Key Takeaways

- AI in insurance uses technologies like machine learning and predictive analytics to handle work that once needed manual effort, across underwriting, claims, fraud, and customer service.

- Real carriers already show the impact, with Lemonade settling a claim in two seconds and Ping An assessing vehicle damage at over 95% accuracy.

- The benefits of AI in insurance are clear: faster service, lower costs, sharper pricing, and stronger fraud control.

- The ROI is measurable, too. Aviva cut complex liability assessments by 23 days and detected 14% more claims fraud in 2024, worth over £127 million.

- The main challenges are data quality, regulatory compliance, talent shortages, and avoiding bias, most of which come down to clean data and strong governance.

- The future of AI in insurance points to agentic AI and hyper-personalised cover, with the market projected to reach $154.39 billion by 2034.

Insurance has always run on data, and AI turns that data into faster decisions. AI in insurance means applying machine learning, predictive analytics, and natural language processing to tasks that previously required significant manual effort across your core insurance operations, from pricing a policy to settling a claim.

Used well, artificial intelligence in the insurance industry helps insurers price risk more accurately and serve customers with far less effort and cost.

In 2025, 90% of insurers were already exploring generative AI, and 55% had reached early or full adoption of AI. (Conning’s 2025 survey)

This blog covers AI in insurance use cases with real examples: Lemonade, Ping An, Aviva, and Zurich. Also, it talks about the business benefits, ROI, implementation challenges, and regulatory considerations, along with a prediction of where AI is heading.

So, let’s get started.

What is AI in Insurance?

AI in insurance can be referred to as a computer system that learns from data and then makes or supports decisions across different insurance operations. It reduces the need for manual work across claims, underwriting, fraud detection, and customer service.

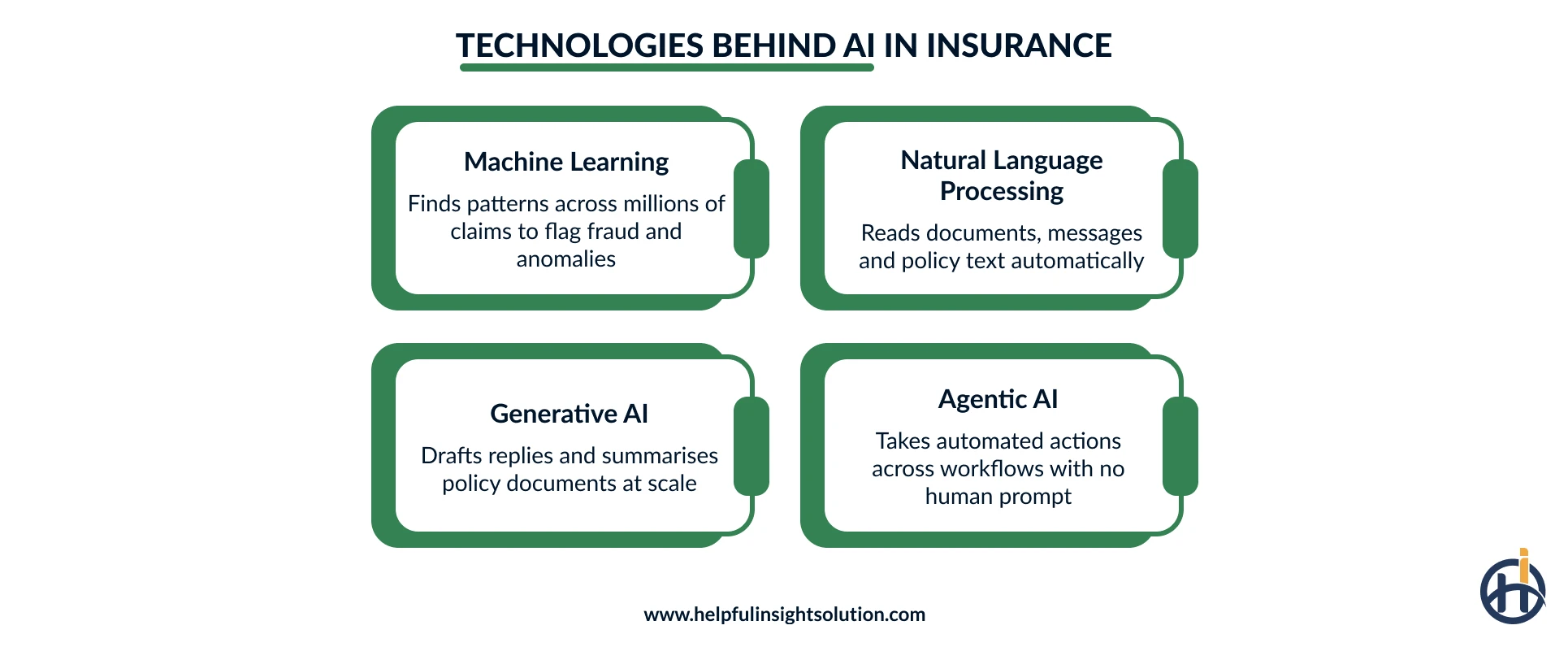

Artificial intelligence uses several technologies, such as machine learning and natural language processing, each having a specific job.

Machine learning identifies patterns across large data sets, flagging anomalies and fraudulent activities that manual review would miss.

Natural language processing reads documents, customer messages, and policy text, making it possible to automate tasks that involve written or spoken language.

The advancement in AI, such as generative AI and Agentic AI, enables insurers to automate draft replies, summarise policy documents, and take automated actions with no human involvement needed.

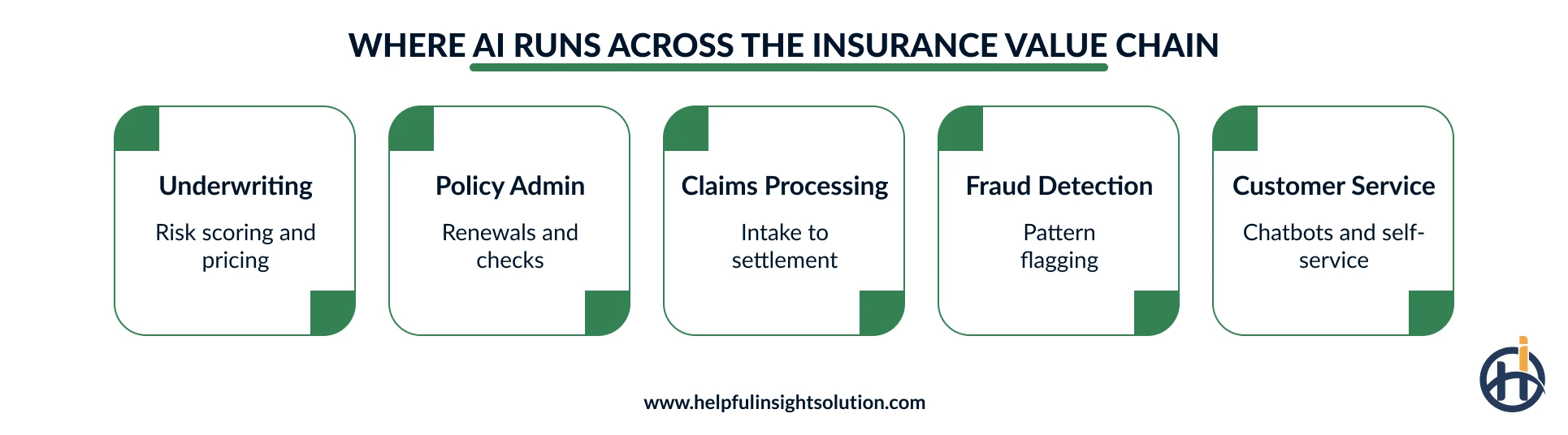

From supporting underwriting, claims management, policy administration, and customer service, AI can be used across the whole insurance value chain.

AI in Insurance Use Cases With Real-World Examples

AI in insurance applies across the whole insurance value chain. Here we have outlined a few of the most common use cases of AI in insurance, along with real-world examples of carriers running them and getting benefits.

Claims Processing

Claim processing is one of the earliest and most widely adopted use cases of artificial intelligence in the insurance industry. The full claims cycle, from intake and document review to policy matching and approval decisions, involves repetitive, rule-based steps that purpose-built claims management software and AI handle faster and more consistently than manual processing.

Lemonade, a US digital insurer, runs an AI claims bot called AI Jim that reads a claim and checks the policy, then runs anti-fraud checks before approving payment. In 2023. AI Jim helped the insurer to process the claim in two seconds, which was too human-like in the process. Lemonade also says that it uses AI across a large share of the claims to ensure the process gets finished within hours at last.

Underwriting and Pricing

Underwriting and pricing are AI and ML use cases in insurance that have been adopted by all sizes of insurers. Models assess risk using far more data than a manual underwriter can process, improving both the accuracy of pricing and the speed of approval decisions. Furthermore, predictive analytics enables more precise, tailored pricing built around individual risk profiles rather than broad category averages.

Ping An, one of the world’s largest insurers, uses AI image analysis to assess vehicle damage at over 95% accuracy, so a motor claim can be priced from a few photos in minutes instead of waiting for an in-person inspection.

Fraud Detection

Fraud drains the industry. The Coalition Against Insurance Fraud estimates it costs the US $308.6 billion a year, and fraud appears in roughly one in ten property-casualty claims.

AI fraud detection in insurance examines each claim against millions of historical records, identifying patterns and inconsistencies that manual review would miss or take far longer to catch.

Zurich, which has been using real-time AI fraud detection for several years, scans industry-wide claims data and says it now identifies the equivalent of £260,000 in fraudulent claims every single day.

Customer Service and Chatbots

Insurtech AI is also handling a large share of routine customer contact. Chatbots in insurance can answer policy questions, guide customers through quote flows, and log the First Notice of Loss (FNOL) at any hour, with no queue or wait.

Lemonade’s customer bot, Maya, runs the whole signup and quote flow inside a chat, while generative AI now drafts tailored replies and summarises long policy documents so human agents can spend their time on complex cases. This reflects a wider shift in generative AI use cases across industries that insurance is moving through faster than most.

In 2026, agentic AI is taking this further. Travelers launched an AI Claim Assistant, a voice agent that takes incoming claims calls, assists with claim filing, and updates customers on settlement progress, with human agents stepping in only for escalations.

Back-Office Automation

The use of AI in insurance is around both customer-facing and internal operations. AI automation in insurance can take over repetitive back-office work like data entry and document checks, which eliminates processing time and errors.

Ping An shows the scale this reaches in production, with AI woven across the operations that serve its 240 million-plus retail customers. At that size, back-office AI has become core infrastructure, well past the pilot stage.

Here’s the Benefits section, value-framed with data, and “benefits of AI in insurance” (the unused primary) woven in naturally.

Benefits of AI for Insurance Companies

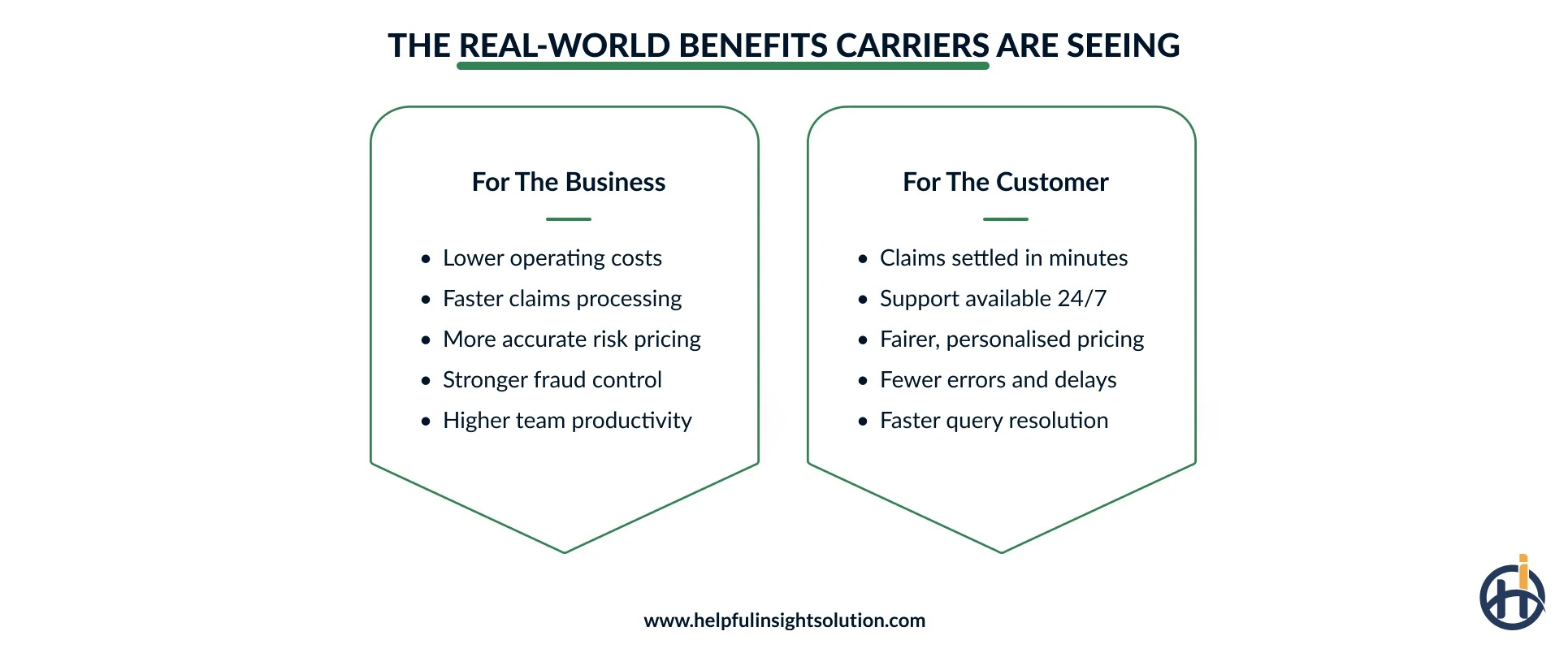

The benefits of AI in insurance are showing up on both sides of the business in lower internal operational costs and in improved customer experience. AI works across the whole value chain, including quotation, underwriting, claims, and service; the benefits add up across many small steps.

- Faster service: AI-driven claims processing can reduce claim and quote times to minutes while keeping customers informed at each step and the reasoning behind the decision.

- Lower costs and higher productivity: Automation handles low-touch tasks like document review, data entry, and claim processing, reducing operating costs while human agents focus on complex cases that need genuine judgment.

- Sharper risk pricing: Machine learning models can assess far more variables than a normal underwriter can, which improves loss ratio and reduces the number of underpriced policies that cost the business at the claims stage. Better pricing also means fairer premiums for lower-risk customers.

- Stronger fraud control: Real-time checks flag suspicious claims early, protecting margins that fraud would otherwise eat into.

- Better customer experience: Self-service and automated support run around the clock, reducing wait times and improving satisfaction without increasing headcount.

- Scale on demand: AI can also help to handle the sudden spikes in the claims volume that would need increasing headcount to keep up. AI absorbs that surge without a backlog, so customers still get a fast response at the moment they need it most, and the insurer avoids the need to hire and train temporary staff.

- Upskilled teams: When AI handles the repetitive tasks like data entry and document sorting, staff spend their time on work that needs human judgment, like investigating complex claims or handling sensitive customer conversations. This also tends to lower burnout and helps insurers keep their most experienced people

These benefits of AI in insurance are the most obvious sign of why adoption is increasing across carriers of every size.

Business Impact and ROI of AI in Insurance

In any sector, every investment is made by looking at the future potential and ROI of it, and insurance is no exception. Business impact and ROI of AI in the insurance industry are among the most common questions carriers assess to determine whether AI is a profitable investment for them or not.

The most obvious business impact of AI in insurance is often shown in faster prices and lower costs,

Process speed: Reduced process time is the biggest impact. Aviva rolled out more than 80 AI models in its claims work and cut the time to assess liability on complex cases by 23 days, while routing claims to the right team 30% more accurately. Similarly, Ping An brought its average claim settlement down to about 7.4 minutes, a speed that is often hard to match with manual efforts.

Fraud savings: Fraud detection is another measurable benefit of Artificial intelligence in insurance. Aviva used AI to detect 14% more claims fraud in 2024, stopping more than 12,700 bogus claims worth £127 million, around £349,000 a day., while Aviva used AI to detect 14% more claims fraud the same year. Every single penny saved from fraudulent activities is often the quantifiable measurement that AI development services yielded ROI.

Productivity gains: McKinsey estimates that generative AI could automate close to half of all manual insurance activities. At scale, those per-task savings across underwriting, claims and administration add up to material reductions in cost per policy.

Challenges of Implementing AI in Insurance

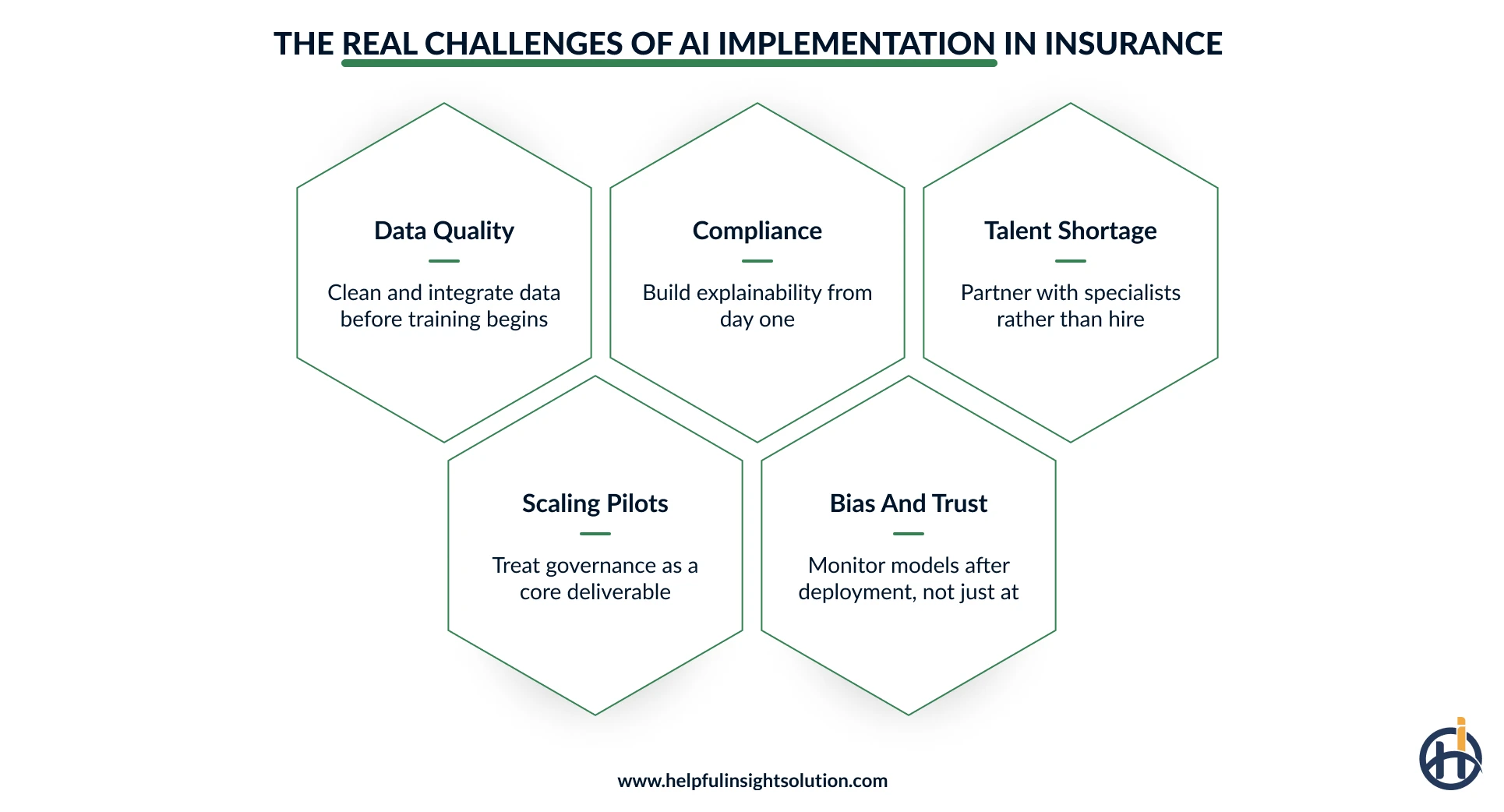

AI has many benefits to offer, but implementing it is not an easy task. Most insurers often face a few of the common challenges that can be mitigated if known earlier.

Data Quality and Legacy Systems

AI is only as good as the data it learns from. However, many insurers are still operating on legacy systems where data is often spread across different places. Therefore, before implementing AI, it is necessary to have a data integration and cleansing process to ensure data becomes useful for AI.

AI Regulatory Compliance

Insurance is a heavily regulated industry, so every AI decision has to be explainable. AI regulatory compliance in insurance means the pricing or claim decision made by a model should be fair and auditable.

In the US, state-level AI laws are creating a compliance patchwork, with California and Texas bringing in enforceable AI rules in early 2026 and New York setting fairness expectations for insurers using AI. In Europe, the EU AI Act treats many insurance AI applications as high-risk, requiring conformity assessments before deployment. In India, the IRDAI governs how insurers use technology and customer data. In the UAE, insurance AI sits under Central Bank oversight.

Building guardrails into AI systems from the start is significantly cheaper than retrofitting compliance after deployment.

Talent Shortage and Cost

Skilled AI engineers and data scientists are limited and expensive to hire. Insurers also compete for the same talent with big tech firms. The 2026 Evident AI Index confirms AI-specialist roles grew 32% year-on-year in insurance, but supply still trails demand significantly.

Building AI systems is only part of the cost. Maintaining, monitoring, and updating models as data patterns shift and regulations change adds ongoing expense that initial business cases often underestimate.

Scaling Beyond Pilots

Many AI projects deliver results in a controlled pilot and then stall before reaching full scale. According to McKinsey, most insurers are still stuck in pilot purgatory, and change management alone takes nearly half the effort of an AI transformation. Moving AI from a successful pilot to a live operational system needs process redesign, staff training, governance structures, and executive sponsorship, none of which the pilot itself tests.

Understanding the broader AI agents use cases for businesses helps insurers see where autonomous systems are already delivering results beyond the pilot stage and build confidence in scaling their own programmes.

Bias and Customer Trust

AI models trained on historical data inherit whatever bias exists in that data. In insurance, this means unfair pricing for certain customer groups or wrong claim denials, outcomes that carry both regulatory and reputational risk. Regular model monitoring is needed to catch and correct bias as it develops. Regulators in several markets now require insurers to show their models are fair and auditable, which makes this a compliance duty rather than an optional step.

AI Ethics and Regulatory Compliance in Insurance

AI in insurance often has access to money and customer-sensitive data, too, so ethics and regulations should be implemented to ensure AI can be trusted. As an insurer, you have to work with an insurance software development company that makes sure that AI usage is fair and explainable.

Fairness and Transparency

The biggest issue with AI is that it can be biased based on old data, which might result in inaccurate decisions. So, insurers need to test their models for bias and keep a human in the loop for sensitive decisions. Also, every automated decision should be explainable, so a customer or a regulator can understand why it was made.

Data Privacy

Insurance runs on sensitive personal data, including health and financial records. AI systems must protect this data and use it only for what the customer has agreed to. Therefore, the use of AI in insurance must be governed using data privacy rules, like GDPR in Europe, which set strict limits on how this data is collected and stored.

Regulations Across Markets

Insurance is a growing industry worldwide. However, the rules differ by region; therefore, you must have a transparent AI regulatory compliance insurance plan in place before any rollout.

For example, in India, the IRDAI oversees how insurers use technology and customer data. In the US, the NAIC has issued guidance on the use of AI by insurers, which individual states are adopting. In the UAE, insurance now sits under the Central Bank, which sets its own conduct and data rules. The EU AI Act adds another layer, treating many insurance AI uses as high-risk.

So, handling ethics and compliance well is what lets insurers use AI with the trust of both customers and regulators.

The Future of AI in Insurance

The future of AI will be around shaping the whole insurance business. Adoption is rising fast, and the numbers show where it is heading.

A Shift to Agentic AI

So far, most AI has assisted people. The next step is about AI agents that act on their own autonomously without human support needed. McKinsey expects that soon, nearly all customer onboarding in insurance could run through AI multi-agent systems, with humans stepping in only for complex or sensitive cases.

Hyper-Personalised Insurance

AI is making insurance more personalized by using real-time data. It can create tailored pricing and design policies around how a person actually lives or drives, like usage-based motor cover that rewards safe driving.

As carriers scale these capabilities, the customer-facing layer matters as much as the underlying models, which is why insurance portal development is increasingly where AI capabilities are first made visible to customers and agents.

Faster, Wider Adoption

The AI in the insurance market, worth $13.45 billion in 2026, is projected to reach $154.39 billion by 2034, a yearly growth rate near 35%.

Insurers are confident too, with more than half of European insurer leaders in a McKinsey survey expecting gen AI to bring productivity gains of 10% to 20%.

So, the future of AI in insurance points to coverage that is faster and more personal. The carriers investing today are the ones most likely to lead tomorrow.

Conclusion

AI has moved from a nice-to-have to a core part of how insurance works. It is already settling claims in seconds, pricing risk more accurately, catching fraud, and handling routine customer contact, with real carriers reporting measurable results. The challenges around data quality and compliance are real, but they are manageable with a careful approach.

For insurers, the focus now is on how to use AI well. The ones that start early, with clean data and strong governance, will be ready for the agentic and highly personalised future taking shape across the industry. So, whether you run a large carrier or a growing insurtech, AI in insurance is no longer something to watch from the sidelines.

FAQs

AI is used across the whole insurance value chain. It can handle claims processing, underwriting, fraud detection, and customer service, often working behind the systems insurers already use.

The main benefits of AI in insurance are faster service and lower operating costs. It also improves pricing accuracy and fraud control, while freeing staff to focus on complex work. For customers, this means quicker claims and support at any hour.

Yes. AI is one of the most effective tools for fraud detection in insurance. It checks each claim against millions of past records to spot suspicious patterns that manual reviews often miss, and insurers like Zurich and Aviva already use it to flag large volumes of fraudulent claims every year.

The future of AI in insurance is moving toward more automation and personalisation. AI agents will handle more tasks on their own, like onboarding and parts of underwriting, while pricing becomes tailored to each customer. Adoption is rising fast, too, with AI in the insurance market projected to grow strongly through the next decade.