The insurance industry has always been a paper-intensive industry, and most of the paperwork moves through human hands, making the process lengthy and cumbersome.

What if 50-60% of those backend operations, like data entry, policy updates, and claims verification, can be done without human involvement?

Automation in insurance industry has the potential to do so. Additionally, technology advancements like Robotic Process Automation (RPA) are helping insurers automate rule-based processes today and laying the groundwork for intelligent automation tomorrow, and opening the door to broader AI development across the insurance value chain.

According to McKinsey & Company, the deployment of robotic process automation in the insurance industry has delivered up to a 200% ROI within the very first year of rollout.

Keeping it simple, automation in the insurance industry has the potential to eliminate the tedious manual work, so your human employees can work on more productive tasks.

So, if you are in the insurance industry, then automation is the key to getting more work done efficiently at a lower cost. This blog will help you with a detailed understanding of automation in the insurance industry and how it can be implemented in your business.

So, let’s get started.

What Does Robotic Process Automation in Insurance Mean?

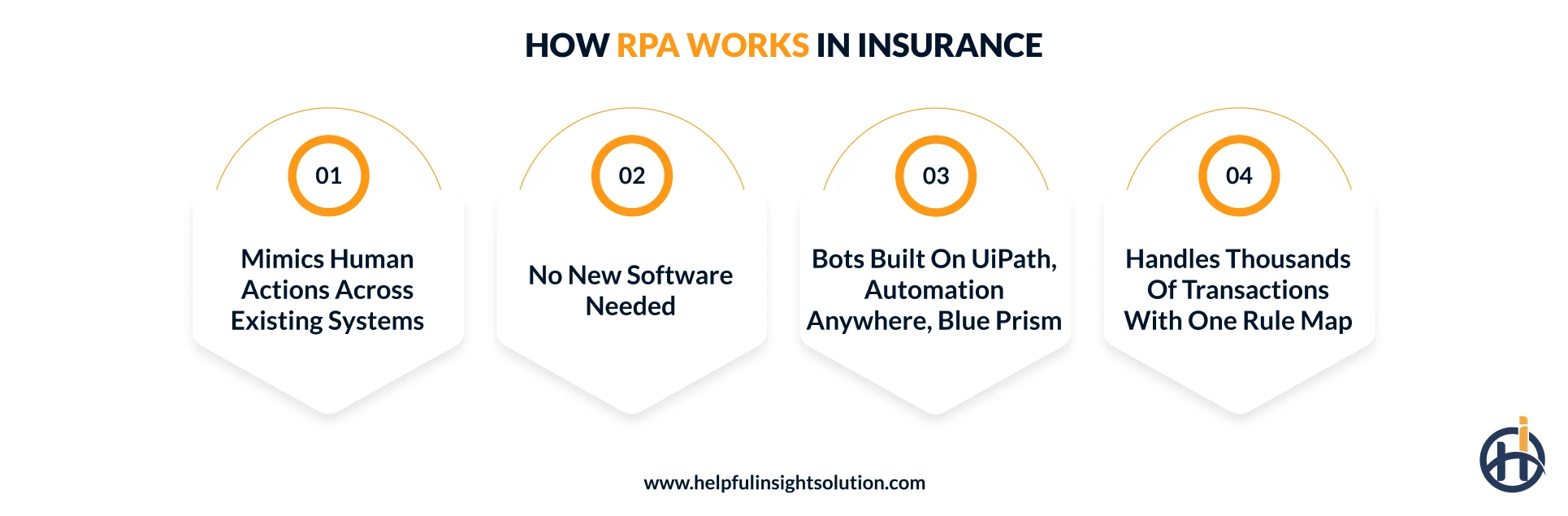

Robotic process automation is a software or a tool that can perform repetitive, rule-based work that your team has to do everything on its own.

These repetitive tasks could be anything from opening policies, copying customer data, filling forms, or updating records. RPA in insurance industry can do it all on its own, without a single click from your team.

Additionally, RPA is built to mimic human actions across your existing systems, so there is no need for new insurance software development.

Technically speaking, RPA for insurance refers to bots built on platforms like UiPath, Automation Anywhere, or Blue Prism. These bots are trained on a defined set of rules.

You map the process once, the screens to open, the fields to fill, the data to move, and the bot repeats the same action across thousands of transactions. Also, for scanned documents or PDFs, the bot uses OCR to read the content and API calls, where available, to move data faster between systems.

You can name RPA as your business’s digital workforce, running the manual work in the background while your people focus on the work that actually needs human judgment.

So, if your insurance firm is still running the same repetitive tasks manually every day, insurance business process automation is where you should start.

How Does Robotic Process Automation Benefit the Insurance Industry?

Insurance business process automation is not just about replacing the manual work your team does every day. It is about what your business actually unlocks once that manual load is off the table.

The real benefit can also be measured in the metrics that move an insurance business, such as claims turnaround time, cost per policy, underwriting speed, customer retention, and more.

According to the survey, 92% of organizations that have deployed RPA report that it has met or exceeded their expectations on compliance, and 90% report the same on quality and accuracy.

Here we have compiled a list of insurance automation benefits:

1. 24/7 Operational Team

The insurance industry heavily relies on human resources, and they often work in shifts. Therefore, to have a 24/7 operational team, you might have to hire employees who work in shifts.

However, once automation software insurance is deployed, it can work to serve your customers 24/7. From claim settlement, policy renewals, KYC verifications, and more can be done with no human agent involvement at the hours customers prefer.

For your insurance firm, this means no claim sits in a queue overnight, and no customer waits for the next business day to get their request acknowledged.

2. Better Renewal and Retention

Renewals are the time when most of the insurers often lose their customers. The reason could be anything beyond just the policy, it could also be because of communication.

Automated InsurTech can help you have personalized communication. Additionally, it can pull the customer’s policy history, flags pending endorsements, processes information requests faster, and turns around endorsement updates in hours instead of days.

For example, insurance robotic process automation can trigger personalized messages on birthdays, policy anniversaries, and life events, the same way your best relationship manager would, just for every single customer in your book.

According to McKinsey & Company research, customer-centric transformation, like personalized communication, can increase customer satisfaction by 20%. As a general rule of thumb, increased customer satisfaction throughout the policy period can improve the customer retention rate. Additionally, it will also help in improving the marketing of words, which means new customer onboarding without spending a single penny on marketing.

3. Lower Cost Per Policy

Cost per policy is one of the most important metrics that insurers track to evaluate their marketing and sales team productivity. Therefore, having a lower cost per policy means higher revenue.

Insurance software development with RPA can eliminate the manual touchpoint in policy issuance, servicing, and renewal, adding to this number. RPA brings it down by taking over the rule-based work across data entry, document verification, premium calculation, and policy generation.

The deployment of RPA can reduce insurers’ operating costs by 40%, with 95% enhanced efficiency by eradicating manual efforts.

So, for your firm, a lower cost per policy means you can either improve margins, price more competitively, or reinvest in growth, all without touching service quality.

4. Improved Underwriting

Underwriting is among the insurance companies’ most tedious processes that defines everything that comes after. Therefore, the underwriting process must be efficient and assess the risks to ensure only an eligible person can get the insurance.

As said, it is a tedious process, therefore, teams often spend a large part of their day pulling customer history, credit checks, claims records, and third-party data from different platforms before they can even start pricing the risk. Pairing RPA with the right insurance underwriting software can automate the end-to-end underwriting process, from data pulls to decision-ready files.

The RPA bot can pull the data, cross-check it, populate the underwriting worksheet, and hand a ready-to-decide file to your underwriter.

5. Employee Productivity on High-Value Work

When employees work on the tasks that actually matter for an insurer, they are most productive.

For example, your claim management team can spend more time on complex, high-value claims. While your underwriters can focus on judgment-led risks. Similarly, your customer service team can handle escalations that actually need a human voice, while the rest of the processes are taken care of by the AI ticketing system with RPA.

Intelligent process automation can free up 20-35% of an employee’s time for higher-value work. It is similar to having two extra working days per week, every week, redirected toward work that actually grows the business.

6. Customer Onboarding and Support Time Drops

Insurance onboarding has always been the slowest part of the customer journey. KYC, document verification, policy issuance, welcome communication, the entire stack can take 2 to 3 weeks in a manual setup.

Insurance business process automation can reduce this to days.

Insurance automation software can verify documents, run background checks, populate the policy admin system, issue the welcome kit, and route any exceptions to your team, all without a human touching the keyboard.

On the support side, RPA in insurance also powers self-service options for your customers. Things like instant policy document downloads, premium payment status, claim status updates, and endorsement requests can all be handled by bot-driven self-service insurance portals, available 24/7. According to Salesforce, 81% of customers prefer to resolve issues on their own before reaching out to support.

So your support team handles the cases that actually need human help, and your customers get faster answers on the routine ones.

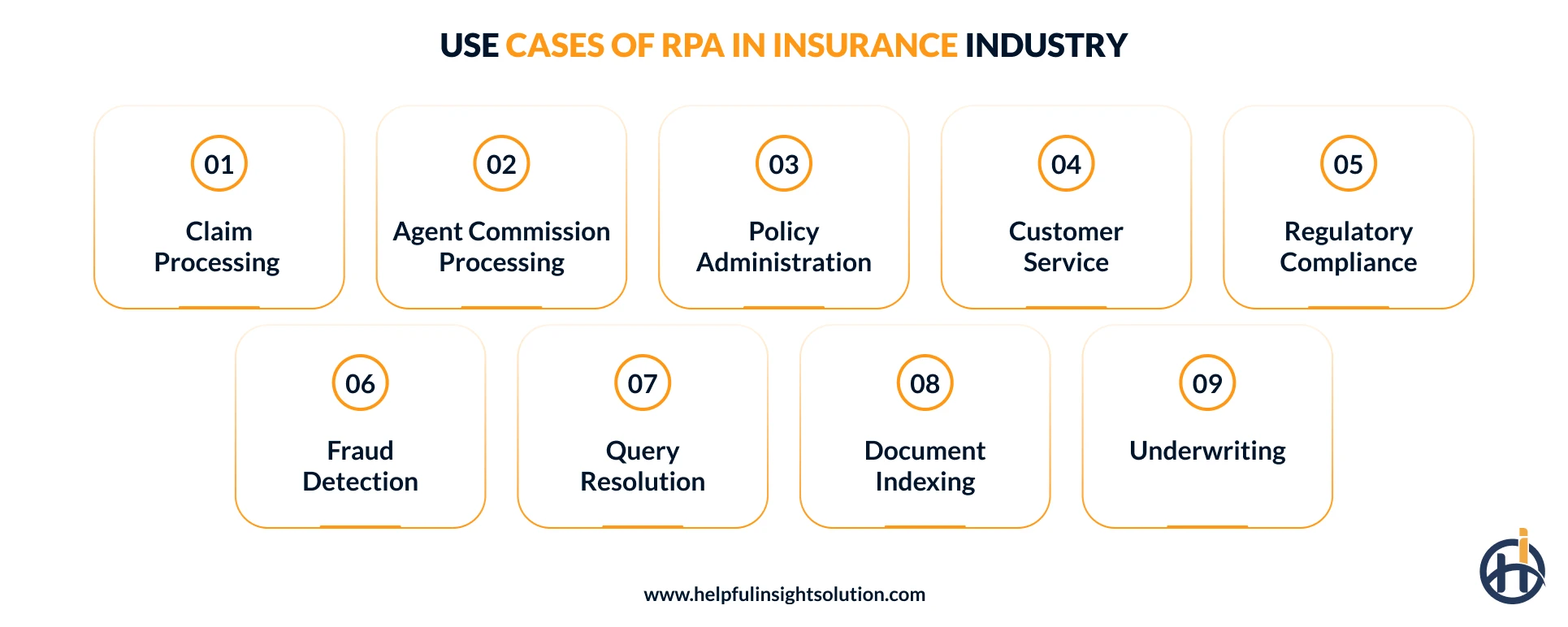

Robotic Process Automation Insurance Use Cases

Insurance is one of the few industries where the entire value chain, from new business to renewals to claims, runs on structured, document-heavy work.

This is exactly the kind of workflow RPA is built to handle. So, the use cases for RPA in an insurance business are not limited to one or two departments; they run across the front office, the back office, and every system in between.

Claim Processing

First Notice of Loss (FNOL) is the first step in the claim processing journey. Additionally, it is the time when insurers are expected to act fast, but their time often goes by browsing through email, web form, call center, mobile app, or even WhatsApp.

RPA captures the FNOL from all these channels, extracts the relevant details, validates the policy status, checks coverage, and routes the claim to the right adjuster based on claim type, value, and complexity. The customer gets an acknowledgment within minutes, and the claim file is already open before your team even sees it.

This is one of the most high-volume RPA claims processing use cases insurers deploy first, simply because the claim processing bottleneck is where customer experience scores drop the fastest. Insurers looking to fix this bottleneck are increasingly turning to Insurance Claims Management Software to bring every FNOL channel, adjuster workflow, and claim status update into one automated system.

Agent and Broker Commission Processing

Agents and brokers are the backbone of the insurance business of all sizes. Therefore, having a system that can calculate their commission transparently will build trust in the long-run.

The calculation rules vary by product, tier, geography, and volume slab, and the moment your agent network crosses a few hundred intermediaries, the manual effort becomes unsustainable.

RPA insurance software can pull the sales data from your policy admin system, apply the tier-based commission rules, generate statements for every agent and broker, and trigger the payout file to finance. It also handles clawbacks for cancelled policies, mid-cycle adjustments, and bonus calculations. Therefore, insurers are benefiting from faster commission payouts, fewer disputes from agents, and a finance team that no longer spends the last week of every month on reconciliation. A result that aligns well with what modern financial software development is built to deliver across complex, multi-tier payout structures.

Policy Administration

Policy administration runs across the full lifecycle of an insurance product, from issuance to endorsements to renewals to cancellations. Each of these stages involves rule-based data movement between your policy admin platform, billing system, and CRM.

RPA in insurance can handle the entire policy administration workflow. The bot pulls policy data from emails, faxes, and customer portals, processes change requests, calculates premiums, tracks expiration dates, and triggers renewal communications. Additionally, it can also generate personalized cancellation responses and update the policy status across every connected system.

Zurich Insurance Group deployed an automation solution where RPA bots enter policy details, issue invoices, and draft policy documents for officer review. As a result, Zurich clients receive policies of higher quality, and the internal support desk gets fewer clarification emails and calls.

Customer Service

Today’s insurance customers expect quick, accurate, and round-the-clock service. But most insurers still rely on manual call handling, email triaging, and policy lookup, all of which slow down response times and create inconsistent customer experiences.

Insurance robotic process automation can take over the routine layer of customer service. The bot pulls customer policy details on demand, sends real-time claim status updates, routes inquiries to the right department, and provides self-service options for policy document downloads, premium payments, and endorsement requests.

So, when RPA is deployed, your customer service team can work on cases that actually need human help, reach them faster, and the routine queries are resolved before they even hit your support queue. The most obvious benefit will be shorter call times, faster email responses, and an improvement in customer satisfaction.

Regulatory Compliance

As said earlier as well, insurance is one of the most heavily regulated industries. Every state, country, and jurisdiction has its own reporting format, frequency, and audit requirements. Therefore, for insurers operating across multiple geographies, manual compliance work becomes both expensive and risky.

Robotic process automation use cases in insurance can be applied across the compliance workflow. It can pull structured data from the policy admin, claims, and finance systems, format it per the regulator’s template, run validation checks, and submit the report on schedule.

Every action is logged with a full audit trail, so when the regulator asks for source data, your compliance team has it ready in minutes.

Fraud Detection

Frauds are the biggest challenge in insurance and often cost billions of dollars each year. Automation solutions for insurance can help in fraud detection.

RPA bots can scan every incoming claim against historical patterns, watchlists, duplicate submissions, and inconsistent data points. It flags suspicious cases, escalates them to the Special Investigations Unit, and pulls supporting evidence from internal and external databases.

For example, Allianz UK developed a machine-learning tool called ‘Incognito’ to identify potentially fraudulent claims, which are then referred to a fraud expert for review. Since its rollout, the claims identified by Incognito have already saved £1.7 million, with a further £3.4 million held in claim reserves pending investigation.

So, robotic process automation insurance use cases do not just eliminate repetitive work, but can also detect fraud to protect an insurance business.

Query Resolution

Insurance firms receive massive volumes of customer and broker queries every single day, by email, phone, and chat.

Traditional practices of handling queries are often slow, error-prone, and exhausting for your team.

RPA for insurance can use a predefined set of rules integrated with natural language processing(NLP) to analyze incoming queries, classify them by type and urgency, and route them to the right specialist. For routine queries like policy document requests, claim status updates, premium payment confirmations, and endorsement updates, the bot resolves them end-to-end without human intervention.

This is one of the first RPA in insurance use cases that can benefit brokers, agents, and customers at the same time. Broker and agents can have a faster turnaround on the small but high-frequency questions that used to clog email inboxes. For your customers, it means the answer to a routine query is no longer dependent on when your support team can get to it.

So, this is one of the most underrated robotic process automation examples in insurance, because query resolution directly shapes the daily experience of both your customers and your distribution network.

Document Indexing and Classification

As said earlier, insurance is a document-intensive industry that often deals with thousands of documents every single day. These documents include claim forms, medical reports, vehicle damage photos, KYC papers, policy documents, hospital bills, repair invoices, and more.

Many insurers are combining RPA with OCR to enable it to read documents, identify the document type, extract the key fields, tag them with the right policy number and customer ID, and file them in the correct repository. So when your claims adjuster opens a file, every supporting document is already indexed and searchable.

Underwriting

Underwriting is where insurance firms make the most consequential decision in the policy lifecycle, pricing the risk. But underwriters today spend a large part of their day pulling customer history, medical records, credit checks, and third-party data from different systems before they can even begin the actual risk analysis.

RPA use in insurance underwriting fixes this. The bot pulls customer data from internal CRMs, policy admin systems, and third-party sources like credit bureaus, medical record providers, and government databases. It can also pre-fill the underwriting worksheet, flag missing details, validate the data, and hand a ready-to-decide file to your underwriter.

For example, Aviva launched an industry-first AI-powered summarisation tool specifically built to speed up the underwriting process for individual life insurance applications. It cuts down the document-heavy review work that used to slow down underwriters across high-value life insurance cases.

What are the Challenges of RPA in Insurance and How to Overcome Them?

Indeed, the benefits and use cases of the RPA in the insurance industry seem promising for carriers of all sizes. But the reality of deploying it across an insurance business is rarely without challenges. Here are the most common challenges insurance firms run into during RPA adoption, along with practical ways to overcome each of them. So, you can identify them at the earliest and plan an RPA development roadmap to mitigate them.

Handling Unstructured Insurance Data

RPA is as efficient as the data it runs on. Unstructured data, such as scanned claim forms, hand-written medical records, vehicle damage arrives as photos, and KYC documents land in PDFs of varying formats.

RPA works well on structured data. So, when the workflow has unstructured data as mentioned above, its efficiency will be reduced.

The best practice is to have structured data that RPA bots can easily interpret and take prescribed actions. This becomes more important in robotic process automation, health insurance and robotic process automation in life insurance, where the document mix is at its most complex.

Compatibility with Legacy Insurance Software

RPA also works well when it can communicate efficiently with all the systems that run an insurance business. However, a large share of businesses are using legacy insurance software with no modern APIs supported to communicate with each other.

Additionally, legacy software integration often needs expensive middleware or custom coding, making RPA adoption challenging. Which is why many carriers prefer working with specialized insurance IT services teams that already understand the system landscape before writing a single line of integration code.

The solution lies in RPA’s biggest design strength. The bot mimics human actions at the user interface layer, so it works on top of your legacy software the same way a person would, no API required. For systems that do have APIs, RPA can use them too, creating a hybrid setup that scales without rebuilding your core infrastructure.

Employee Resistance to Automation

The biggest challenge in RPA adoption is employee resistance. Wherever a company says they will automate insurance processes, the natural reaction from underwriters, claims adjusters, and customer service teams is the same. Is the bot going to replace me?

This is one of the most underestimated challenges in any RPA rollout. The technology can be perfect, but if your people are not behind it, adoption fails.

The best practice to ensure that employees can adopt RPA is to introduce it as an augmentation rather than a replacement. Help employees to understand how it can remove the tedious work from their day-to-day tasks, so they can focus on higher-value work.

Security and Compliance for Bot-Level System Access

Robotics process automation in insurance runs on credentials. Bots need to log into the policy admin, claims, billing, and external systems just like an employee would. As a result, it is common among carriers to be concerned about security and compliance.

If a bot’s credentials are exposed, the breach surface is much larger than a single employee account, because a bot operates 24/7 across multiple systems.

The solution is to manage bot credentials through a centralized vault, apply role-based access controls, log every bot action for audit, and rotate credentials on a defined schedule. Every action the bot takes should be traceable to a unique bot identity, not a shared service account.

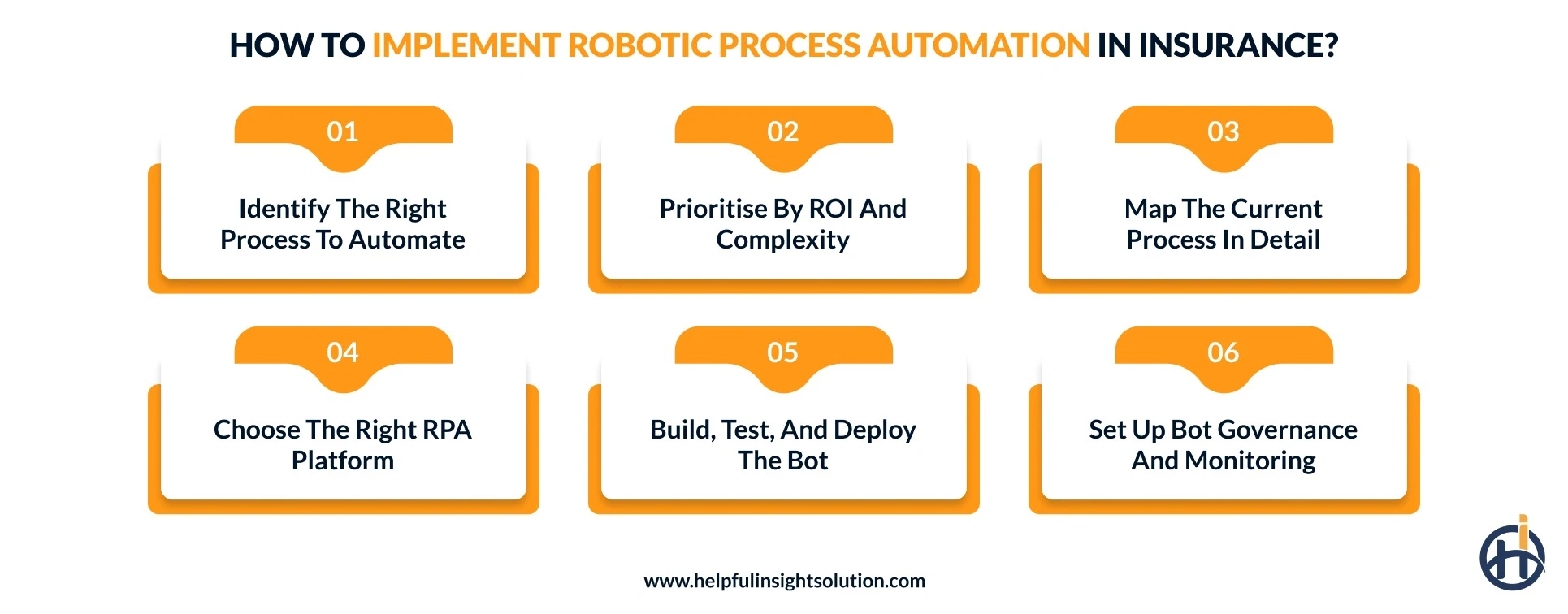

How to Implement Robotic Process Automation in Insurance?

Here is how you can implement RPA in your insurance business to realize the benefits we have discussed so far.

Identify the Right Process to Automate

The insurance industry has several processes, but all are equally important. Thus, you should start with the processes that have high importance in your business. Additionally, the process must be rule-based and run on structured data.

For example, you can start with the process of claim intake, policy issuance, KYC verification, or premium collection. These processes often have structured data and can be automated using rule-based automation.

The best practice is to avoid choosing practices that need human oversight at each step or that often change rules more frequently.

Prioritise by ROI and Complexity

You might have multiple insurance processes to automate. The best practice is to have a priority order rather than implementing them all at once.

So, you should start with your shortlisted processes on a simple 2×2, business impact on one axis, automation complexity on the other. The processes that have a high impact and low complexity are best to get started with.

Map the Current Process in Detail

RPA in insurance works on rules that help it to learn the process end-to-end. Therefore, you must map every click, every screen, and decision point to make it easier for the bot to follow the process correctly.

The best practice is to work with a software development company that can align with the team actually running the process and document it to ensure the right execution.

Choose the Right RPA Platform

The leading RPA platforms for insurance are UiPath, Automation Anywhere, Blue Prism, and Microsoft Power Automate.

These platforms are just a few of the examples, the selection often depends on your existing IT environment, the scale of bots you plan to run, and your team’s technical maturity.

Build, Test, and Deploy the Bot

The developer builds the bot logic based on your process map, configures the screens and rules, and integrates OCR or API calls where needed.

The bot should then be tested with the actual business team to ensure its effectiveness. Once the testing is done, it should be deployed in the production environment with strategies to roll back, if things don’t work as expected.

Set Up Bot Governance and Monitoring

RPA deployment is not a one-time deployment, it often requires a governance system to ensure it works effectively.

The best practice is to set up a control room to track every bot’s status, performance, and errors in real time. Additionally, you can assign clear ownership, who maintains the bot when the underlying application changes, who handles exceptions, and who approves logic updates.

How can Helpful Insight Help You with Insurance Automation Solutions?

Adopting robotic process automation in insurance is a journey, and it works best when you have the right partner walking it with you.

Helpful Insight is an experienced insurance software development company that has been working with insurers across India, the USA, and the UAE. Our team has spent over a decade building automation solutions for the insurance industry, so we understand both the technology and the daily operational reality of running an insurance business.

We have experience working across end-to-end RPA automation solutions deployment for insurance businesses:

- Process assessment: identifying the right workflows to automate first, based on business impact and complexity

- Platform selection: choosing the right RPA platform, such as UiPath, Automation Anywhere, Blue Prism, or Microsoft Power Automate, based on your IT environment

- Bot development: building, testing, and deploying the bot to production with rollback safeguards

- Integration: connecting RPA with your existing policy admin, claims, billing, and CRM systems, including legacy software

- Governance setup: control room configuration, bot monitoring, exception handling, and version control

- Scaling support: moving from one bot to enterprise-wide automation through a center of excellence

So, whether you are a regional carrier looking to automate one workflow or a larger insurance firm planning a multi-department rollout, we can match the scope of work to your stage of automation.

FAQs

RPA, or Robotic Process Automation, in insurance is software that follows a fixed set of rules to perform repetitive, structured work.

AI, on the other hand, can learn from data and make decisions on its own. So, what does RPA mean in insurance? It means a digital workforce that runs your rule-based work, like data entry, policy updates, and claims verification, without learning or judgment of its own. When you combine RPA with AI, the bot can also handle unstructured inputs like images and free-text emails, which is where intelligent automation begins.

The cost to automate insurance processes depends on the number of workflows, the platform you choose, and whether you build in-house or partner with an insurance IT services provider.

The best way to plan the budget is to start with one high-impact workflow, prove the ROI, and scale from there.

A focused RPA pilot, covering one well-defined workflow, can be deployed in 4 to 6 weeks from process mapping to production. Larger rollouts across multiple departments take 2 to 6 months, depending on legacy system complexity, data readiness, and internal governance.

The fastest path is to start with structured, rule-based processes like RPA for claims processing or KYC verification, where the data is clean, and the rules are scoped.

Yes, RPA in life insurance and robotic process automation in health insurance are among the highest-impact deployments in the industry today.

In life insurance, RPA handles medical underwriting data pulls, beneficiary updates, lapse management, and policy reactivation outreach, which makes it especially effective for shortening the issuance cycle on high-value policies.

In health insurance, RPA powers claims adjudication, pre-authorization checks, provider network updates, and member onboarding. So, regardless of the line of business, the automation software used in insurance industry workflows can adapt to your operations.