Key Takeaways:

- AI in fintech is a set of jobs, not one project. Teams that treat it that way ship, the rest stall after the pilot.

- The market is set to grow from $36.96 billion in 2025 to $241.67 billion by 2034, a 23.2% CAGR.

- Adoption is wide but shallow. 81% of firms use AI, but only 40% have scaled past early stages.

- Fintechs outperformed traditional institutions everywhere: 47% vs 30% on advanced adoption, 56% vs 34% on higher profitability.

- Higher AI spending pays back. Firms spending over $100K a year hit advanced maturity and report stronger profits.

- Fraud detection, credit scoring, and customer support are the use cases that return first.

- Stripe, Plaid, Klarna, and Mastercard prove the value is in scale, not secret technology.

- The hard part is data privacy, cross-market compliance, explainability, and legacy integration, not the model.

- Start with one use case that has a clear return, prove it, then grow.

AI in fintech is the technology everyone says they are using, and far fewer have actually shipped.

81% of financial firms now use AI at some level, yet only 40% have moved beyond the early stages to scaling or transformation.

Have you ever wondered why so many AI plans stall after the pilot? Among all the reasons, one keeps repeating that teams treat artificial intelligence in fintech as a single project instead of a set of very different jobs.

So, the fintech companies that are moving beyond the pilot phase are the ones picking the fintech AI use cases that pay back first, then building out from there.

This blog covers everything you need to know about AI in fintech in 2026, including how it works, the use cases that matter, the numbers behind the adoption, and the challenges teams hit once the models go live.

So, let’s get started.

What Does AI in Fintech Actually Mean?

AI in fintech is software that learns from financial data and uses that learning to make decisions or help people make them. A normal rules-based system only does what it was programmed to do. AI works differently, as it keeps improving as new data comes in, and since financial data is always changing, this matters more than it first sounds

Now, the term itself is where most of the confusion starts. AI in fintech is not a single technology. It is a few separate technologies that ended up grouped under one name, and they do not all do the same job.

The one doing most of the work is machine learning. You train it on old data, like which customers repaid their loans and which ones did not, and over time, it gets good at spotting those same signals in new applications. Most credit scoring and fraud checks run on this. That close relation is also why people usually write AI and ML in fintech together, almost as one term.

Machine learning mainly deals with numbers, though, and a fair share of finance is not numbers. It also has documents, chats, support tickets, and so on. Therefore, natural language processing (NLP) is the part that handles that. It reads what a customer uploads at onboarding, understands a support query, and pulls the important details out of a long contract.

Generative AI came later and builds on that same language ability. The main difference is that it can write back now. It can draft replies and can summarise a customer’s full account history for an agent in a line or two.This shift is part of a broader pattern, and you can see how it plays out across other industries in our roundup of AI trends shaping 2026.

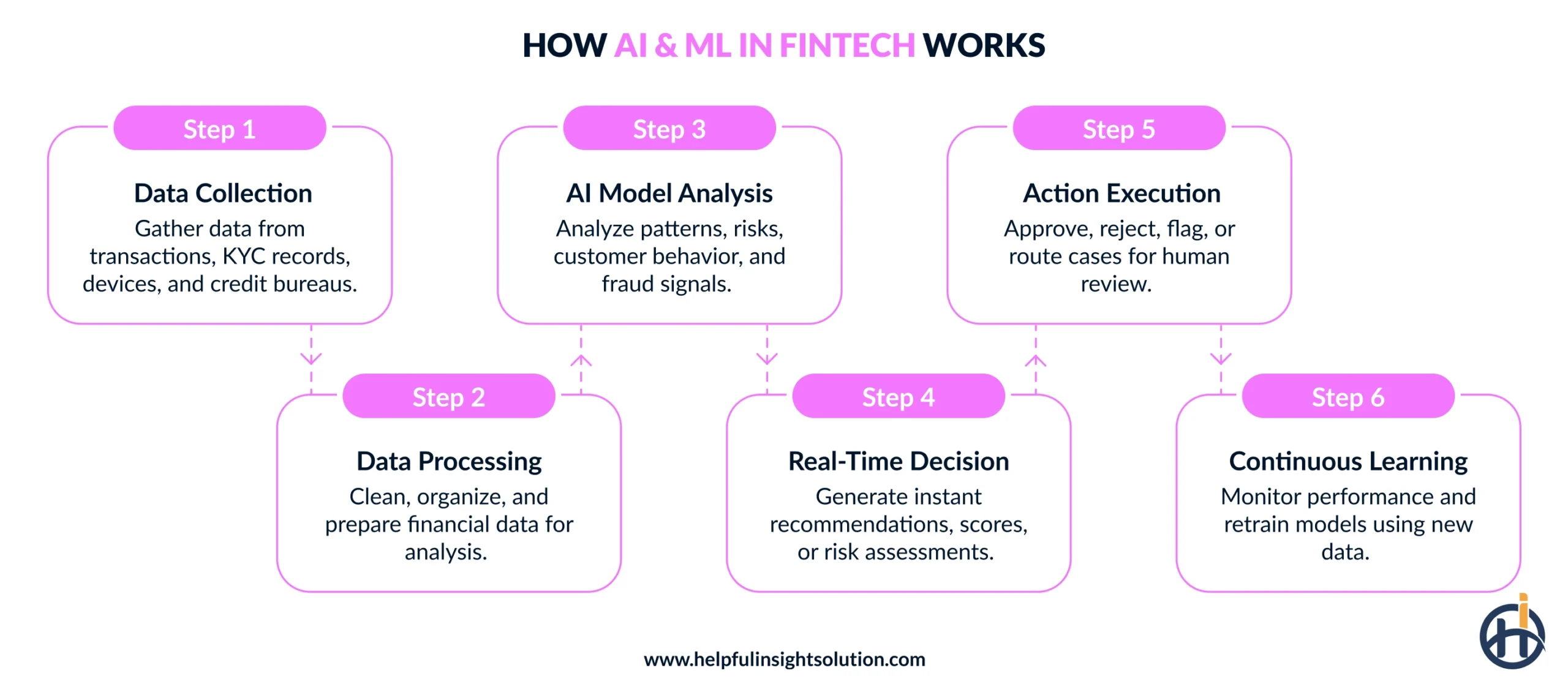

AI and ML in fintech: How it Works?

Simply saying, any AI feature inside a fintech app runs as a connected flow rather than one model doing everything on its own. Once you understand flow, it becomes much easier to see where AI can fit into your product.

The working of the AI and ML begins with the data, and as you know, fintech apps produce a lot. A single decision is made by bringing together the information from different sources, like a customer’s transaction history, their KYC details, the device they are on, and their credit bureau records. The accuracy and result of the AI models depend entirely on the data, so getting their part right is the first and foremost step to be considered.

Once the data is ready, it is shared with the model, which turns it into a decision inside the product, and this often happens in real time. So when a customer makes a payment or submits an application, the model reviews it at that moment and returns a result the app can act on, usually within a second.

As you know, AI and ML in fintech bring automation. So, not every time human involvement is needed, the straightforward ones, like a clearly safe payment or an obviously risky application, are handled automatically, while the harder issues are passed to a team member for a closer look. This way, a human stays in control of the decisions that carry real risk. This balance between automation and human oversight is the same principle behind AI agents in finance, where agents handle routine work and escalate the rest.

The last part of the flow is monitoring, and this is the step most teams underestimate. Customer behaviour keeps changing, and so do fraud patterns, which means a model that worked well earlier can slowly lose its accuracy. However, to avoid that, teams keep monitoring how the model is performing and retrain it on newer data from time to time.

This is why AI and ML in fintech are often considered as a system you maintain rather than a feature you build once. It needs reliable data and regular monitoring to keep performing as your customers and the risks around them keep changing.

AI in Fintech Statistics for 2026

AI is disrupting almost all the traditional processes across industries, including fintech. It has been adopted by almost all fintech companies, from startups to large enterprises, inspired by its potential to deliver improved ROI.

Here we have compiled a list of AI in fintech statistics saying the same thing.

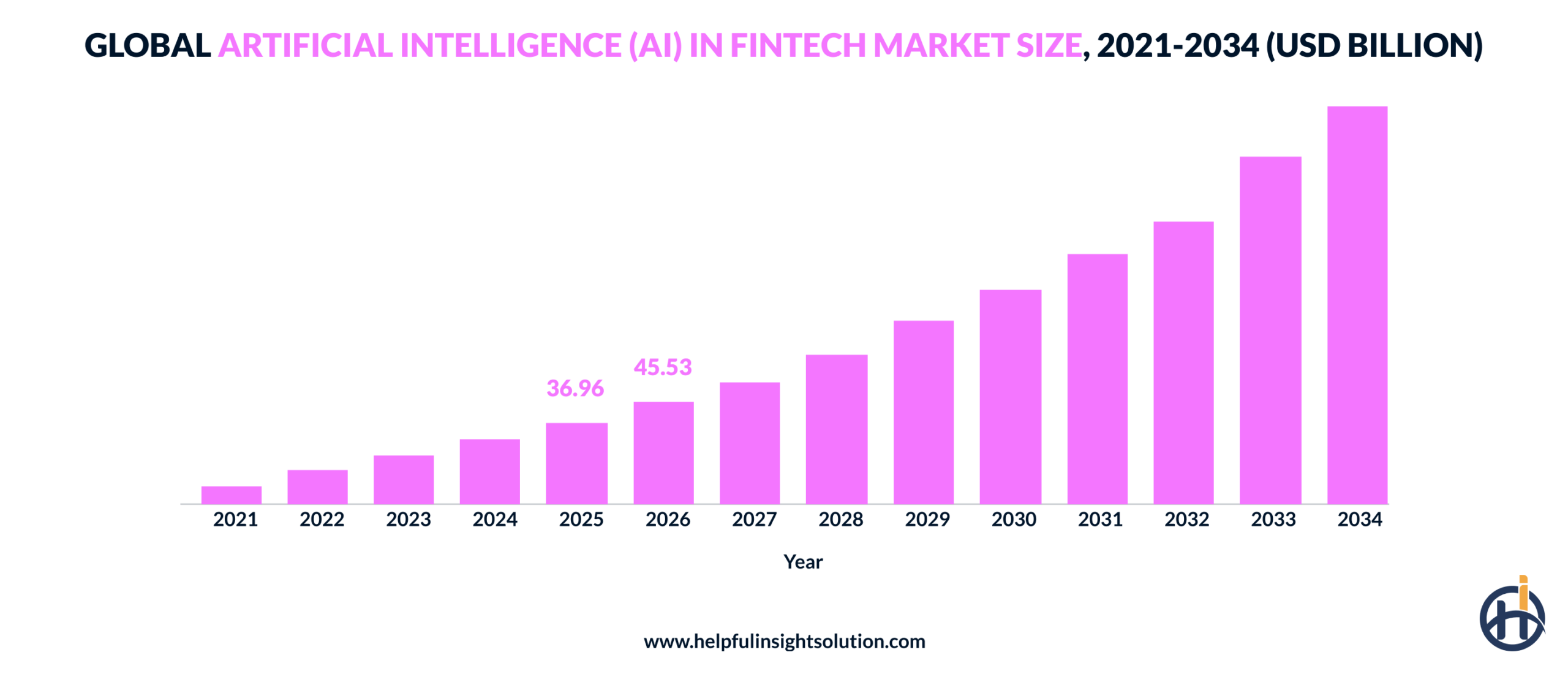

AI in Fintech is a Multi-Billion-Dollar Market

The market size of AI tells the first part of the story. According to Fortune Business Insights, the global artificial intelligence in fintech market was estimated at USD 36.96 billion in 2025 and is expected to reach USD 45.53 billion in 2026, before reaching USD 241.67 billion by 2034 at a CAGR of 23.20%.

The steady growth of the market rarely holds the spending is paying off, and here it is, fintechs and banks reporting the returns.

Fintechs are Adopting AI Faster Than Traditional Institutions

Adoption has already crossed the halfway mark. Research from the Cambridge Centre for Alternative Finance found that 81% of financial firms now use AI at some level, and 40% have reached an advanced stage of it.

The part that matters more for you is the split between fintechs and the older institutions, because the gap is fairly wide.

| Adoption Measure | Fintechs | Traditional Institutions |

| Advanced AI adoption | 47% | 30% |

| Transforming stage | 19% | 6% |

| Agentic AI adoption | 57% | 45% |

| Reporting higher profitability | 56% | 34% |

So, it is obvious that the fintech sector is leading the AI adoption across other industries.

Higher AI Investment is Showing Up in Profits

Profitability is the very first thing against which fintech institutions weigh their investment decisions. Among the finance organisations spending more than USD 100,000 a year on AI, 62% of them reached advanced maturity, and 62% of that group reports higher profitability.

McKinsey says that generative AI could add USD 200 billion to USD 340 billion in value every year, roughly 9 to 15% of operating profits, mostly through productivity for banking institutions.

Customer Support and Fraud Detection are Where AI Starts

Customer support and fraud detection are among the first use cases for AI in fintech.

AI-powered customer support is the most common front-office use case at 74%, and fintechs run ahead at 82%. Fraud detection comes next at 58%, with credit risk modelling at 54%.

Top Use Cases of AI in Fintech

AI applications in fintech are broad, but most of their value comes from a few AI use cases that often repeat across almost every fintech business.

Below, we have discussed some of the most common fintech AI use cases.

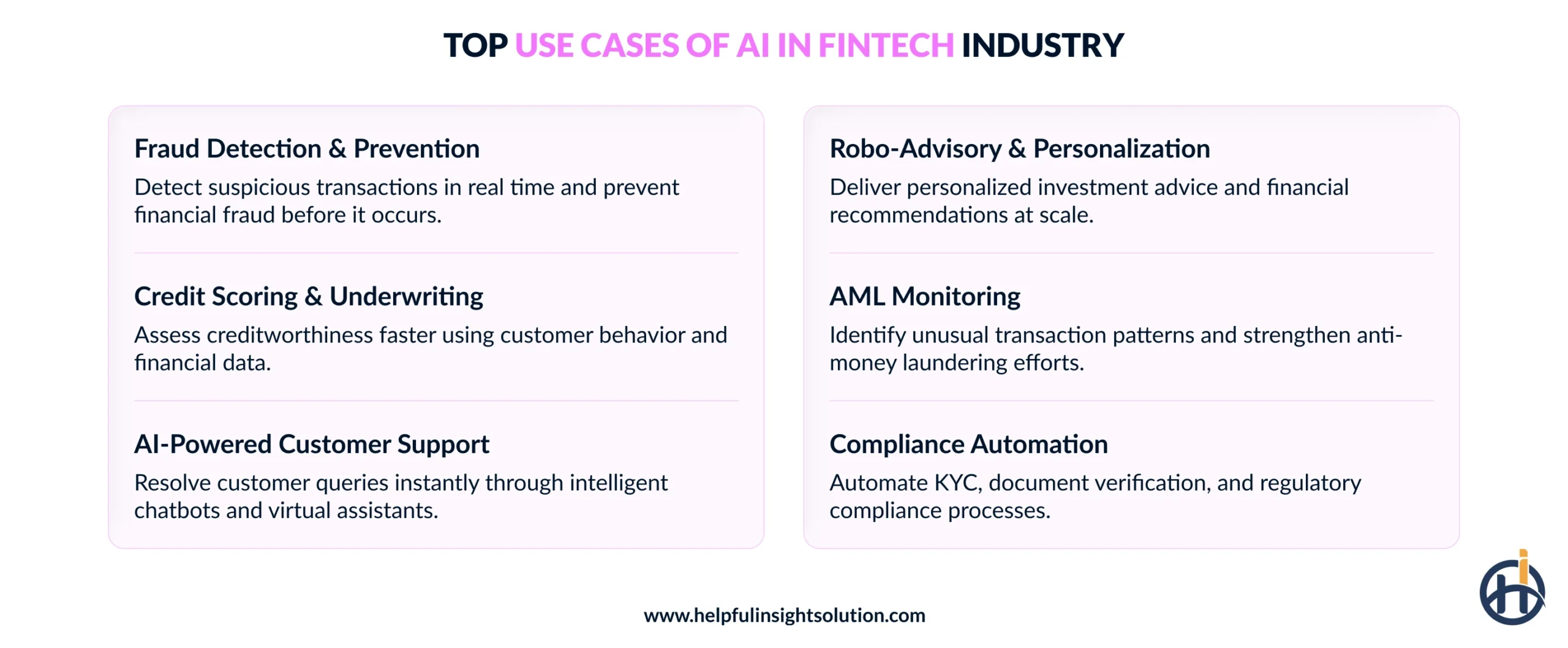

Fraud Detection and Prevention

Fraud detection is one of the most valuable applications of AI in fintech, as it works in real time to protect both you and your customers.

When a payment or a login comes in, the model instantly reviews signals such as the device, the location, the transaction amount, and the customer’s usual behaviour, and then decides whether to approve it, decline it, or ask for an extra verification step.

This whole process happens within seconds, and so customers can be updated with the final status of the transaction within seconds.

Credit Scoring and Underwriting

Credit scoring is where AI in fintech directly improves the way you lend. Instead of depending only on a traditional bureau score, the model can analyse a customer’s bank transactions through open banking and understand their real income, spending habits, and repayment behaviour.

This allows you to approve customers with little or no credit history within seconds, set a credit limit that matches their actual repayment capacity, and revise it later as you learn more about them.

For a lending business, this is often the use case with the most direct impact on revenue, since it helps you approve more customers without raising your default risk. If you are planning to build these lending and scoring features into your product, the same logic sits at the core of most fintech software development projects, especially lending, credit scoring, and risk assessment platforms.

Customer Support With Chatbots and Virtual Assistants

Customer support is usually the first place where your customers experience AI in fintech.

A virtual assistant can handle the repetitive queries that fill a fintech’s support channels, such as a failed payment, a balance check, a card block, or a password reset, and pass only the complex cases to your team.

It can also guide customers through KYC and document submission during onboarding, which reduces the number of users who drop off midway.

The generative AI that powers these assistants is growing rapidly, with the generative AI in the financial services market valued at USD 2.96 billion in 2025 and projected to reach USD 25.71 billion by 2033 at a CAGR of 31.0%, according to Grand View Research. Since most of this support now happens inside the app rather than over a call, building a strong in-app assistant has become more important than before, a shift that is clearly visible across mobile app usage statistics.

Personalised Advice and Robo-Advisory

With AI, you can offer every customer the kind of financial guidance that was once limited to high-value clients only.

A robo-advisor takes a customer’s financial goal and risk appetite, builds a suitable investment portfolio, and keeps rebalancing it automatically as the market moves, all at a cost low enough to serve even small investors profitably.

For many fintechs, this also opens the door to micro-investing, where a customer starts with a small amount, and the system manages everything for them.

Compliance, AML, and Back-Office Automation

A large part of the value of AI in fintech sits quietly in the back office. The model runs continuous transaction monitoring to identify money-laundering patterns, screens customers against sanctions and PEP lists, and cuts down the false positives that usually bury a compliance team in manual checks. It can also read and extract information from onboarding documents, so a verification that earlier took an analyst several minutes now finishes in seconds.

These same models are not limited to fintech alone. Insurance companies apply them to claims and underwriting in a very similar way, which is the idea behind automation in insurance.

Real-World Examples of AI in Fintech

Some fintechs are leading the AI, and looking at what they have actually built is the quickest way to understand what is possible in your own product.

Below are a few fintechs with top AI technology and what each one is doing with it.

Stripe

Stripe runs one of the most advanced fraud systems in payments through Radar, its machine learning engine.

Radar scans every payment using hundreds of signals and is trained on over USD 1 trillion in annual payment volume, which the company says reduces fraud by 32% on average, according to Stripe. Since it learns from millions of businesses at the same time, there is a 92% chance any given card has already been seen somewhere on the Stripe network, and that shared view is what makes its scoring so accurate.

Plaid

Plaid sits between apps and banks, and it has built financial models on top of that network. Its Trust Index now identifies 30% more fraud than earlier versions by reading transaction history alongside network patterns, while Plaid Signal has analysed more than USD 185 billion in payments to judge payment risk.

This is an example of AI applications in fintech that quietly power onboarding, risk checks, and lending decisions inside many fintech apps you already use.

Klarna

Klarna is the most obvious example of what AI can do for customer support. Its assistant, built with OpenAI, handled two-thirds of the company’s customer service chats within its first month, which added up to 2.3 million conversations and the workload of around 700 full-time agents.

It also brought the average resolution time down to under two minutes from eleven, while managing queries in more than 35 languages.

Mastercard

Mastercard is a payments network rather than a fintech, but its AI sits under a large part of the rails fintechs run on. It uses generative AI to double the rate at which it detects potentially compromised cards, so banks can block and reissue them far sooner. The same technology also cuts false positives by up to 200% and helps it spot at-risk merchants much faster.

What stands out across these fintechs with top AI technology is that none of it is out of reach. They are using the same use cases covered earlier, just at a larger scale, and the approach carries into neighbouring sectors too, which is why insurance software development has moved in much the same direction. If you’re exploring where else this kind of automation fits, our list of AI business ideas covers opportunities beyond fintech as well.

What are the Adoption Challenges in AI For Fintech?

Adopting AI solutions for fintech is not plug-and-play, but putting it inside a regulated financial product brings a set of challenges you need to plan for early.

Here we have compiled a list of the challenges you might come across.

Data Privacy and Security

Financial data is among the most sensitive data any business can hold. When you use AI in fintech, you feed this data, such as account details, transaction history, and identity records, into your models, and all of it has to stay protected and used only in the way the customer agreed to.

Data privacy is also the biggest worry across the industry, rated as the top AI risk by 74% of financial firms. So strong data protection has to be in place before you scale any model.

Regulatory Compliance Across Markets

The rules for AI change in every market you operate in. In the US, you answer to the SEC and the CFPB. In India, the RBI sets the terms, and in the UAE, the central bank and local authorities do.

Each of them looks closely at how your model makes decisions on credit, fraud, or advice, and whether those decisions are fair to the customer. This is the reason 69% of financial firms have asked for clearer regulatory guidance. Therefore, building compliance into your system from the start costs you far less than fixing it later.

Bias and Explainability

An AI model can give accurate results and still cause problems if it cannot explain how it reached them. When you decline a loan or block an account, regulators and customers both expect a clear reason behind the decision, not just a score.

Explainability and bias checks should therefore be implemented in your design from day one, not get added later.

Legacy System Integration

Most established financial companies still run on old core systems that were never built for AI. Connecting AI to these systems is challenging, as the data usually sits in separate silos and the formats do not match, which leaves the model without the clean data it depends on.

Data availability and quality are, in fact, the leading barrier to AI adoption. This is one area where fintechs have an edge, as they usually run on newer systems and can feed their models properly from the start. Enterprises facing this exact bottleneck often benefit from a structured approach, similar to what we outline in AI for enterprise.

Talent and Cost

Artificial intelligence in fintech needs people who understand both finance and machine learning, and this mix is hard to find and costly to keep. Cost adds more pressure, though, as the earlier numbers showed, higher spending tends to bring better results rather than wasted budget.

The sensible way forward is to start with one use case that has a clear return, prove it works, and grow your team and budget around it.

Final Take

AI in fintech is no longer a plan. It already runs inside the products people use every day, whether that is the fraud check on a payment or the assistant answering a support query. The companies getting real value from it are not the ones with the biggest budgets, but the ones that picked a clear use case, proved it worked, and grew from there.

So the question for you is not whether to adopt AI, but where to begin and how to do it without running into the data and compliance issues covered above. This is usually far easier with a partner who has built these systems before.

At Helpful Insights, we build AI solutions through financial software development for fintech businesses and startups across India, the USA, and the UAE through our fintech app development services. So, if you are planning to bring AI into your fintech product, talk to our team, and we will walk you through what is possible for your specific case.

Frequently Asked Questions (FAQs)

Yes. Most AI solutions for fintech startups today are accessed through pre-built APIs and pre-trained models rather than being built in-house. Providers like Stripe, Plaid, and several cloud platforms let you add fraud scoring, KYC, or document reading with a simple integration and pay only for what you use. This build-versus-buy choice is why a small team can now ship AI for fintech features that once needed a full data science department.

The next stage of fintech and AI is agentic AI, where models do not just analyse data but act on it, such as moving money or approving a step in a workflow on their own. This is already moving fast, with 52% of financial firms actively adopting agentic AI and 81% expecting it to be meaningfully in place by 2030, according to the Cambridge Centre for Alternative Finance. The shift means more decisions will run end-to-end with lighter human involvement, which also raises the bar for oversight and controls.

In most cases, AI in fintech supports people rather than replacing them. It takes over repetitive, high-volume work like first-level support, document checks, and transaction reviews, while humans handle the complex cases, the exceptions, and the final call on anything high-risk. The practical effect is that teams spend less time on routine tasks and more on judgment-heavy work, which is where fintech and artificial intelligence tend to work best together.

Traditional automation follows fixed rules that someone writes in advance, so it does the same thing every time until the rules are changed. AI and machine learning in fintech work differently, as the model learns from data and adjusts its own output as patterns shift. This is why a rule-based system struggles with new fraud tactics, while an ML model can pick up on behaviour it was never explicitly told to look for.

Before picking a partner for AI for fintech, look at where their data comes from, since a model is only as strong as the data behind it. It also helps to check whether the solution can explain its decisions, how it handles data privacy, and whether it fits the regulators in your markets. For many fintechs, the right mix is using a trusted provider for common tasks and a development partner for the parts that are specific to their own product.