

Name the Regulator in the Statement of Work

Finance is a highly regulated industry, therefore, the outsourcing company spells out the regulations, such as the RBI, the SEC, or whichever regulator governs it, so data residency and reporting are built to the correct standard from the start.

A build that ignores the right regulator is expensive to fix once it is live.

Demand Logging and a Breach-Response SLA

Require audit-ready logging, keep the right to run your own penetration test, and agree in writing how fast the partner must report a security incident.

Set the notification window in hours, not days. In finance, these are basics a regulator will ask about.

Insist on Documentation and Knowledge Transfer

Make handover documents and code walkthroughs part of the deliverables, so the product does not live only in one vendor’s head.

Ask for architecture notes and runbooks alongside the code. This protects you if a key person leaves or you change partners.

These practices lower the risk before it turns into a problem, and they make the last decision easier, which is choosing the partner in the first place.

How to choose a fintech development company?

When you choose a fintech development company for outsourcing fintech services, the price is only one of the factors to be considered.

Here we have outlined a few of the best practices that you can follow to choose a fintech development company that has experience delivering the expected outcomes.

- Real finance experience: Ask what they have shipped, like a payment platform or a lending system with KYC. It will help you understand whether they have experience working on such projects; if so, you can see their outcomes and choose accordingly.

- Fit with your market’s rules: A partner that has built under your regulator already knows its reporting and data-residency needs. If you are in the US, look for work with the SEC or state money-transmitter rules, beyond just offshore delivery.

- Their own security posture: See how they handle their own data and access. It will help you understand how proficient they are with their internal security. You can ask them how they manage security, and review their portfolio too to see their clients’ security postures.

- Clear communication: Transparent communication is the foundation of every project. Therefore, you must have a project manager and technical lead assigned to your project, so you can reach out to them for project information.

So, if a company checks these boxes, you have found a partner worth talking to. That is where Helpful Insight fits in.

Why Helpful Insight for fintech software outsourcing?

You know your finance business better than anyone. Helpful Insight brings the other half, the development team that keeps a finance product compliant and running, like payment integrations and audit-ready ledgers.

We build software for finance worldwide, so a project starts with people who already know your regulator and your rails. Whether you need a full product or a few dedicated fintech developers, the work fits around what your team already does, not the other way round.

Frequently Asked Questions

Fintech development outsourcing costs depend on the project scope and the partner’s location. On offshore rates, a fintech MVP usually runs $30,000 to $75,000, while a full application with compliance and integrations sits closer to $100,000 to $300,000. Ongoing work like managed services is billed monthly on top of that.

Most of the stack in fintech app development can be outsourced, including app development, payment and API integration, fraud and risk systems, modernization, and managed services. Some companies hand over a full build, while others outsource one module like KYC and keep the rest in-house.

It can be, as long as the partner brings the right expertise and controls. Look for current PCI DSS and SOC 2 certifications, insist on owning your encryption keys, and keep audit rights in the contract. Handled this way, financial software development through a partner can be as secure as an in-house build.

It is subject to your choice. For example, if you have a fixed-scope project, outsourcing might help you with predictable costs with no burden on the team management. While hiring fintech developers, you have an in-house team and are looking for specific skills for a temporary period.

Timeframe is directly proportional to project scope. A simple MVP might be delivered within 1 or 2 months, while a complex product might take between 4 and 6 months. So, the timeframe is not definitive.